As the cost of living begins to ease, consumers are hoping to ramp up their savings, but it’s unfortunate timing. Just as consumers are looking to make their money work harder, banks are slashing their interest rates.

As record numbers of savers shop around for the best rates on offer, how can banks retain their customers and help them grow their savings?

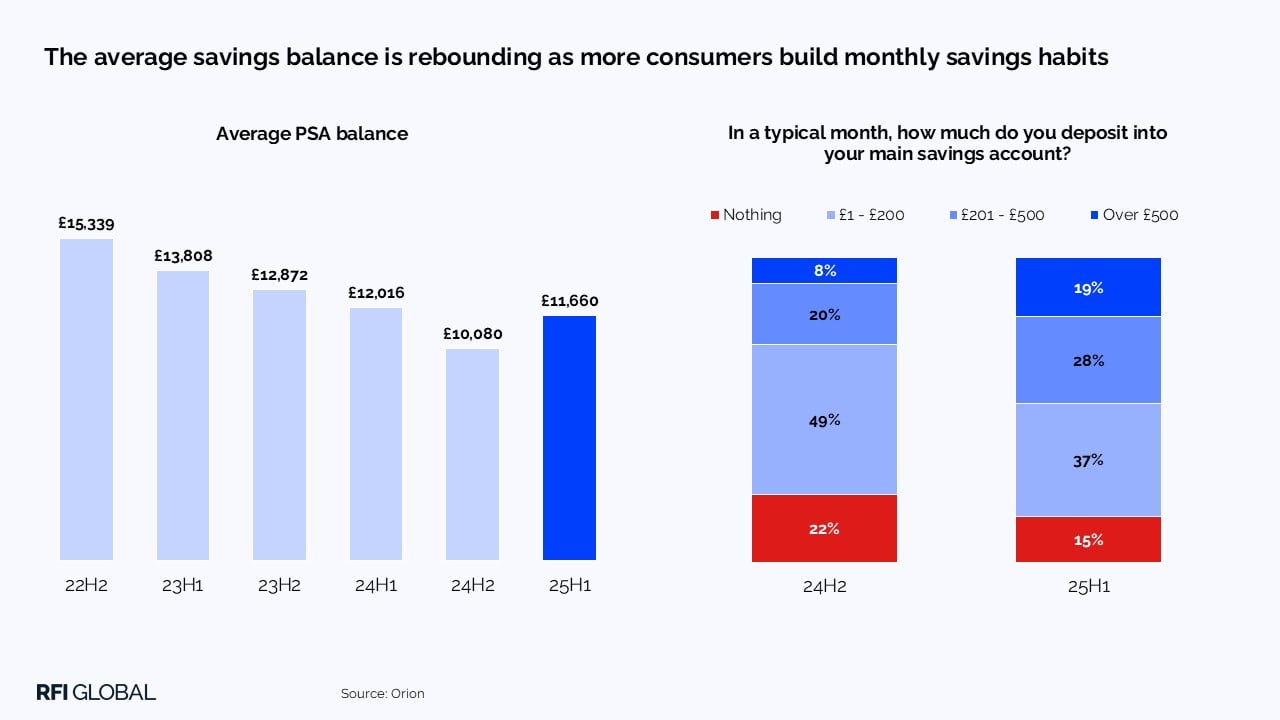

Savings are on the rebound

Despite lingering economic uncertainty, savings are on the rebound, signalling a positive shift in consumer finances. Earlier this year, RFI Global reported that piggy bank raids reached a 12-year high as consumers relied on savings and credit to cover essential costs.

Now, the tides are beginning to turn. Recent data from Orion, RFI’s extensive survey on UK financial behaviour, found that 3 in 10 UK consumers intend to increase their savings over the next year and they’re putting their money where their mouth is. Average savings balances are growing and more consumers are saving regularly.

Falling interest rates

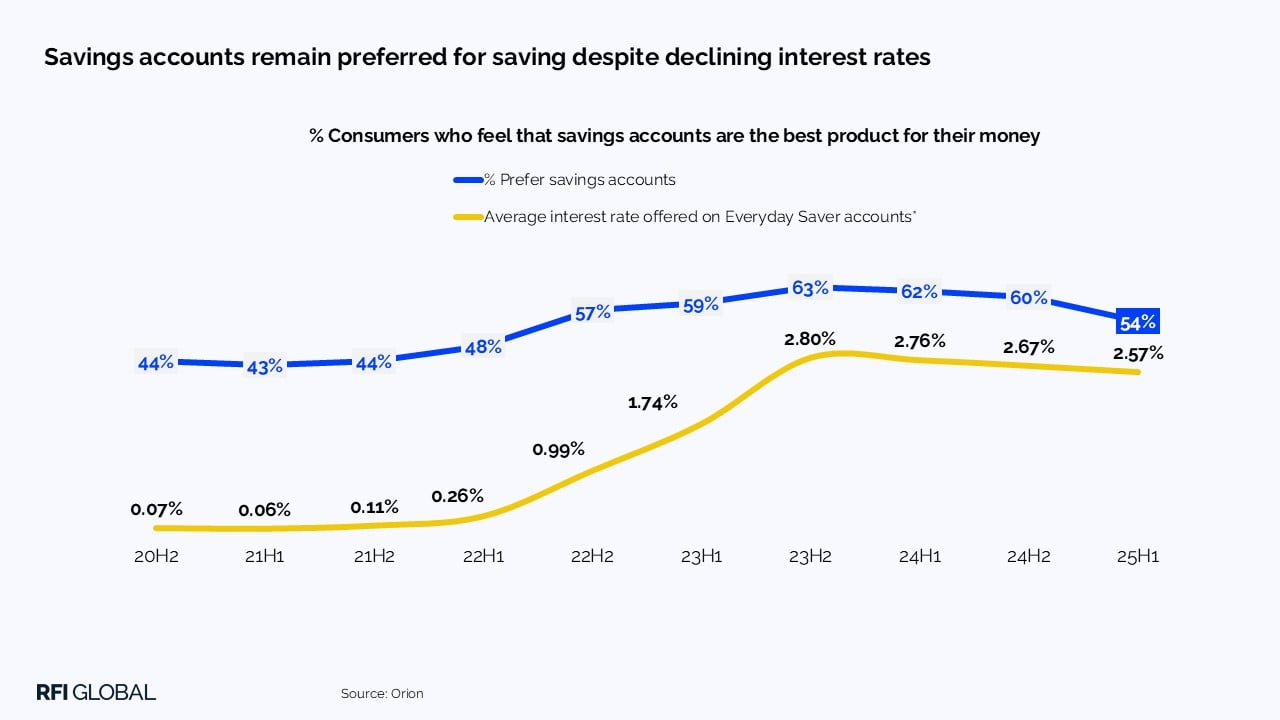

The timing couldn’t be worse. Consumers are more eager than ever to make their money work harder, evidenced by the latest Cash ISA figures from the Bank of England. This April, UK consumers placed a record £14 billion into Cash ISAs – a record high since the ISA’s launch in 1999. However, as the Bank of England cuts the base rate, returns are falling. Banks have rushed to cut their rates, prompting consumers to rethink their options.

Savings accounts remain the most popular way to save, but declining interest rates have soured this preference.

The switching surge

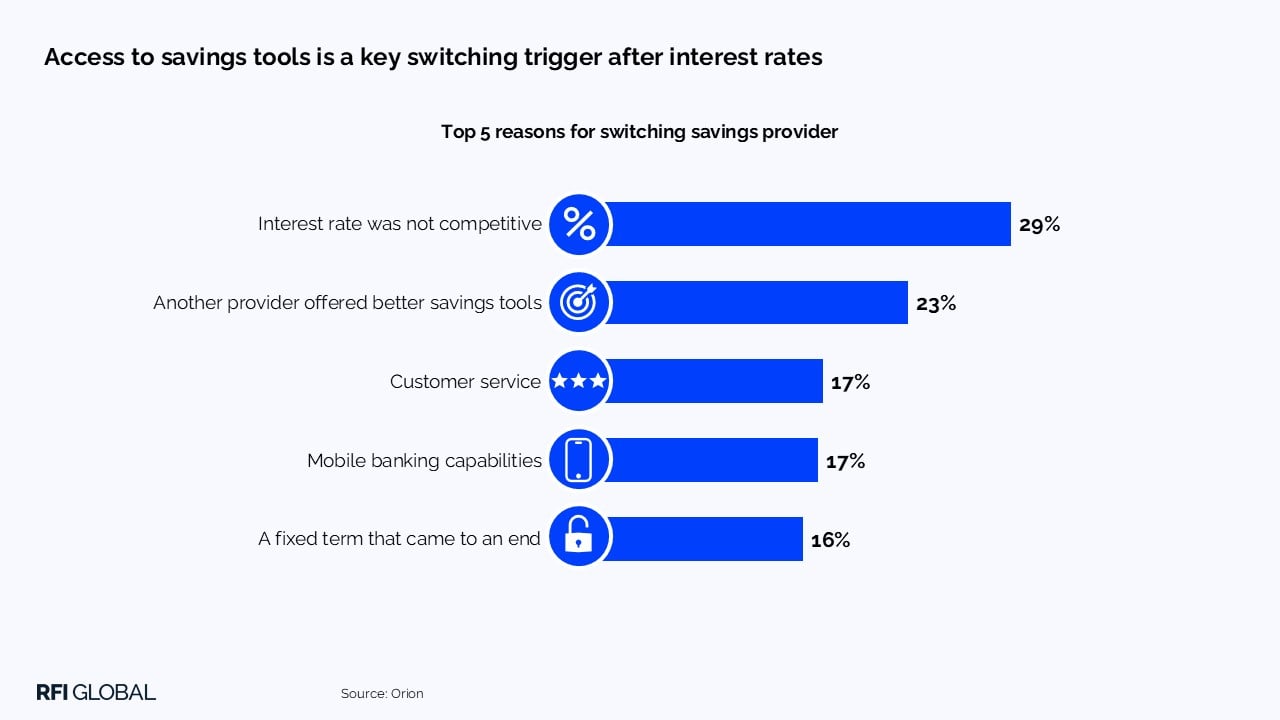

Although savings accounts remain popular, 44% of savers are looking to switch to another savings provider. This surge in switching activity presents a significant opportunity for banks to grow their share of the savings market. While there has been a drop in the number of savers considering a new account with their existing provider, banks needn’t despair. Look beyond the rate-chasing and banks will find that there is also an opportunity to help consumers navigate a shifting savings landscape.

With the right products and tools, banks can help consumers reach their long-term goals more effectively and develop a strong relationship that can outlast temporary bonus rates.

Traditionally, in lower-rate environments, the appeal of fixing savings accounts is high: lock your money away and take advantage of higher rates. With the cost of living still lingering, this option is off the table for many. According to our data, most consumers with fixed-term accounts do not intend to reinvest their money into another of these accounts.

Flexibility is a top priority for consumers; our data shows that 47% of savers have been dipping into their savings over the last 12 months. A happy medium is the instant access ‘reward savers’ on the market, where savers can enjoy higher interest rates for the months they avoid withdrawals. These accounts offer a clever incentive to help consumers balance their desire for higher interest rates with easy access to their savings. However, these offers rarely last forever, with most banks reverting to standard rates after the bonus period, leaving the door open for potential switching activity.

Empowering savers through mobile-first experiences

In our article, Five strategies for banks and fintechs, we outlined that the future success of banking lies in delivering exceptional customer experiences, driven by innovation and strategic incentives. The savings landscape is no exception.

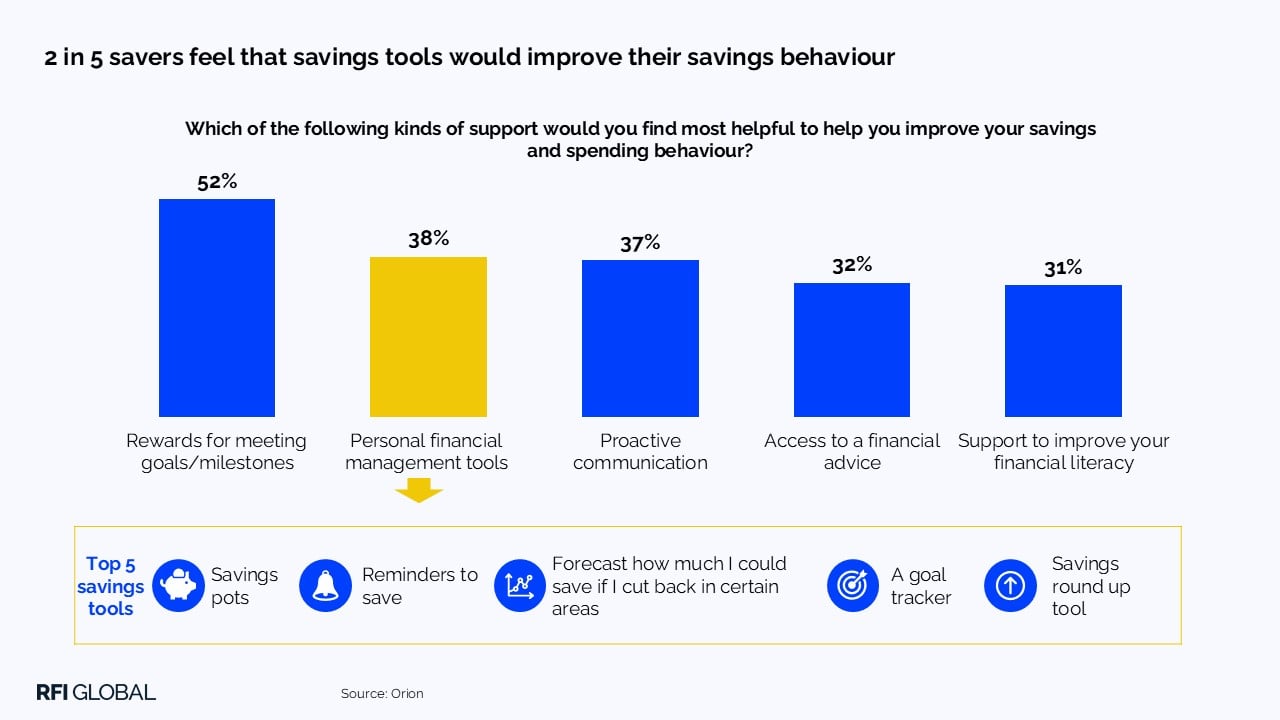

Consumers ultimately seek meaningful growth in their savings, and they need support to achieve that. While 53% of Baby Boomers may be satisfied with their monthly savings contributions, this drops to 10% and 14% among Gen Z and Millennials respectively. There is a significant opportunity to build loyalty by empowering savers with innovative money management and savings tools that make saving effortless.

Smarter money management

Take Monzo’s 1p Savings Challenge; by the end of January 2025, over 1 million savers had signed up. While interest on these pots is reserved for Monzo Perks and Monzo Max subscribers, the broader appeal lies in the gamified experience – users can track their progress and enter prize draws, making saving both structured and rewarding. Monzo handles all the legwork, making the transfers. Customers can sit back and watch their pot grow with their regular savings habit.

Simple experiences done right can be powerful. Banks must make it easier for consumers to build their savings and track progress toward their goals. Our data shows features such as savings pots are a key tool that savers value. It might seem old hat – neobanks have been doing this for years – but HSBC only announced its savings pots earlier this year.

These digital savings tools are not just nice-to-haves; they are an influential factor among consumers who choose to save with neobanks. What’s more, among those who’ve switched banks in the past three years, digital savings features rank just behind interest rates as key motivators. For Gen Z and Millennial consumers in particular, access to digital tools is equally, if not more, critical than the interest rate in the decision to switch. On the flip side, for consumers with no intention of switching, a well-designed digital banking experience plays a significant role in keeping savers engaged and loyal.

The implications for UK savings providers

As the savings landscape evolves, record numbers of savers are now looking to switch in search of the best rates. Promotional offers will always spark interest, but to succeed, banks must go beyond rates. Banks that embrace a mobile-first strategy, combining intuitive goal tracking, behavioural nudges, and flexible access, can turn everyday savers into loyal advocates:

1. Prioritise flexibility

With the cost of living still lingering, consumers will look for accounts that balance incentives with flexible access to their funds.

2. Invest in digital experiences

For Gen Z and Millennial savers, especially, the digital banking experience can make or break the relationship.

3. Support and reward good saving habits

Digital tools like savings pots, nudges and challenges help build savings habits and propel savers towards their goals effortlessly.

Greater transparency can also help banks secure their position as a trusted savings partner. In addition to notifying customers of better offers, they should offer guidance on savings products, clearly communicating features and making it easy to compare how different accounts will support savings goals.

Today’s savers are motivated, but they need smarter support. Banks that empower consumers to take control of their financial futures will be best placed to succeed in the shifting savings landscape.

Get in touch for more insights from the survey and find out more about Orion here.

UK savings trends: key questions answered

Q: Why are more UK consumers switching savings providers in 2025?

A: RFI Global’s Orion study of UK financial behaviour shows that 44% of savers are considering switching their providers. With falling interest rates and the end of introductory offers, consumers are actively shopping around for better returns and more flexible savings solutions.

Q: What do UK savers want from their savings accounts?

A: RFI Global data shows that UK savers are prioritising flexibility, ease of access and digital tools over traditional fixed-term accounts. Many are switching because they believe they can get better rewards and features elsewhere, not just higher interest rates, but also tools that support saving habits, like savings pots and reward-based incentives.

Q: How can banks retain savers in a low-rate environment?

A: RFI Global data shows that to retain and engage today’s savers, banks should:

- Offer flexible savings products with fair rewards

- Deliver mobile-first experiences that simplify saving

- Use digital features like goal tracking, nudges and gamified challenges

- Provide transparent, timely information about better rates and account features

Data-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.