Earlier this week HSBC in the UK announced it would not close any more branches in 2025. Also in the UK this week the CMA found that digital banks without a physical branch network – such as Monzo, Starling and Chase – did better than traditional lenders when it came to how likely customers were to recommend them to friends and family.

The phrase ‘the branch is dead, long live the branch’ has been bouncing around since 2015, and yet we still seem to be no further in understanding what role the branch will play in the future.

How is digital banking affecting branch usage?

In the UK 75% of consumers bank digitally first but when we break it down, this is almost entirely transactional behaviours. If we look at the reasons consumers, pre-pandemic, continued to visit branches then we see it was to talk to a human about a problem or an important or life-stage decision, as opposed to all the transactional behaviours they did digitally. As a result of the pandemic, consumers were forced away from this channel. The reliance on branches diminished significantly and video conferencing and chat became much more prevalent, thus further reducing the role of the branch.

In the US, RFI Global’s MacroMonitor data shows that in 2024 75% of millennials and Gen Z would rather rely on robo-advice than speak to bank staff.

In the UK Steve Weston, Head of Money Management at Barclays Bank, says in our Banking Uncovered podcast, that based on their 20 million customers, 75% of under 30s and 60% of all customers want a digital-only bank experience and “under 30s don’t want to talk to a human.” Branches are closing and the race to acquire Gen Z is heating up with fintechs also competing heavily and successfully in this space.

So, the need for branches is reducing, surely?

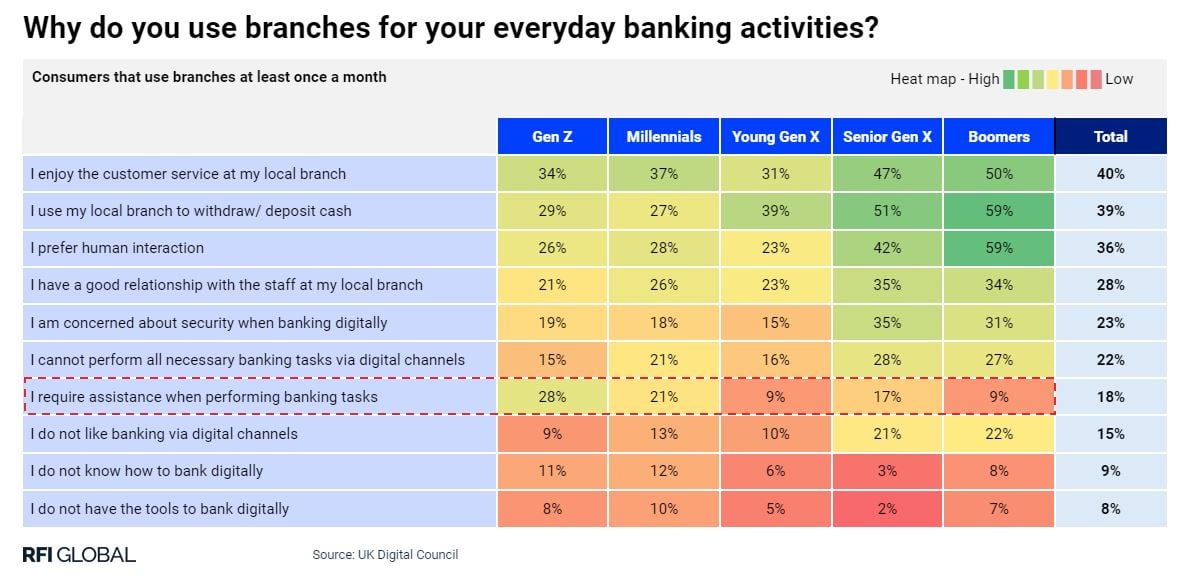

A third of Gen Zs want innovative services at their branch. RFI Council data shows that Gen Z are the heaviest users of branches with 42% of Gen Z using it on a monthly basis, higher than any other UK demographic.

One of the reasons for Gen Z’s reliance on the branch is that according to RFI data, 20% of Gen Z and Millennials don’t have the tools to bank digitally or don’t know how to bank digitally and a surprising 25% require assistance when performing banking tasks digitally, in both cases more than any other UK demographic.

So, what is going on?

Historically the branch was the number one channel. Even in 2024, RFI data shows that the branch is still the main driver of customer satisfaction. All other channels – ATM, phone, online and mobile have been secondary and subservient to the branch. They have been supporting channels for the main channel – the branch.

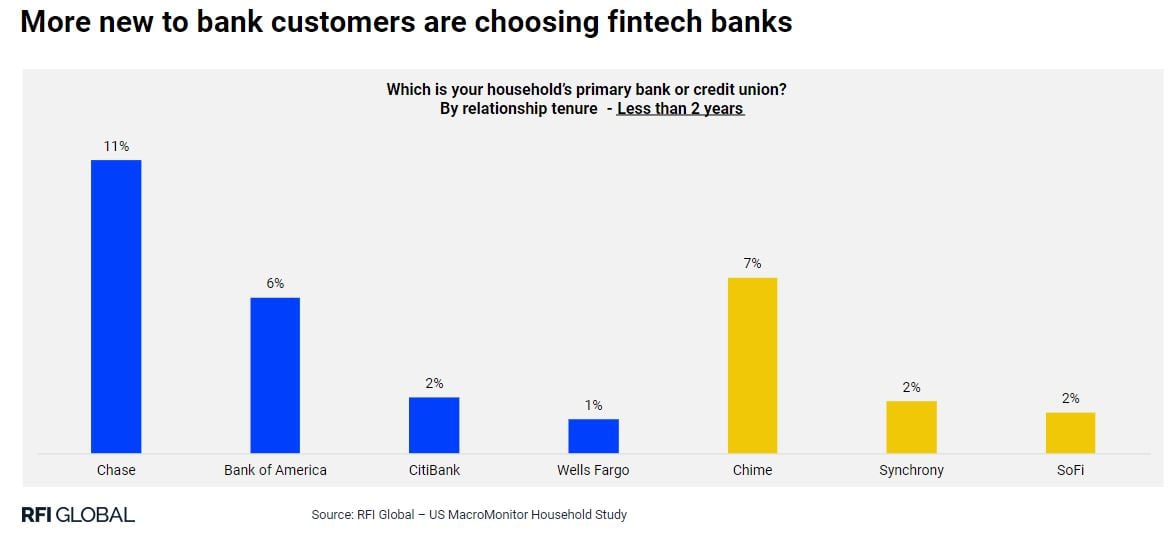

Fintech uptake continues to increase – Monzo just passed 10 million customers. In the USA Chime and Synchrony onboarded more new-to-bank customers in the last 2 years than Bank of America and Wells Fargo combined.

Digital banking and mobile wallet usage continue to grow at pace. The result of these factors is that the dominant main channel is now digital. The branch has moved into a support role. As the first chart shows Gen Z and Millennials now go to the branch not for a life-stage decision but to be coached in how to perform banking tasks and how to bank digitally. Once this support function is no longer necessary the branch need reduces further.

But what about Gen X and Baby Boomers?

They already know how to perform these tasks. Steve says that there is a cohort “where there is something in my psyche that if I need to go and talk to someone there is a branch in the high street.” He goes on to say that “for the incumbents, it is about leveraging your history, age and physical branches combined with looking at how the challengers are doing such a good job with the younger demographic.” This undoubtedly combines the best of both worlds, as I’ve discussed in previous blogs. The new game changer is AI.

What does the future hold for branches?

As Generative AI, AI and avatars continue to grow, and at the moment we have barely even scratched the surface, will that psychological need referred to by Steve finally dissipate? Who now still goes to a bookstore to buy a book? How many people insist on doing their weekly grocery shop in store?

One of the other reasons for talking to a human in a branch was for investment decisions. RFI’s MacroMonitor data shows that in the US 40% of households would now trust all their wealth to a robo-advisor. Steve talks about the need of the younger generation “for ever greater and greater personalisation.”

As the capabilities of AI continue to further increase personalisation, will there still be a need for contact with a branch even as a support channel? While I agree that the combination of the security and risk compliance and stability of the incumbents combined with the personalisation and UX of the digital players will be a winning combination, it appears that AI, if it can continue to develop to the point where it provides an almost human touch, might finally remove the need for the physical branch even as a support channel.

Subscribe to get the latest RFI data and insights.

Data-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.