Stefano Colombu, Managing Director, Asia

RFI Global’s Financial Services Trends & Predictions 2026 report draws on insights from over 200,000 consumers and 60,000 businesses globally, alongside thousands of real digital banking interactions, to identify the five trends set to define financial services in the year ahead. While global in nature, the trends play out differently by market based on maturity, regulation, infrastructure and consumer behaviour. This article explores how these trends are evolving in Hong Kong, and where the market diverges from global peers based on insights from over 2,000 Hong Kong consumers.

As a highly digital, internationally connected financial hub, Hong Kong consumers demonstrate strong adoption and engagement with emerging technologies. The market is also highly concentrated, dominated by large institutions such as HSBC, Bank of China (Hong Kong), Citi and Standard Chartered and a wide array of smaller financial institutions and digital banks. It also acts as a gateway between Mainland China and international markets.

1. From curiosity to confidence: Trust in AI-powered finance

As AI becomes embedded in everyday life, financial institutions are accelerating its use across customer interactions. Globally, however, concern remains high.

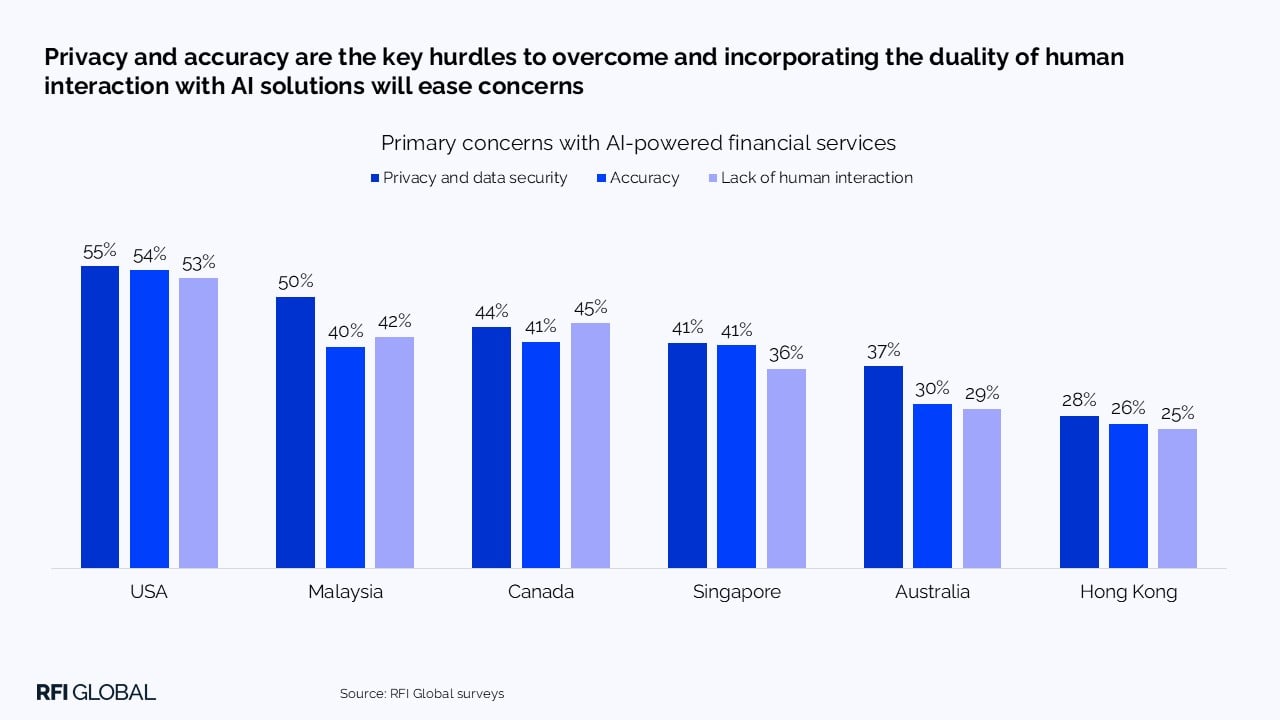

In Hong Kong, while 80% of consumers report some level of concern, this is lower than other markets (Singapore 95% and Australia 94%). Privacy, accuracy and lack of human interaction are the main global concerns, but Hong Kong consumers consistently report fewer concerns across all three dimensions, indicating a higher baseline acceptance.

Further, around three-quarters of consumers are interested in AI-driven tools such as virtual assistants, predictive insights and fraud detection, and half (52%) are open to AI-supported loan approvals.

Hong Kong’s lower resistance creates a favourable environment for adoption, but trust remains critical. Institutions that combine rapid deployment with transparency and clear governance will be best positioned to convert openness into sustained usage.

2. Digital user experience (UX): The key battleground for customer loyalty

Digital experience has become a key differentiator in financial services. As mobile has overtaken online as the primary banking channel, customers expect seamless, intuitive and secure interactions – and are increasingly willing to switch when these expectations are not met.

In Hong Kong, this shift is particularly pronounced. High mobile adoption and strong infrastructure mean that for many customers, the app is the bank. Expectations now centre on speed, simplicity and control, rather than basic functionality.

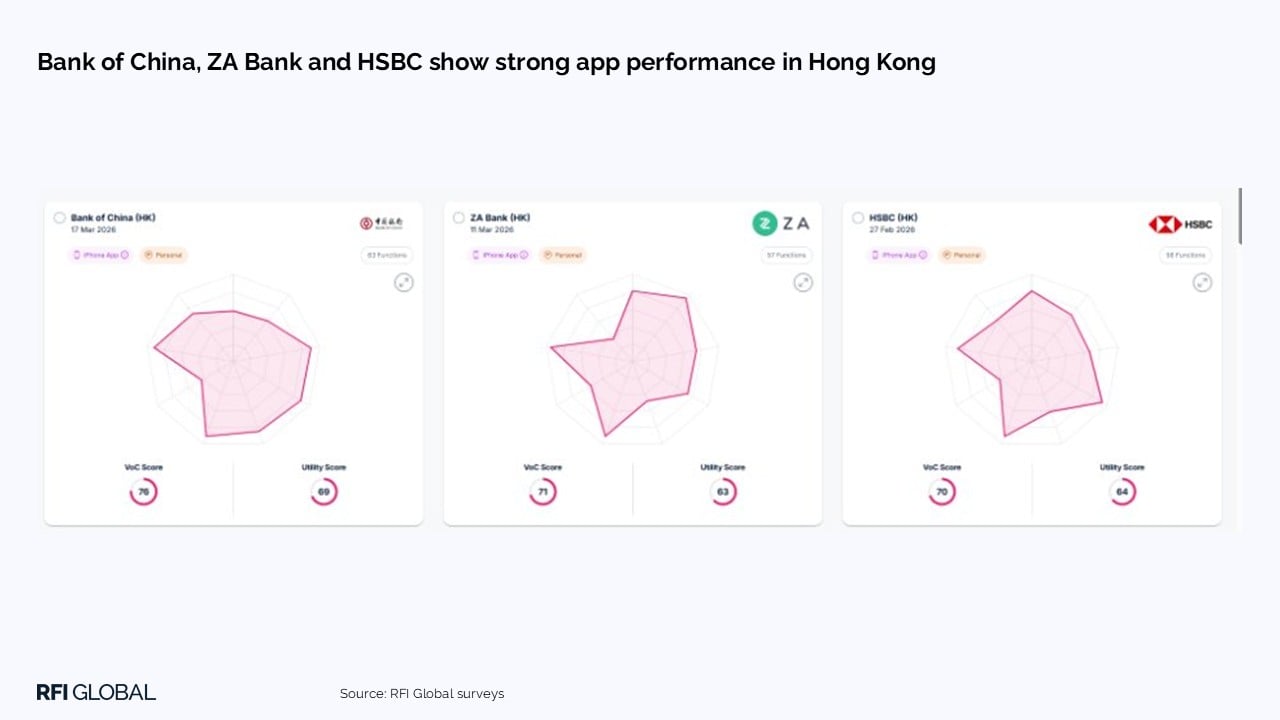

Security remains a significant focus across Asia. Leading Hong Kong banks are deploying pages that allow customers to track and respond to events like contact changes, statement downloads, or new payees, providing greater visibility, control and real-time functionality and empowering consumers.

Insights from RFI Global’s iSky Radar platform highlight strong digital performance across a mix of regional, local and global players, including Bank of China, ZA Bank and HSBC.

As digital becomes the primary relationship channel, competitive advantage will increasingly be defined by the quality and consistency of the experience, with loyalty driven by ease, speed and control rather than brand alone.

3. The next chapter for neobanks: From growth to value

Globally, neobanks are shifting from rapid customer acquisition to sustainable growth, with a greater focus on engagement, monetisation and profitability.

In Hong Kong, the region’s neobanks are focusing on customer value and product diversification to drive sustainable growth. ZA Bank became the first to report a monthly profit in 2024, with deposits and transaction volumes rising sharply.

This trend is also reflected in the evolution of Hong Kong’s virtual banking sector. Following an initial phase focused on scale, virtual banks are narrowing losses and expanding into wealth management. While this mirrors developments in more mature markets such as the UK and US, Hong Kong remains earlier in the maturity curve, with significant room for growth.

The competitive focus is now shifting from acquiring customers to deepening relationships, requiring both virtual banks and incumbents to broaden their propositions and compete more effectively for share of wallet.

4. Cybersecurity: Fraud has evolved, but have banks?

As fraud and cybersecurity threats become more sophisticated, expectations of how banks respond are rising.

In APAC, and particularly in Hong Kong, consumers are more comfortable with the use of AI in fraud prevention. Three-quarters of Hong Kong consumers (74%) are open to AI-driven protection, alongside 70% in Malaysia and 68% in Singapore – significantly higher than the US (23%). This signals a clear opportunity for banks to accelerate the deployment of advanced technologies in this space.

However, this openness is not translating into satisfaction. Just 15% of Hong Kong consumers are satisfied with their primary bank app’s security features, and 9% have switched their main bank due to dissatisfaction with fraud handling.

Fraud prevention is no longer just a risk function; it is a core driver of trust and retention. Banks that make security visible, intuitive and responsive will be better positioned to build trust and retain customers.

5. Wealth in 2026: Unlocking fee-based growth as affluent investments rise

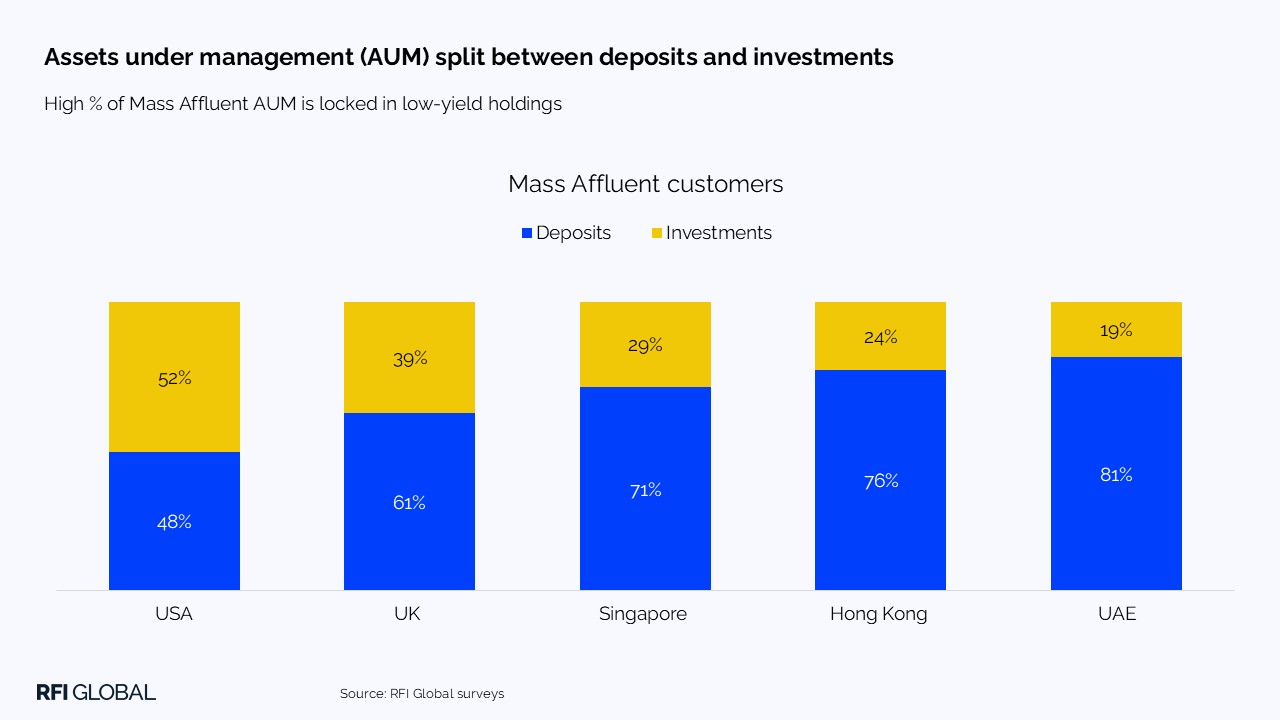

Around the world, the majority of wealth is held by a small proportion of affluent consumers. And globally, a significant proportion of this wealth remains held in deposits, creating an opportunity for financial institutions to drive greater investment participation and support evolving wealth needs.

In Hong Kong, this trend is amplified by the market’s role as a cross-border financial hub. Consumers are not only seeking returns but also diversification and access to a broader range of investment opportunities, particularly across the Mainland China-Hong Kong corridor.

At the same time, the core global challenge remains – 76% of Mass Affluent consumers’ assets in Hong Kong are still held in low-yield savings.

This presents a clear opportunity for institutions to convert deposits into investments, supported by more integrated, personalised and cross-border wealth propositions.

Conclusion: a market defined by speed, sophistication and global connectivity

Hong Kong reflects our global financial services trends, but with greater intensity. Customer expectations are evolving rapidly, with increasing demand for seamless, secure and intuitive experiences.

For financial institutions, this raises the bar. Success will depend on the ability to execute quickly, deliver high-quality digital experiences and meet increasingly complex customer needs across borders.

In 2026, the winners will be those who translate global innovation into locally relevant, trust-led experiences at scale.

Download the full report for detailed trend analysis, and to see how Hong Kong compares to other key financial markets.

Stefano Colombu

Managing Director, Asia

Stefano Colombu is Managing Director, Asia at RFI Global, leading the firm's research and advisory work across Asian markets.

View full profileFrequently Asked Questions – Financial service trends in Hong Kong

Q: What are the key financial services trends in Hong Kong for 2026?

The key financial services trends in Hong Kong for 2026 are AI adoption in banking, digital user experience as a key driver of loyalty, the shift of neobanks towards sustainable growth and profitability, rising expectations around fraud prevention, and wealth management growth as more assets move from savings into investments.

Q: How open are Hong Kong consumers to AI in banking?

Hong Kong consumers are more open to AI in banking than many global peers. While 80% report some concerns, this is lower than Singapore (95%) and Australia (94%). Around three-quarters are interested in AI-driven tools, and 52% are open to AI-supported loan approvals.

Q: What do Hong Kong consumers want from digital banking?

Hong Kong consumers want digital banking experiences that are fast, seamless, secure and easy to use. With mobile now the primary banking channel, expectations have moved beyond basic functionality to intuitive app journeys that provide greater control and real-time visibility. Customers are also more willing to switch providers if these expectations are not met, making digital experience a key driver of loyalty.

Q: How satisfied are Hong Kong consumers with their bank’s security and fraud protection?

Customer satisfaction with banking security in Hong Kong remains low. Only 15% of consumers are satisfied with their primary bank’s app security features, and 9% have switched their main bank due to dissatisfaction with how fraud was handled. This highlights the growing importance of visible, responsive and effective fraud prevention in driving trust and retention.

Data-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.