Stefano Colombu, Managing Director, Asia

As we start 2026, Singapore’s financial services sector stands at the crossroads of rapid digital transformation, evolving consumer expectations and intensifying competition. Our Financial Services Trends and Predictions 2026 global report identifies five trends that will shape the year ahead for the financial services industry. Drawing on RFI Global’s latest APAC research, this article explores what these trends mean for the future of banking in Singapore and the implications for financial institutions and consumers alike.

Trend 1. From Curiosity to Confidence: Building trust in AI-powered finance

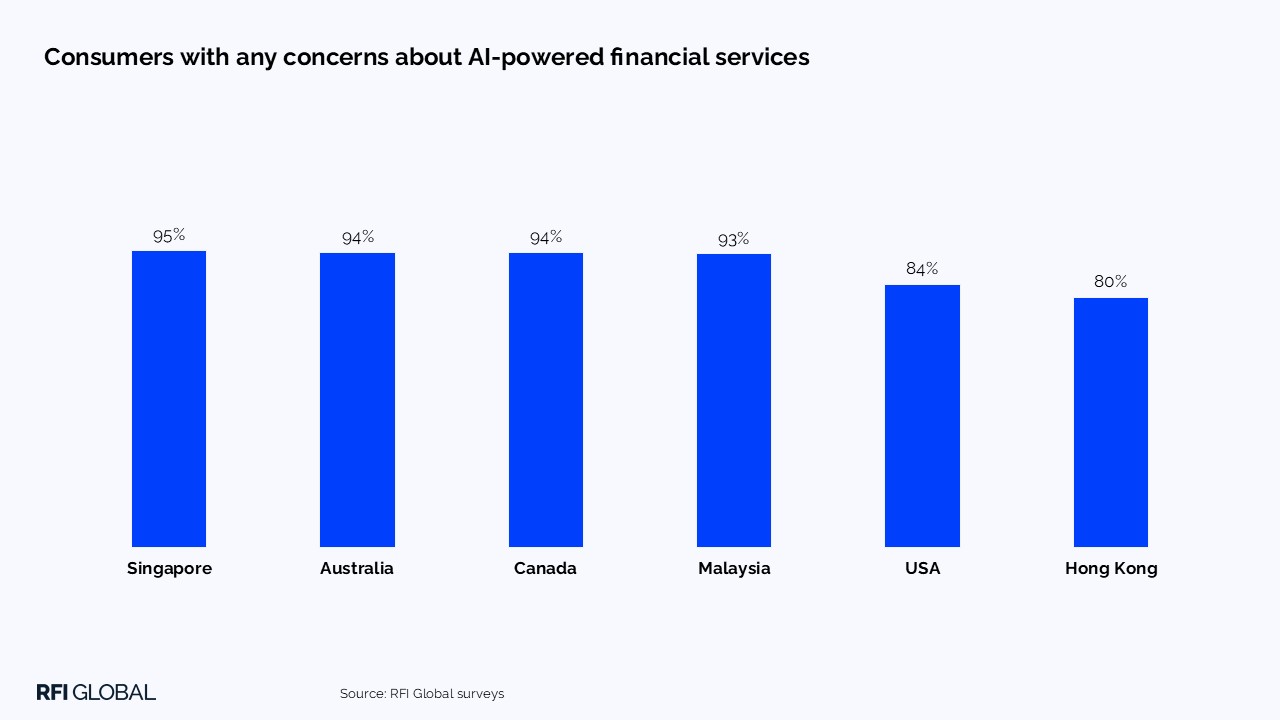

AI is rapidly moving from novelty to necessity in Singapore’s banking landscape. While consumers are increasingly open to AI-powered tools, such as virtual assistants, fraud detection and predictive analytics, trust and transparency remain critical hurdles. In Singapore, a striking 95% of consumers express concerns about using AI with their bank, with privacy and data security topping the list. Two-fifths also worry about the accuracy of AI-based decision-making.

Transparency is key: 34% of Singaporean consumers say clear explanations of AI’s benefits and limits would boost adoption. Banks that offer hybrid models, combining AI efficiency with human support, will differentiate themselves in a crowded market.

Highlighting the balance between innovation and customer trust in AI, Natalia Goh, CEO of MariBank and member of Singapore’s Government Technology and Innovation Committee, explained on our Banking Uncovered podcast:

“Gen AI has been a very exciting development in general for everyone, and I think for banking, the full potential really still remains to be seen in terms of how we think about the use cases for Gen AI or AI more broadly in banking… At MariBank, we’re still in very early stages of exploration… we want to be very careful when it comes to Gen AI in terms of handling direct customer interactions because for us, customer experience is really important, so when we roll these out, we want to make sure that we’re not compromising customer experience when we use Gen AI.”

– MariBank’s Natalia Goh

Trend 2. Digital user experience (UX): The key battleground for customer loyalty

Mobile banking has overtaken online banking as the main interface for financial management in Singapore. The app is now the bank, and digital user experience is evolving at an extraordinary speed. Security features like locks on funds and enhanced verification are gaining prominence, with Singaporean banks leading in rolling out protective features that prevent transactions until additional checks are completed.

Payment innovation is also accelerating, with over 27% of banks in the region incorporating QR code payments and pre-login payment options. As digital empowerment becomes the norm, banks must deliver seamless, secure and personalised journeys to win customer loyalty.

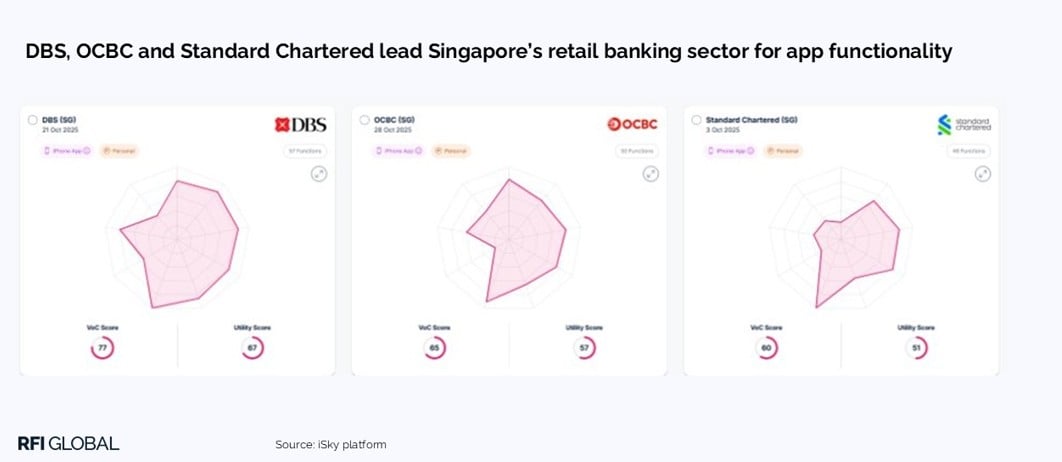

Analysis from our iSky platform, which tracks thousands of real consumer interactions with banking apps globally, shows that DBS, OCBC and Standard Chartered lead Singapore’s retail banking sector, achieving the highest Voice of the Customer score, a key measure of app functionality and user experience.

Trend 3. The next chapter for neobanks: From growth to value

Neobanks in Singapore have experienced exponential growth in their customer bases over the past four years. The focus is now shifting from rapid acquisition to deeper engagement and sustainable profitability. Product diversification, expanding into savings, credit, wealth management and insurance, is driving usage and retention. Strategic partnerships and AI-driven personalisation are becoming key differentiators.

Trust Bank leverages a supermarket loyalty ecosystem (FairPrice/Linkpoints) for targeted rewards, highfrequency engagement and lowcost acquisition, focusing on mass retail deposits/cards/payments.

GXS Bank cross-sells to ridehailing, deliveries and mobile subscribers, focusing on simple savings, microsavings/’pockets’ and entrylevel credit.

As neobanks evolve into full-service financial institutions, their ability to deliver integrated experiences and innovative solutions will be crucial in capturing greater wallet share and reshaping customer expectations.

For traditional banks in Singapore, this raises the bar on digital experience, speed to market, and ecosystem integration. Incumbents will need to modernise data and core platforms, deploy AIdriven personalisation with strong model governance, and deepen partnerships (e.g., with retailers, telcos and platforms) to remain the primary relationship for everyday banking.

Trend 4. Cybersecurity: Fraud has evolved, but have banks?

Fraud is evolving faster than ever, driven by AI, digital tools and sophisticated scams. In Singapore, 8% of consumers who are considering switching their main banking relationship cite dissatisfaction with their bank’s response to fraud as a key reason. Only 17% of Singaporean consumers are wholly satisfied with the security features of their primary bank’s app, highlighting a major opportunity for improvement.

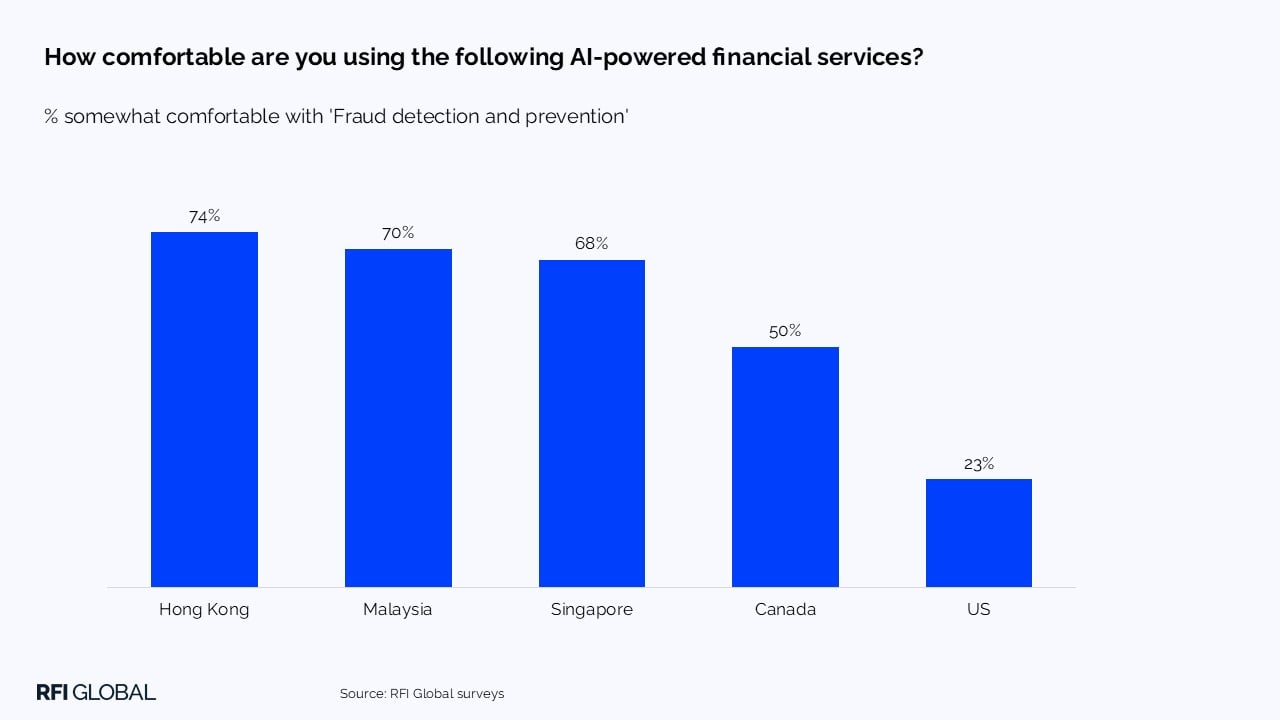

Asian consumers are among the most receptive to financial institutions using AI for fraud detection and prevention, with 68% of Singaporeans somewhat comfortable with these solutions. Financial institutions must harness AI, share intelligence across industries, and balance friction with trust to stay ahead of increasingly inventive fraudsters.

The tension between stronger security and seamless customer experience is also reflected in how institutions think about digital relationships. Gourab Kundu, Citi Wealth’s head of digital growth for Asia South, based in Singapore, explains on our Banking Uncovered podcast:

“Cybersecurity is such a huge topic at the moment. But you’re talking about continuing digital innovation within the overall customer experience. And that leads on to relationships. Because relationships are a pain point. And satisfaction and service levels from RMs are the number one driver of poor NPS results in the mass output space. It’s a conundrum because you have to achieve that balance, which, as you say, again, is very personalised.”

Trend 5. Wealth in 2026: Unlocking fee-based growth as affluent investments rise

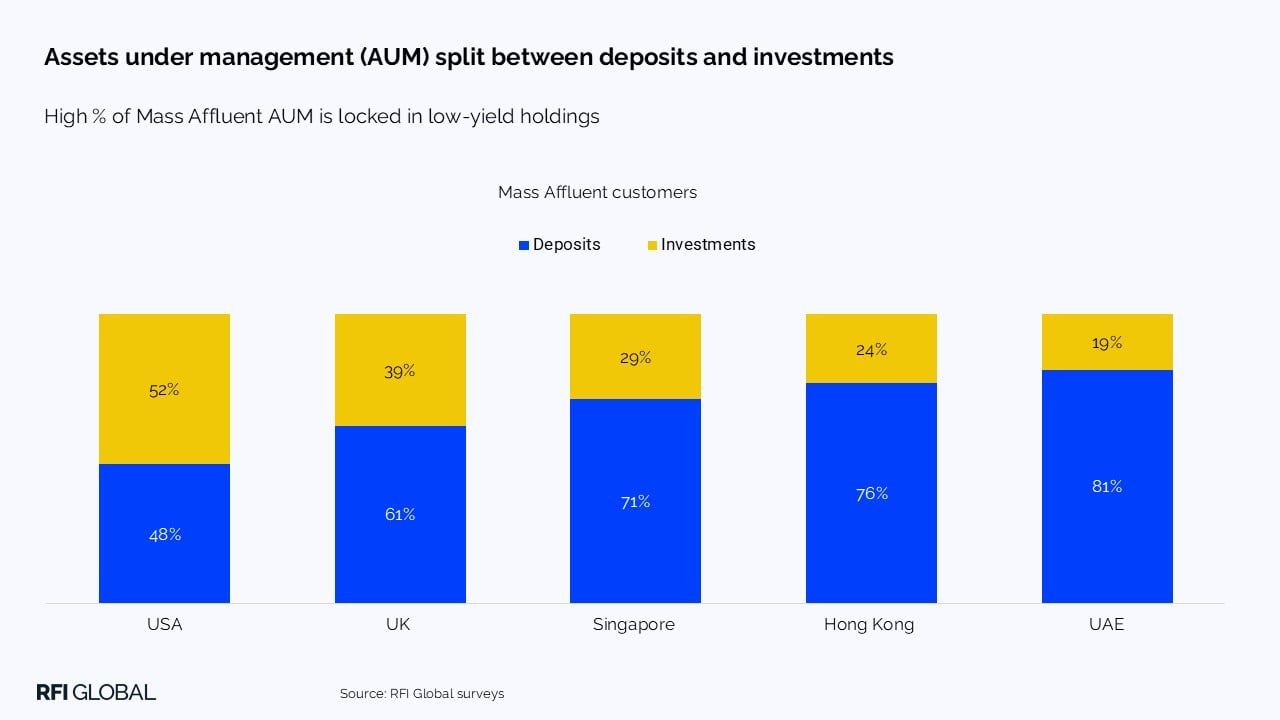

Singapore’s affluent consumers are leading a global resurgence in investment intent, with 41% open to reallocating funds from savings into portfolios as rates decrease. Despite this, 71% of affluent consumers’ liquid assets remain parked in low-yield deposit products, signalling a major conversion opportunity for banks.

Winning in 2026 will require banks to deliver seamless, personalised, and insight-driven offerings that encourage movement from deposits to higher-return portfolios. Fee-based income will grow for institutions that get conversion, visibility and experience right.

What’s Next for Financial Services in Singapore?

2026 will be defined by the intersection of trust, technology, and transformation. Success will belong to financial institutions that combine innovation with integrity, using AI responsibly and delivering experiences that feel both human and high-tech. As digital maturity and customer-centricity become the new benchmarks, banks must evolve from custodians of cash to architects of their customers’ financial futures.

For a deeper dive into these trends and their implications for financial services, download the full report or reach out to your local RFI Global expert to explore how they can shape your strategy.

Stefano Colombu

Managing Director, Asia

Stefano Colombu is Managing Director, Asia at RFI Global, leading the firm's research and advisory work across Asian markets.

View full profileFrequently Asked Questions about the future of banking in Singapore

Q: What are the major banking trends in Singapore for 2026?

In 2026, Singapore’s banking sector will be shaped by rapid AI adoption, enhanced digital user experiences, the maturation of neobanks, evolving cybersecurity strategies and new opportunities in wealth management for affluent consumers.

Q: What opportunities exist for wealth management in Singapore in 2026?

Affluent Singaporean consumers are showing renewed investment intent, moving funds from low-yield deposits into portfolios. Banks that offer personalised, insight-driven, and seamless investment experiences can grow fee-based income and capture greater wallet share.

Q: Why is cybersecurity a key focus for Singaporean banks?

As fraud becomes more sophisticated, banks must balance robust AI-driven security with frictionless user experiences. Consumers increasingly expect real-time protection and clear communication, making cybersecurity a strategic differentiator.

Q: How are neobanks evolving in Singapore?

RFI Global research indicates that Singapore’s neobanks are shifting from rapid customer acquisition to deeper engagement, product diversification and AI-driven personalisation to drive sustainable growth.

Data-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.