Luke Allchin, Director, North America

The evolving demands of modern banking consumers will force incumbent banks in the United States to adapt to remain competitive in a rapidly changing banking landscape.

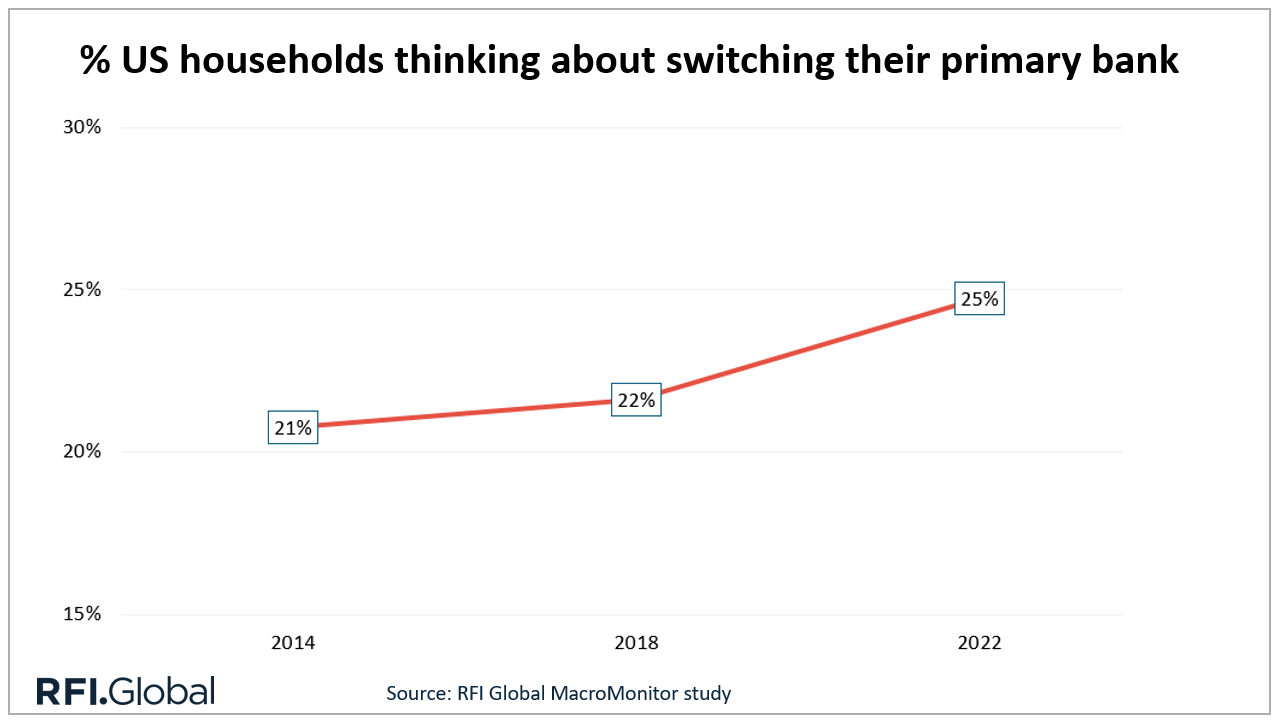

In recent years, the banking landscape in the United States has undergone significant change. In a market where the average relationship with the primary bank is 16.6 years, and over two-thirds of households established their banking relationship over two decades ago, yet 25% of households are at least thinking about switching their primary bank if not actively looking.

Driven by the amalgamation of digital innovation, growing customer expectations, and cost considerations, more households than ever before are likely to switch their primary banking provider.

Exploring the factors behind this trend with insights from RFI Global’s MacroMonitor study uncovers valuable insights into the evolving demands of modern banking consumers. It shines a light on incumbent banks, and their need to adjust to stay competitive in an ever-changing banking landscape.

The impact of digital banking

Technology has revolutionized the way people interact with their banks. And one of the most prominent drivers of increased switching behavior is the rapid advancement of digital banking.

Digital banking platforms offer unparalleled convenience; convenience that tech-savvy consumers find particularly appealing. The features provided by digital banking platforms go beyond basic transactions. Real-time transaction alerts, budgeting tools, and personalized financial insights – tools that help consumers make informed financial decisions and manage their money more effectively – have become greatly desired. As a result, banks that fail to offer a robust digital experience risk losing customers to their more technologically advanced competitors.

In addition to digital innovation, customer experience has become a critical factor in the decision-making process. People are increasingly prioritizing customer service when choosing their banking providers. Our data shows that in the US, banks that offer superior customer support, often facilitated through digital channels like chatbots and 24/7 customer service, are more likely to attract and retain customers. Prompt and effective resolution of issues is crucial in building trust and loyalty.

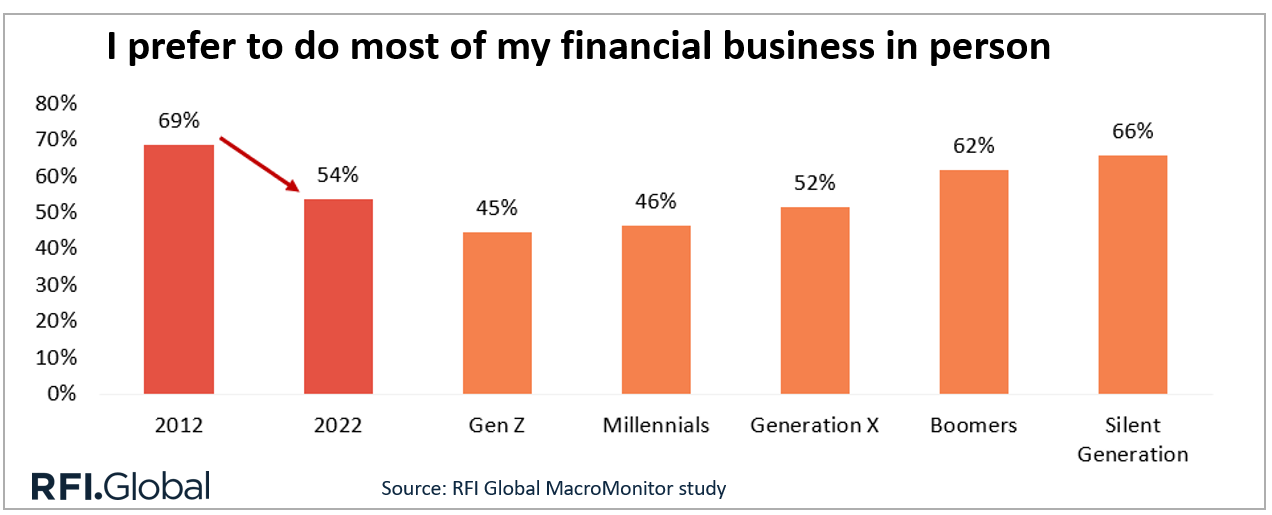

Personalization is another key aspect of the customer experience. Banks that leverage data analytics to offer tailored financial advice and personalized product recommendations are more attractive to consumers. Personalized experiences make customers feel valued and understood, enhancing their overall satisfaction. Again, this ties into technology and the extent to which banks are investing in digital innovation. Since fewer people prefer to manage their finances in person, digital personalization is becoming key to retaining that personal touch.

What about the cost of banking?

In a time where households face rising rent, bills, and general living costs, financial competitiveness is unsurprisingly another significant factor driving switching.

Choosing to bank with one of the larger incumbent banks can come with a range of fees, from account maintenance to ATM fees. Some consumers look to digital-only banks as they are often perceived to offer lower fees for basic banking services. This cost advantage of banking small is a compelling reason to switch for some consumers.

And the importance of digital innovation?

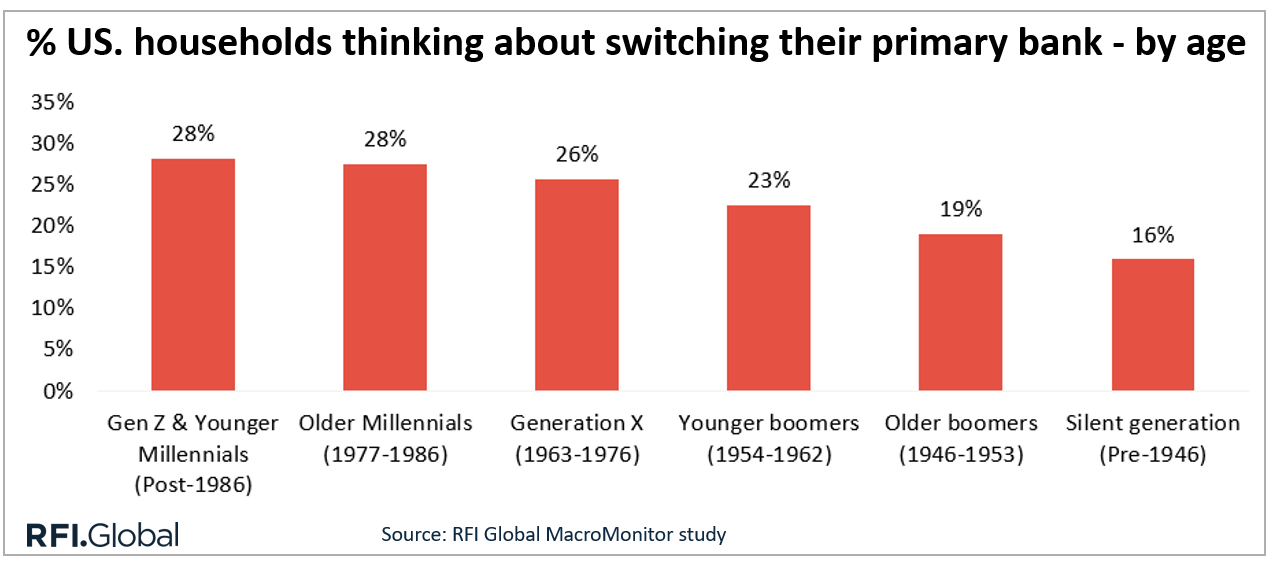

There is a recurring theme around switching. In one way or another, it comes down to a bank’s ability to deliver meaningful digital and technological innovation to its customers. Digital servicing is deeply ingrained in the lives of young consumers. As a result, switching intentions are higher among younger households in the US, rising to 28% of Gen Z and Millennial households.

The trend of switching banks can be characterized by a notable shift from the larger incumbent banks in favor of digital-only banks, such as Chime, Synchrony, and SoFi. For many, these digital-only banks offer superior digital experiences, lower fees, and innovative features that appeal to US consumers. The ease of account management and the availability of advanced tools make digital-only banks an attractive alternative to the larger incumbent banks.

Despite the rise of digital banking, the ability to speak with a knowledgeable representative is still invaluable for many, which is why physical branches remain important to some households. For more complex banking needs, such as applying for a loan or seeking financial advice, consumers often prefer in-person channels.

While it is true that the human element of banking cannot be entirely replaced by digital interactions, especially for customers who value personal connections, the delivery of effective live chat and video chat services is certainly helping to bridge that gap.

National banks vs. digital-only banks

Now, I don’t expect the digital-only banks to unseat the national banks, such as Wells Fargo, Chase, and Bank of America, anytime soon. However, the US retail banking market does look different when we focus on new-to-bank relationships and the effects of recent customer switching activity.

Focusing on households that opened their primary bank account within the last two years we see Chime accounting for 7% of primary banking relationships, a greater share than Bank of America and Wells Fargo. Collectively, Chime, Synchrony, and SoFi account for 1 in 10 primary bank accounts opened in the last two years.

A significant shift in preference among US consumers

The increase in switching behavior among US banking consumers is driven by a desire for better digital experiences, lower costs, and most importantly superior customer service. While digital banking plays a crucial role in this shift, physical branches are still relevant for certain banking needs and customer demographics. Banks that can strike a balance between digital innovation and excellent customer service, with personalized experiences will be best positioned to attract and retain customers in this evolving retail banking landscape.

Get in touch for more insights from MacroMonitor. Based on over 5,000 interviews, MacroMonitor provides the most comprehensive insights into US financial services behavior across all household financial products.

Subscribe to get the latest RFI data and insights.

Luke Allchin

Director, North America

Luke Allchin is a Director, North America at RFI Global, leading financial services research and advisory across the North American market.

View full profileData-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.