Migration is firmly back on the agenda in 2024. The media is giving it plenty of airtime, driven by discussions around housing shortages and employment. Last year I wrote an article on new arrivals to Australia and the opportunities open for banks and financial institutions to ensure that they better targeted and serviced this influx of new customers. I referenced RFI Global’s 2017 study of recent migrants and anticipated our updated survey, which we undertook at the end of 2023 encompassing more than 600 recent arrivals (who have moved in the last five years), and 400 prospective migrants who are moving to Australia in the next 12 months.

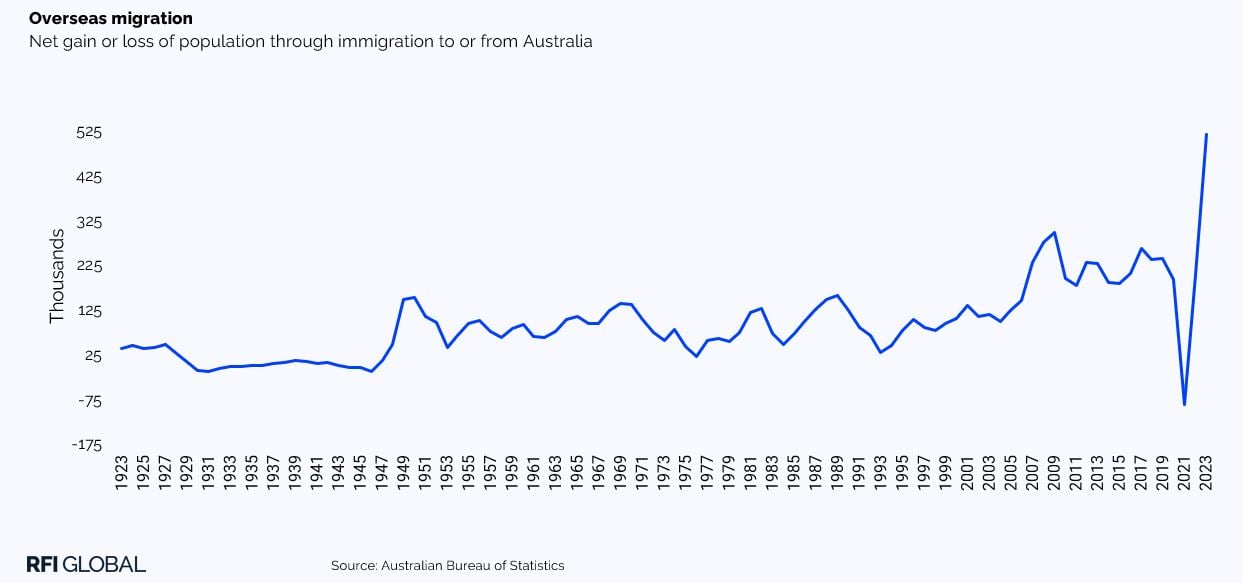

There is no doubt that net migration has seen a stark recovery since the pandemic, with net overseas migration reaching 518,090 in FY23 and more than 713,000 individuals arriving in the country. This figure is significantly higher than before the pandemic when net migration never exceeded 300,000.

How to win hearts and minds

With so many new arrivals to Australia, it’s no wonder the banks are seeking to understand how they can best meet their needs. This is particularly important when you consider that our study shows that more than 90% of migrants moving to the country stick with their first bank account provider for the long haul.

Of course, being first is easy to say, but how does a bank ensure that it has the best chance of being that first bank? Over the last couple of decades, there has been an airport signage war, which was dominated first by HSBC and in more recent times by CBA. This attempt to be the first bank seen upon arrival is understandable, but does it lead to actual patronage?

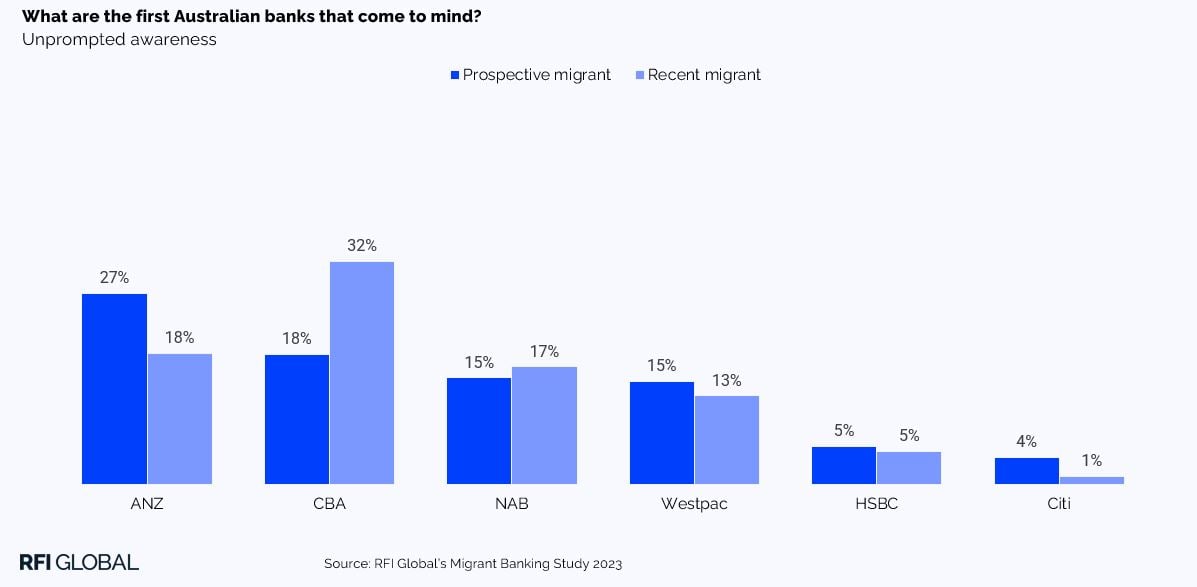

Our study shows that it could well have an impact on awareness. A comparison of banking brands that recent arrivals are most familiar with vs prospective migrants shows that the number one brand for those moving to the market is ANZ, with 27% saying it’s one of the first brands that comes to mind. However, for those recently arrived, CBA dominates, with 32% saying it’s one of the first banking brands they think of.

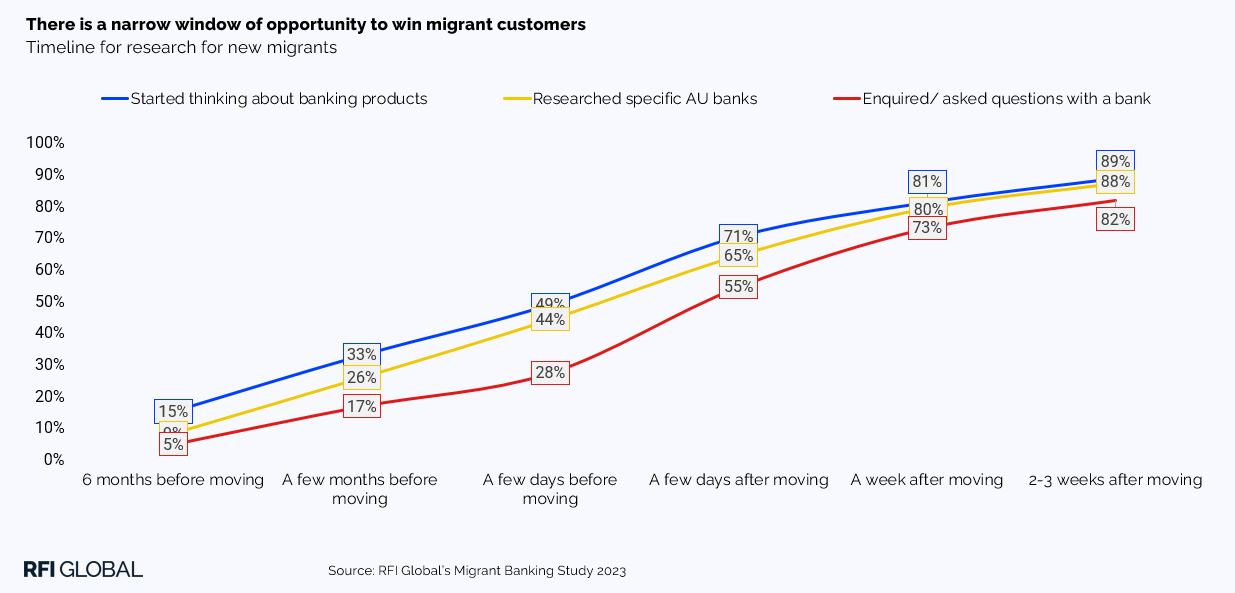

Also, of note, 31% of prospective migrants say they aren’t familiar with any banking brands. I’m a great believer in there being two sides to every statistic, and so, to me, this shows that 69% are aware of Australia’s banks and the study shows that this is because one in two (49%) has already started thinking about banking products and 44% have researched banking products before they even set foot in the country.

You could argue that waiting for migrants to arrive before engaging with them is already too late.

In fact, a whopping 76% of recent arrivals said that they would like to receive information on Australian banking before moving.

Leveraging advocacy and easing transitions

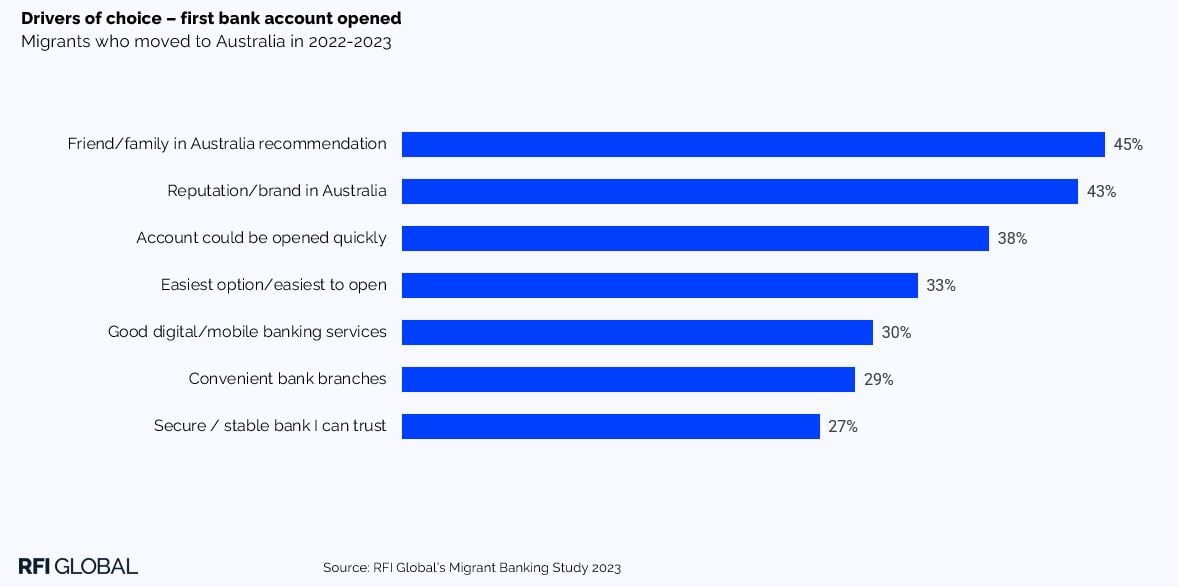

So, how can you best expand that reach beyond the borders? Analysing the drivers behind the choice of first bank account is revealing. Nearly half (45%) of all migrants that arrived in the 2022-23 period, stated that they chose an account because it had been recommended by friends or family in Australia.

Beyond these recommendations, reputation, ease, speed, convenience, innovation and stability all play a role in the end decision and should be factors to emphasise for any bank wanting to service the arrivals.

This is reinforced by the study’s question of where recent arrivals found their information when it came to researching banking. Speaking to friends and family, migration agents and using social media all fell into the top five sources of information, alongside contacting banks directly and general internet searches.

The implications

There are clear actions that banks and financial institutions can take at every stage of the migrant journey. If we focus on the fact that being the first bank leads to ongoing patronage (90% of migrants are still banking with the same bank after five years), then engaging with prospective migrants is a key component of success.

And the conclusion? One in two migrants has done their banking research by the time they set foot in Australia, and their existing support networks are easing their entrance into the country and steering them in the direction of the right service providers.

The opportunity for banks is to leverage word of mouth by:

- Engaging with community groups and migration agents who are easing the transition to living in Australia

- Implementing customer-get-customer strategies when it comes to referrals to encourage customer advocacy

- Engaging with prospective migrants through social media channels

Of course, you could wait until they arrive, but that seems like a miss.

Subscribe to get the latest RFI data and insights.

Data-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.