Jackie Greig, VP Marketing, Global

As many households worldwide grapple with rising costs and economic uncertainty, others are building wealth. Affluent consumers are increasingly influential in shaping the global financial services landscape.

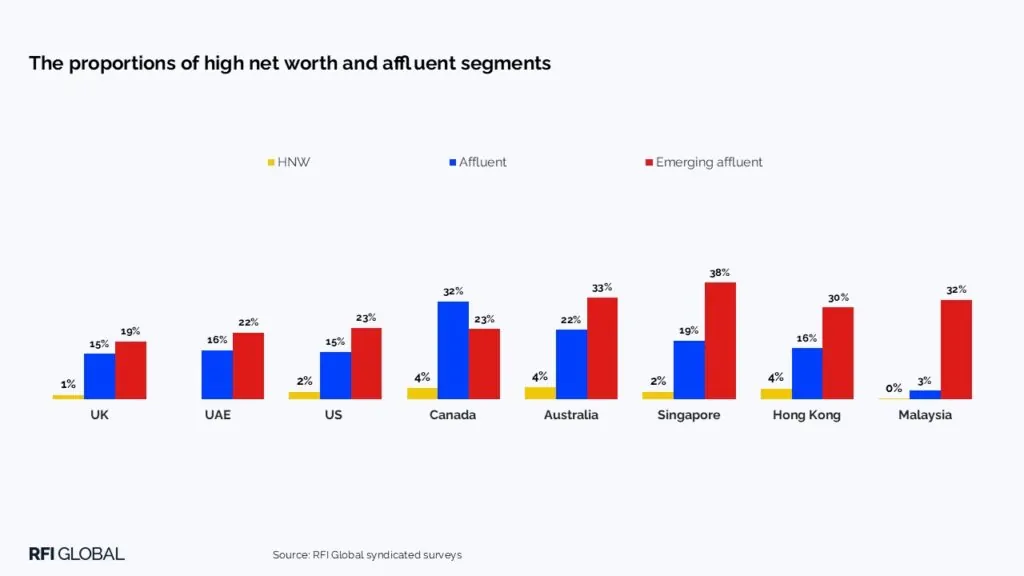

While definitions of affluence vary by market (see RFI Global definitions below), our data show that high-net-worth (HNW) individuals represent a small elite segment of around 2-4% of country populations. In contrast, the broader affluent segment is significantly larger, representing between 15% and 32% of the population in most markets. Canada stands out with nearly a third (32%) of its population qualifying as affluent, while Malaysia is an outlier at just 3%.

The next wave of affluence

Alongside established affluents, the emerging affluent segment represents a distinct and influential group. Typically comprising younger professionals, entrepreneurs, or digitally native consumers, these individuals are on an upward financial trajectory, with growing incomes, investments and purchasing power. The emerging affluent segment makes up between 19% and 38% of country populations, with Asian markets and Australia standing out with high proportions of emerging affluent customers, representing the next wave of affluents customers.

Over the past two years, these proportions have remained largely stable. Notable shifts include a 3% rise in affluents in the US, accompanied by a 9% decline in emerging affluents. In the UK, we’ve seen a modest increase of 2% in both segments.

The value of affluent consumers

The financial impact of these groups becomes even clearer when examining their share of investable assets. Affluents and high-net-worth individuals together control up to 89% of investible wealth. In Canada, the US and the UK, the figures are highest at 89%, 88% and 86%, respectively. The UAE (58%) and Malaysia (29%) have a lower overall concentration, but with the highest value amongst emerging affluents at 24% and 52% respectively.

To put this into perspective: in the US, just 18% of households hold 88% of investable assets. That’s an enormous concentration of financial power in a relatively small segment of the population.

What does the future hold?

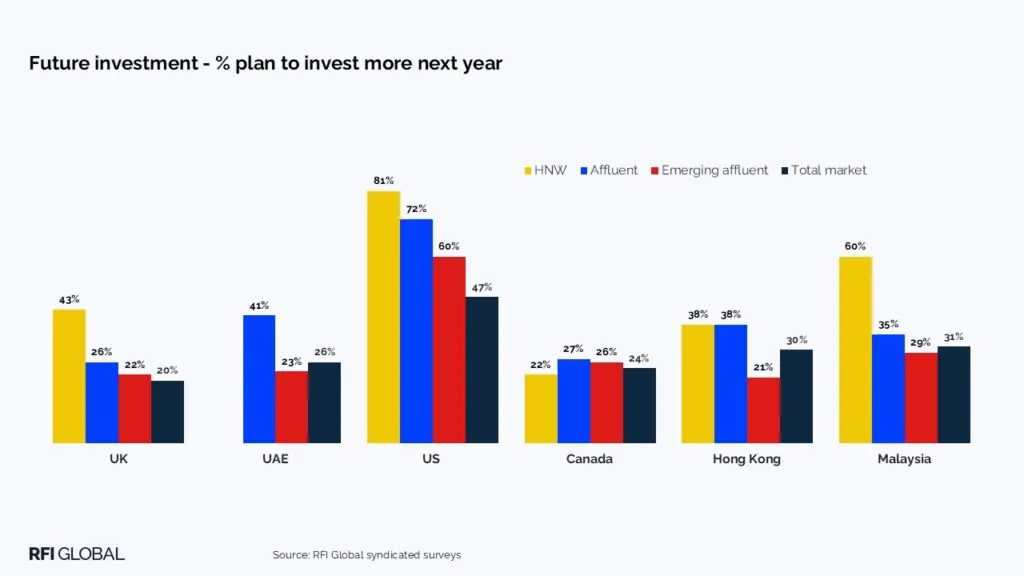

Affluent consumers are not just wealthy; they are forward-thinking and actively shaping their future. Many plan to increase their investments over the next 12 months. In the US, 81% of high-net-worth individuals and 72% of affluents say they intend to invest more next year. Canada shows a more conservative outlook, with a lower intent to grow investments, with just 22% of HNWs and 27% of affluents planning to invest more next year.

Affluent consumers also typically hold more financial products, on average, two more per person, and they are much more likely to own investment products. The difference is marked in the US and UK, where 86% and 68% of affluents, respectively, hold investments, compared to just 48% and 39% of the general population.

The challenge for financial service providers

Affluent consumers are financially savvy and more likely to shop around for products and consider alternatives. In most markets, we’ve seen an increase in switching intentions in the past few years. Affluent customers in the UAE show the strongest loyalty to existing providers, with the lowest switching propensity, whereas affluent and HNW customers in the US are the least loyal, with the highest propensity to switch.

So, how can you capture a bigger share of affluent segments?

With numerous product holdings and high switching intentions, affluent consumers are not always loyal to their providers – they tend to spread their assets. In the UK, for example, affluent consumers keep less than 50% of their savings with their bank. HSBC leads the pack, capturing 60% of their customers’ wallets, ahead of Barclays at 55%, the only two banks to capture more than half of their customers’ affluent savings wallet.

Affluent consumers provide opportunities both to deepen existing relationships and to win new ones. But what sets this segment apart from the mainstream? And how can providers position themselves to win?

Five ways to attract and retain affluent consumers

Affluent consumers are shaping the future of financial services. Their behaviours, expectations and goals demand tailored strategies. Whether your focus is loyalty, growth or innovation, understanding this segment is critical. Here are five ways to engage and retain affluent customers:

1. Tailor by market maturity

In established markets like Canada, where affluent penetration is high, the focus should be on deepening relationships through wealth advisory services, premium offerings and personalisation. In growth markets like Singapore and Malaysia where emerging affluents represent strong future potential, education, access and aspirational branding are key to nurturing the next wave of affluent consumers.

2. Invest in digital, but don’t neglect human touch

Affluent consumers are digitally savvy, often favouring online channels and digital-only banks, but they also value expert advice and personalisation. A hybrid model that blends seamless digital experiences with access to knowledgeable advisors is likely to resonate most.

3. Differentiate through product breadth and innovation

In markets like Singapore and Hong Kong, product engagement is high. Providers that offer a diverse range of options, from international equities and ETFs to structured products, can grow wallet share. Smart, personalised recommendations based on data add further value.

4. Build trust through purpose, values and transparency

Values matter. Transparency is key to savvy investors who are more likely to be shopping around. ESG considerations are increasingly important in some markets, especially among emerging affluents in the US. Understanding how this segment thinks about sustainability and social impact can help brands tailor both messaging and product development.

5. Switching is an opportunity and a risk

High switching intent means there’s a constant risk of losing customers, but also an opportunity to win new ones. Financial institutions must focus on delivering long-term value, strong service and standout propositions to attract affluent switchers and retain loyal customers.

Reaching affluent consumers takes more than simply recognising their wealth, it requires a nuanced understanding of their behaviours, motivations and expectations, and how these vary across markets.

RFI Global’s syndicated research solutions offer in-depth insights into how affluent individuals manage their financial lives: what they value, how they invest, and what influences their loyalty. Get in touch for more insights from our research to discover how to better attract and engage affluent segments in your markets.

Jackie Greig

VP Marketing, Global

Jackie Greig is the Global VP of Marketing at RFI Global. She is a senior marketing and market research leader with extensive experience building global marketing strategies for financial services brands.

View full profileData-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.