Digital players are becoming increasingly sophisticated, and consumer uptake is increasing around the world. In the UK, the proportion of people using digital-only providers has increased since 2018 from 16% to over 50%. An interesting trend is that as well as the anticipated take-up by Gen Z, there has been a significant uptake by Mass Affluent consumers with 28% in the UK now holding liquid assets with neo banks.

So, what’s behind this trend?

As digital wealth providers continue to improve their offerings, the simplicity and speed of the UX have increased in appeal to this segment.

To better understand how wealth is distributed and assess the impact RFI Global launched Wealth Trax in Singapore, Hong Kong and the UK. Wealth Trax collects and analyses data on all the savings, investments and wealth of consumers by product type, provider, volume and value. This enables us to track how wealth and share of wallet are distributed by institution and to understand the value of wealth providers are losing to other players.

Singaporean share of wealth

The average Singaporean wallet holds $218,261 SGD of which 39% is with local banks, 27% with foreign banks and 7% with digital-only players. DBS has the largest share of the local banks while Citi holds the greatest share of the foreign banks.

Wealth also increases significantly between the Emerging Affluent segment and the Mass Affluent segment, increasing from $99k to over $810k SGD.

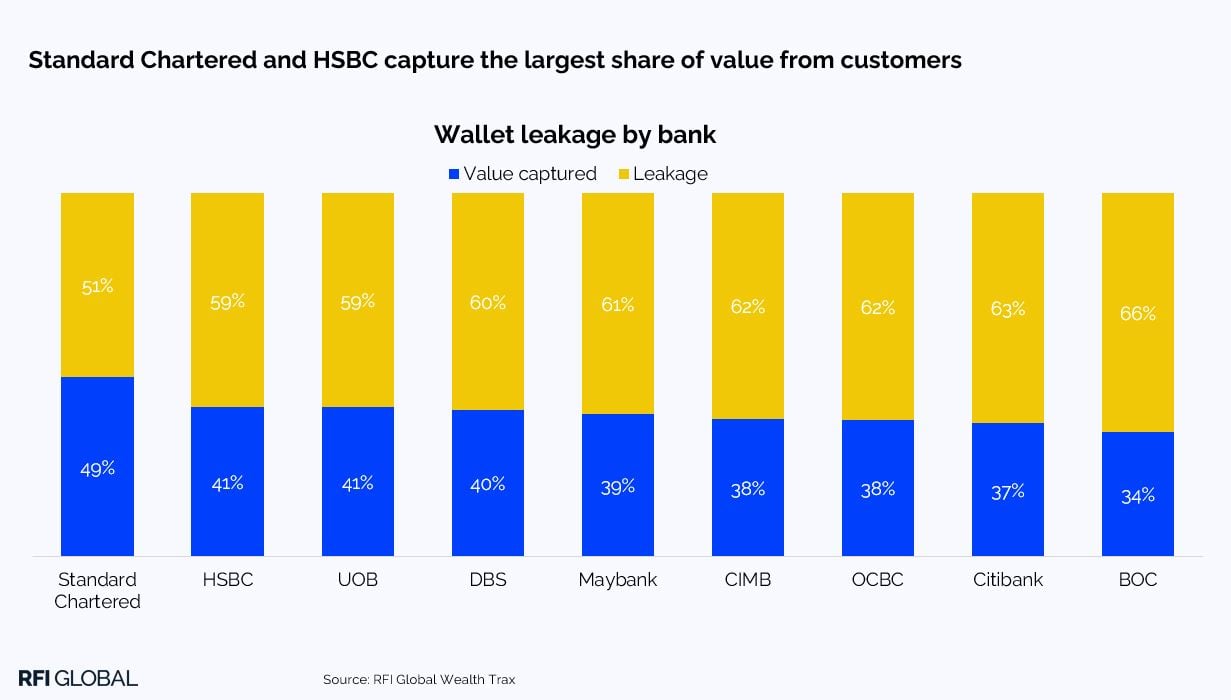

When we look at the Mass Affluent wallet, we see that as well as the average wallet increasing to $810,500, the foreign banks’ share of wallet increases to 34%, and the local banks drop to 32%. The digital-only players also increase to 10% of the share of wallet. While HSBC leads the foreign banks capturing $89k of the total $810k, followed by Citi at $72k and Standard Chartered at $71K they are still pipped by DBS who capture the most share of the Mass Affluent wallet with $116k.

While DBS leads the pack by total value, they are only third when it comes to the stickiness and loyalty of their Mass Affluent customers. DBS capture 40% of their customers’ wallets but HSBC capture 41% and Standard Chartered leads on loyalty with a massive 49% of all their Mass Affluent consumers’ wealth captured.

With the exception of DBS, each of the foreign banks competes with its foreign-based peers for the share of the Mass Affluent wallet each losing approximately 18-20% to their foreign peers. The 10% of the wallet that is captured by digital providers is mainly won by Trust, GXS and Maribank.

How do UK banks compare?

The average wallet size in the UK is just over £26k with Nationwide leading the pack at 13% just ahead of Barclays and HSBC at 11% and 8%. The digital players have made strides with almost 13% of the total wallet with Shawbrook leading Chase and Marcus all of whom are ahead of Monzo.

When we look at the UK Mass Affluent wallet which averages just over £121k, Nationwide again lead the pack with 13% ahead of Barclays at 12% and HSBC at 10%. Lloyds are at the back of the high Street banks both with the average consumer wallet and the Mass Affluent wallet.

When we look at the loyalty of the UK Mass Affluent consumers, HSBC is far ahead of the pack capturing 60% of their customers’ wallets, ahead of Barclays at 55%, the only two banks to capture more than half of their customers Mass Affluent wallet in either market.

Lloyds again lag the High Street pack with only 28%, attracting less than a third of their customers’ wallets. When we look at the average consumer wallet HSBC again leads on loyalty followed by Barclays with both again attaining over 50% of their customers’ wallets.

While the digital players in the UK are still only just over 10%, we can see from the above chart that Marcus is starting to gain real traction with the top end with over a quarter of their Mass Affluent customers’ wealth. It will be fascinating to revisit this data next quarter to see the progress of the digital banks.

What next?

Get in touch for exclusive insights from our wealth analysis.

Data-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.