Luke Allchin, Director, North America

Canada’s financial services sector is navigating a complex mix of digital maturity, consumer caution and intensifying competitive pressure. While many of the forces reshaping banking are global, Canadian consumers exhibit distinctive behaviours, particularly around trust, technology adoption and expectations of service quality.

Drawing on insights from RFI Global’s Financial Services Trends and Predictions 2026 report, alongside data from our Consumer Banking, Payments and Innovation survey (CBPI) and iSky digital benchmarking platform, this article explores the five key trends set to shape the year ahead for financial institutions in Canada and what they mean for growth, loyalty and competitive advantage.

Trend #1. From curiosity to confidence: Building trust in AI-powered finance

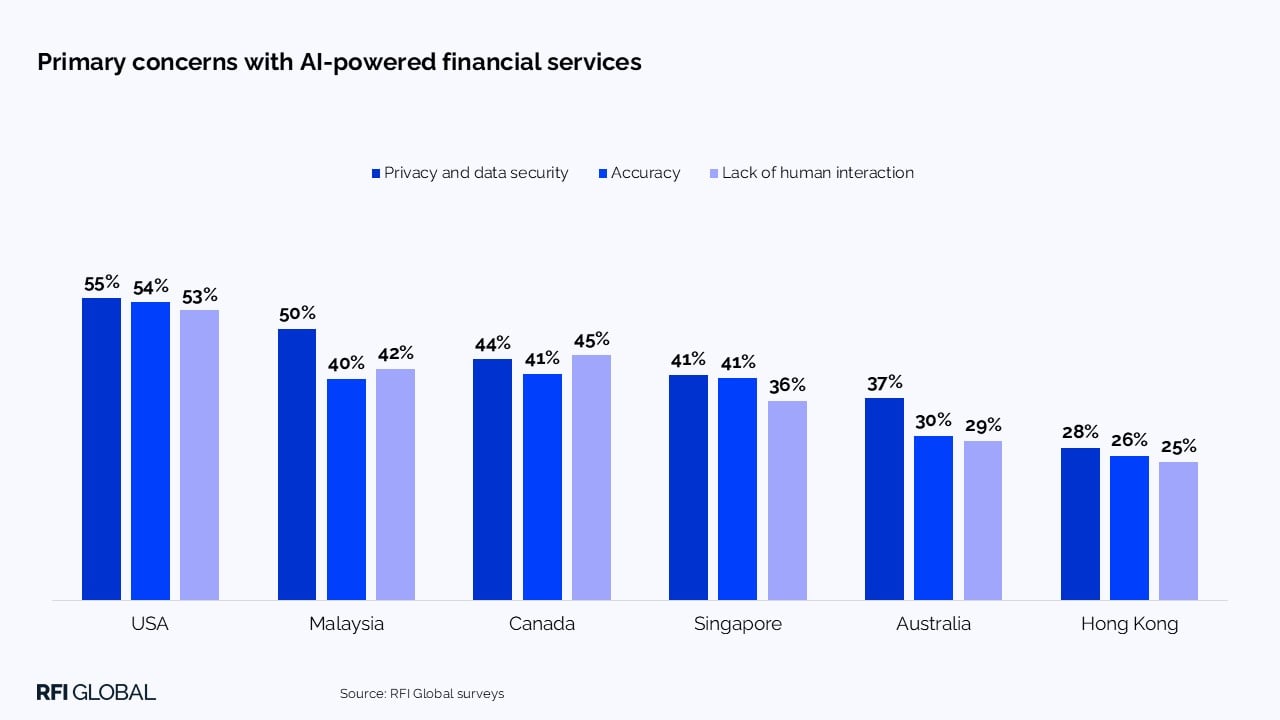

AI is firmly on the agenda for Canadian banks, but trust remains the biggest barrier to widespread adoption. CBPI data shows that 94% of Canadian consumers have concerns about using AI with their bank, with privacy and data security the dominant fears. This places Canada alongside Singapore and Australia among the most cautious markets globally when it comes to AI in the financial services sector.

Consumer interest in AI-powered banking tools also varies greatly by use case. While markets such as Hong Kong, Malaysia and Singapore see around three-quarters of consumers open to AI-based virtual assistants, predictive insights and behavioural analysis, Canadians are far more hesitant. Outside of fraud detection, enthusiasm for AI in everyday banking remains limited, highlighting the need for education and reassurance.

Concerns about human connection are particularly pronounced. Nearly half of Canadians (45%) are worried about losing the personal touch when financial services are delivered through AI, and comfort levels are lowest for automated advice: just 36% say they are comfortable with robo-advisors. For Canada, the message is clear. A blended model that combines AI efficiency with human support is essential.

CBPI data also indicates a market split down the middle. Half of Canadian consumers are ready to embrace AI in financial services, while the other half remains cautious, creating a meaningful window of opportunity. Banks that prioritise explainability, strong governance and clear guardrails around data use will be best placed to convert hesitation into confidence.

Trend #2. Digital user experience: The key battleground for customer loyalty

Mobile and digital banking are now central to how Canadians manage their finances, but the pace and focus of innovation change across areas. Insights from RFI Global’s iSky Radar platform reveal that cards have become a priority area of catch-up for Canadian providers. Over the past two years, around 35% of institutions introduced in app card locking for the first time, reflecting a concerted effort to close the gap with global peers in this critical UX and security feature.

That improvement is material, but it also underscores where Canada has historically lagged. Card controls and self service tools have been slower to arrive than in other markets, even as consumer expectations around security and control continue to rise.

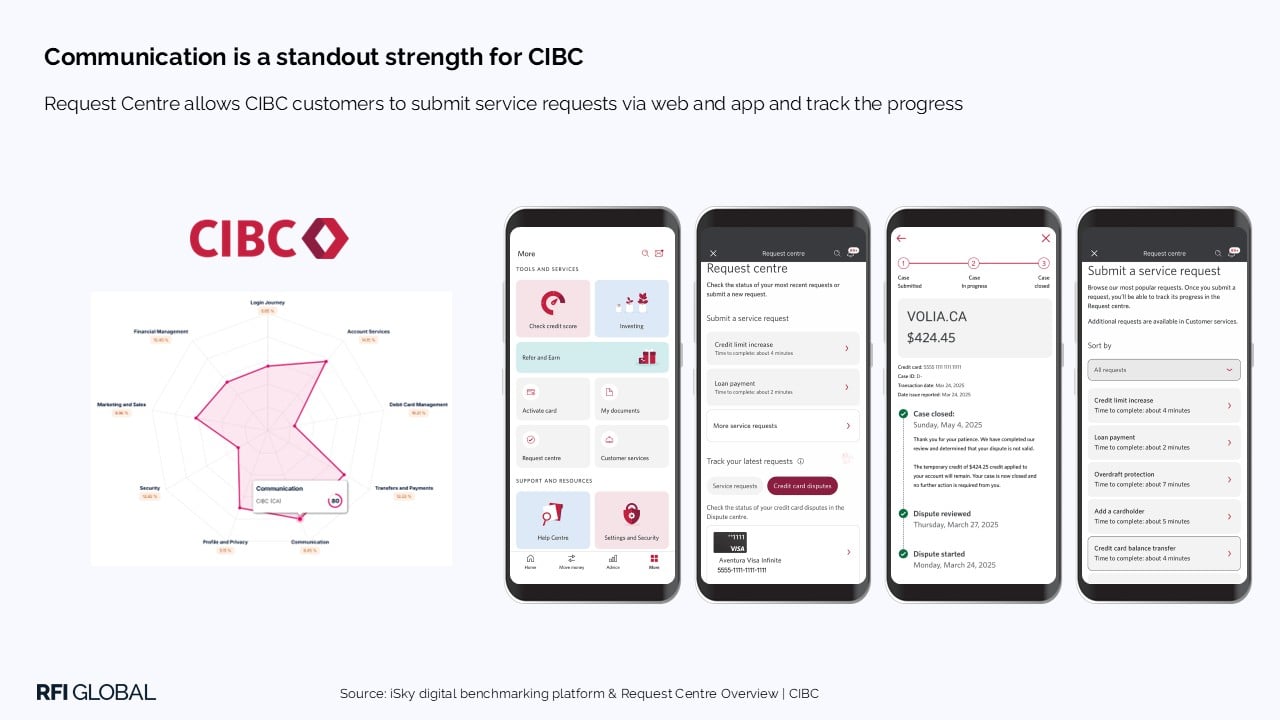

At the same time, Canada shows clear areas of strength. Communications and transparency are a standout, with solutions such as CIBC’s Request Centre providing customers with visibility on non straight through processing requests. These kinds of tools improve customer understanding, reduce operational costs and strengthen perceptions of responsiveness and trust.

Beyond core functionality, banks are also investing in value adding features. Rewards and benefits offerings have increased by 29% over the past two years, often delivered without incremental fees, while accessibility tools and information services are up 22%. Together, these enhancements signal a growing emphasis on inclusion, transparency and perceived value.

As digital experiences become a core expectation, Canadian institutions that continue to improve control, clarity and usefulness, rather than simply adding features, will be best positioned to protect loyalty in a mature, highly competitive market.

Trend #3. The next chapter for neobanks: From growth to value

Neobanks in Canada occupy a very different position compared with markets like the UK or the US. CBPI data shows that around 20% of Canadian consumers now have an active relationship with a digital only bank compared to 26% in the UK and 29% in the US, representing a slight decline since the end of 2022, suggesting that momentum has stalled rather than accelerated.

Importantly, the market structure matters. The two largest digital-only players, Tangerine and Simplii, are both owned by incumbent banks. As a result, disruption in Canada has been more evolutionary than revolutionary, with challengers reinforcing consumer expectations around pricing and usability rather than fundamentally reshaping banking models.

Lower fees remain the primary reason Canadians choose digital-only banks, and the leading driver for making them a primary banking provider. Product breadth, advisory capabilities and ecosystem expansion are still limited compared with more mature neobank markets.

For incumbents, this creates both comfort and risk. While competitive pressure from pure challengers is more muted, customer expectations around value, simplicity and digital ease have been permanently reset. The lesson from Canada’s neobank story is not about scale, but about standards. And those standards are now firmly embedded in the Canadian market.

Trend #4. Cybersecurity: Fraud has evolved, but have banks?

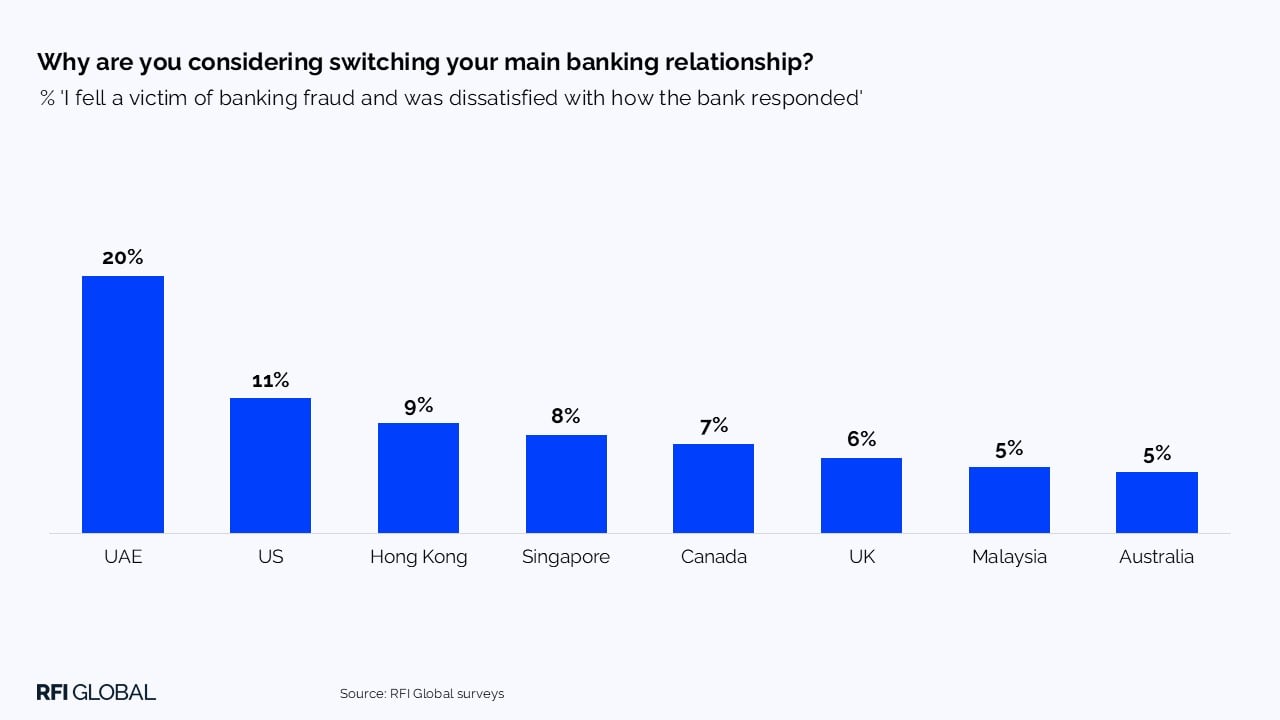

Fraud continues to weigh heavily on consumer confidence in Canada, particularly when banks fail to meet expectations at moments that matter most. CBPI data shows that 7% of Canadians considering switching providers cite being a victim of fraud and dissatisfaction with how their bank responded as the trigger behind their intention to leave.

This signals an important shift: prevention remains critical, but response is just as influential in shaping trust and loyalty. Faster detection, clearer communication and visible support during fraud incidents have become key differentiators.

AI has a role to play here, but comfort is cautious. Half of Canadians say they are somewhat comfortable with AI-powered fraud detection and prevention, reinforcing that this is currently the strongest and most accepted AI use case in financial services. Getting it right can improve protection without undermining trust. Getting it wrong risks accelerating distrust of AI more broadly.

As fraud tactics become more sophisticated, banks will need to combine advanced analytics with customer education and reassurance. Those who can strengthen security while maintaining transparency and empathy will be better placed to defend relationships in an increasingly high risk environment.

Trend #5. Wealth in 2026: Unlocking fee-based growth as affluent investments rise

While Canada’s wealth opportunity is substantial, unlocking it will depend less on technology alone and more on confidence and engagement. Widespread caution around automated advice suggests that fully digital wealth propositions may struggle without clear human support and guidance.

The reluctance toward robo-advisors, combined with strong concerns about AI accuracy and personal relevance, points to a market where hybrid advice models are likely to resonate most. Helping consumers move from deposits to investments will require more than access; it will require reassurance that advice is aligned, transparent and accountable.

For Canadian banks and wealth providers, the opportunity in 2026 lies in combining digital convenience with visible expertise. Clear explanations, tailored recommendations and optional human support will be essential to converting intent into fee based growth.

What’s next for financial institutions in Canada?

Canada enters Q2 2026 as a market defined more by caution than pace. Consumers are digitally engaged but highly discerning, particularly when it comes to AI, security and trust. 2026 will be pivotal for banks seeking to move customers from cautious acceptance to confident use of new tools.

Institutions that invest in transparent AI governance, close remaining UX gaps, respond decisively to fraud and blend digital efficiency with human reassurance will be best positioned for sustainable growth. In a market where trust is hard won and easily lost, execution will be the defining advantage.

Get in touch to explore the data behind these trends and what they mean for your strategy in Canada.

Luke Allchin

Director, North America

Luke Allchin is a Director, North America at RFI Global, leading financial services research and advisory across the North American market.

View full profileFrequently Asked Questions

Q: What are the key trends defining Canadian financial services in 2026?

The Canadian financial services market in 2026 is shaped by five key trends: growing but cautious adoption of AI, digital user experience becoming the primary battleground for customer loyalty, a shift in neobanks from growth to value, the increasing importance of fraud response in building trust, and a renewed focus on hybrid wealth models to drive fee-based growth.

Q: What are the barriers to AI adoption in Canadian banking?

Trust remains the primary barrier to AI adoption in Canadian banking, with 94% of consumers expressing concerns, particularly around privacy and data security. Many customers are also worried about losing human interaction, and comfort with AI-driven advice remains low. As a result, banks must prioritise explainability, strong governance and human support to increase confidence and adoption.

Q: How important is digital user experience for customer loyalty in Canada?

Digital user experience is a critical driver of customer loyalty in Canada, with mobile banking now central to how consumers interact with their financial institutions. While banks are improving features such as card controls, rewards and accessibility, gaps remain compared to global peers. Institutions that focus on usability, transparency and meaningful functionality, rather than simply adding features, are best positioned to retain customers.

Q: What is driving switching behaviour among Canadian banking customers?

Fraud-related switching is increasingly driven not just by the incident itself, but by how banks respond. Around 7% of Canadian consumers considering switching cite dissatisfaction with their bank’s handling of fraud. Faster response times, clear communication and visible customer support are now essential to maintaining trust and reducing churn.

Q: What is the opportunity for wealth growth in Canada’s financial services market?

The wealth opportunity in Canada lies in helping consumers move from deposits to investments through hybrid advice models. Low trust in fully automated advice and concerns about AI accuracy mean that combining digital tools with human guidance is critical. Providers that deliver transparent, tailored and accountable advice will be better positioned to drive fee-based growth.

Data-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.