The pace of change across global financial services continues to accelerate. In 2025, AI and digital innovation reshaped how consumers and businesses manage money, while fintech expansion and economic uncertainty changed expectations of value, loyalty and service. Customer behaviour evolved in markedly different ways across markets, from near-universal mobile wallet adoption in APAC to the UK’s continued reliance on cash.

AI is at the centre of these changes, presenting both significant opportunities and new risks for institutions navigating heightened expectations around trust, security and transparency.

Drawing on insights from over 200,000 consumers, 60,000 businesses and thousands of real banking app interactions worldwide, our Financial Services Trends & Predictions 2026 report outlines the five trends we believe will define the year ahead. This article is a snapshot – download the full report for deeper analysis and market-by-market comparisons.

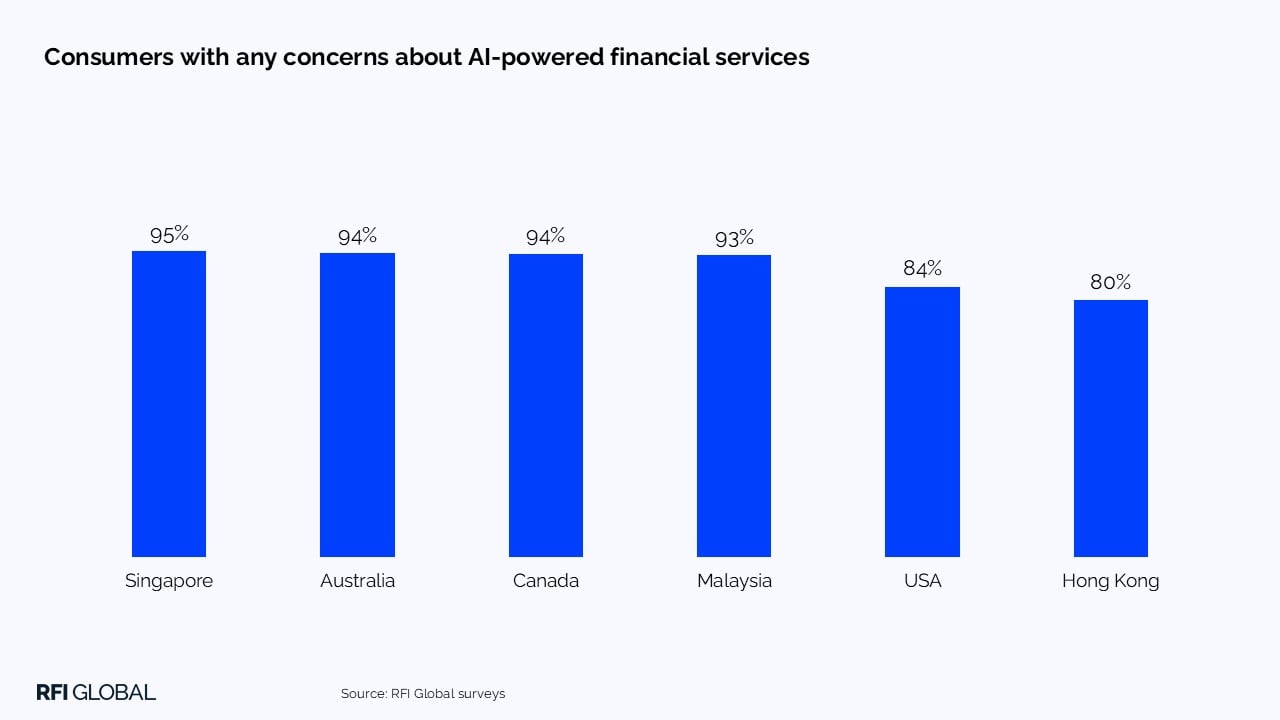

1. From curiosity to confidence: Building trust in AI-powered finance

AI is rapidly moving from novelty to necessity in financial services, but widespread adoption still hinges on trust. Most consumers globally report at least one concern about using AI in banking. Even in the most confident markets, the US and Hong Kong, around four in five consumers express reservations.

The strongest barriers to AI relate to trust, accuracy and the perceived loss of human interaction. People want to understand how AI makes decisions, how their data is stored and used, and when they can still rely on human support.

For financial institutions, progress relies on transparency, reassurance and responsible design. Providers that clearly articulate safeguards and offer hybrid human-AI experiences will be better placed to build confidence and engagement.

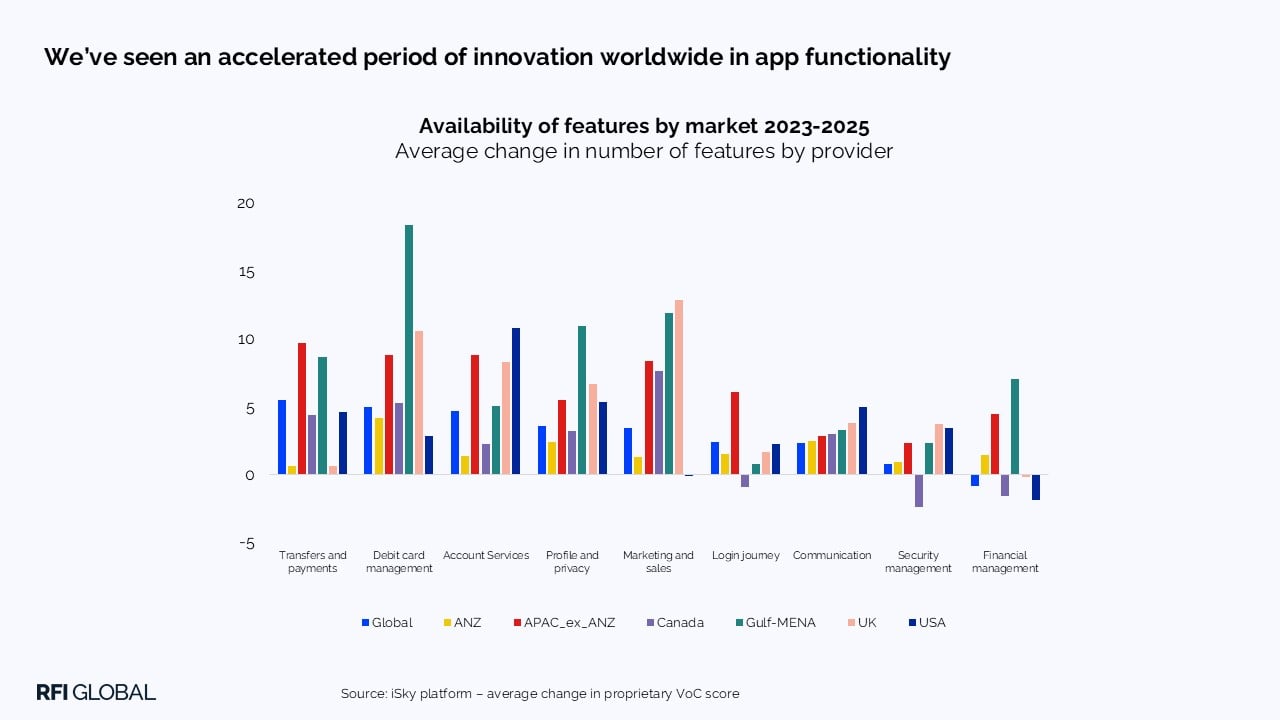

2. Digital user experience (UX): The key battleground for customer loyalty

Digital experience has become a key differentiator in financial services. As mobile overtakes online as the primary banking channel, customers expect journeys that are intuitive, secure and consistent – and are increasingly prepared to switch when these expectations are not met.

Our iSky platform, which analyses thousands of real interactions across more than 200 banking apps worldwide, shows growth in features that enhance transparency and control:

- The ability to lock or disable a card has increased 13.8% over the past two years.

- In the same period, 16% of banks globally added profile or account closing functionality.

- And over 10% added the ability for customers to view card details in-app.

Across markets, the direction is clear: digital access is no longer enough. Institutions are investing in experiences that provide customers with more visibility, greater security, and increased autonomy in their day-to-day banking.

3. The next chapter for neobanks: from growth to value

Neobanks are entering a new phase, one defined not by rapid customer acquisition, but by deeper engagement, stronger trust and sustainable profitability. After years of scaling fast with narrow propositions, they are now evolving into full-service providers through broader product suites, embedded technology and strategic partnerships.

Our data shows this evolution is gaining momentum.

- In the US, neobanks’ share of primary banking relationships has almost doubled – from 4.6% in 2022 to 8.7% in 2024.

- In the UK, the share of primary banking relationships rose from 3.5% in 2022 to 5.9% by mid-2025.

Customers are increasingly choosing neobanks as their main financial provider, not just a secondary or niche option. As consumers seek better value, personalisation and frictionless digital experiences, neobanks are well-positioned to expand wallet share and redefine what customers expect from their primary bank.

In 2026, we expect this shift in strategy to accelerate and reshape the competitive landscape, driven by consumer demand for value, innovation and integrated financial experiences, as well as growing trust in these providers.

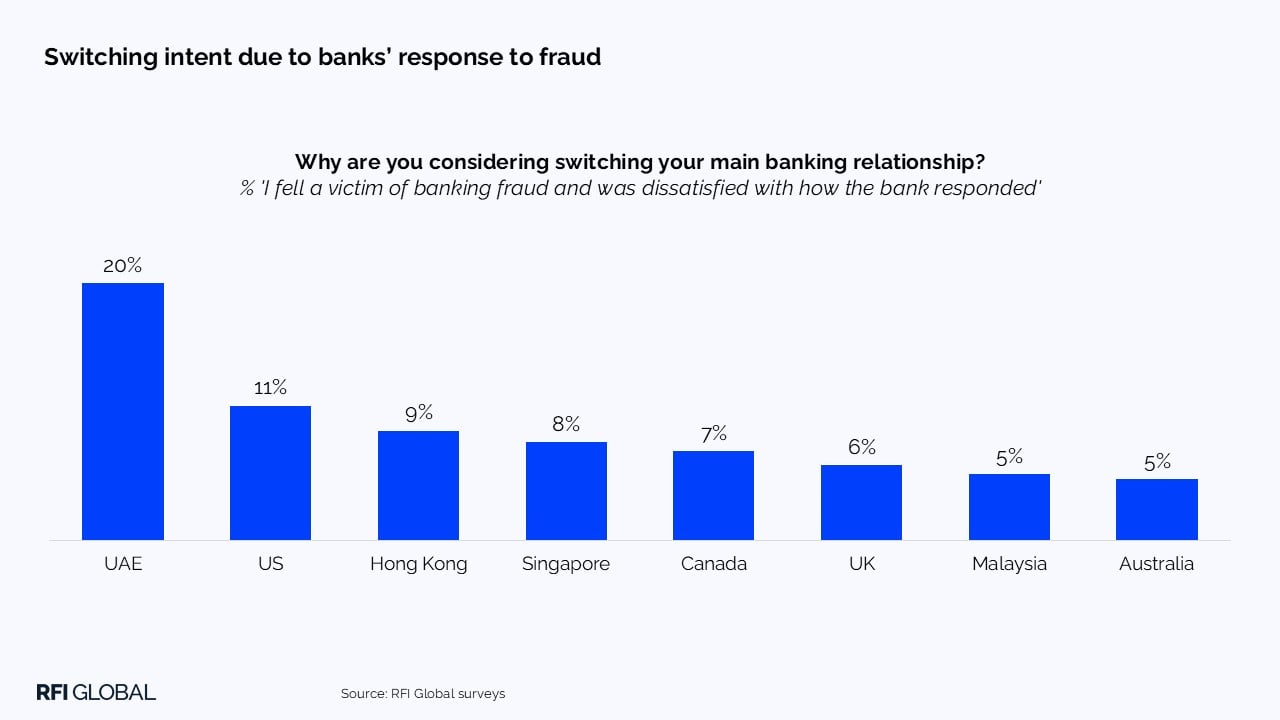

4. Cybersecurity: Fraud has evolved, but have banks?

Fraud is evolving at unprecedented speed, fuelled by AI, digital tools and increasingly sophisticated scams. As threats intensify, financial institutions face growing pressure to strengthen detection, secure digital interactions and protect customers without adding friction. At the same time, expectations are rising sharply: consumers want stronger protection that feels seamless, intuitive and trustworthy.

Confidence in security now shapes a wide range of behaviours – from preferred payment methods to customers’ willingness to trust digital channels. It also plays a growing role in retention. Across markets, 5–20% of customers say their bank’s response to fraud is a key reason they are considering switching.

In 2026, cybersecurity will remain a core differentiator. The institutions that lead will be those that make protection visible, proactive and reassuring, without disrupting everyday banking.

5. Wealth in 2026: Unlocking fee-based growth as affluent investments rise

As interest rates fall, affluent consumers are moving funds from savings into higher-return investments, signalling a renewed surge in global wealth activity.

Our data reveals a global resurgence in investment intent:

- Singapore: 41% of affluent consumers are open to reallocating funds from savings to portfolios.

- United States: Investments account for 31% of household financial assets.

- UK: 31% of affluent consumers plan to chase higher returns.

- UAE: 24% of affluent consumers are exploring new wealth offerings.

As consumers rebalance from deposits to diversified portfolios, fee-based growth is becoming the new benchmark for success for banks. However, capturing this opportunity depends on addressing behavioural inertia, improving visibility across cross-border wealth flows and strengthening digital advisory services. Customers are ready to invest, but they want clear guidance, transparent propositions and seamless digital experiences.

Implications for financial institutions in 2026

Together, these trends point to a year where competitive advantage will come from clarity, digital capability and customer confidence. Institutions will need to build trust in AI-powered services, deliver intuitive and effortless digital experiences and respond to rising expectations around value and personalisation. Neobanks will continue to influence what customers consider ‘best practice’, while wealth providers must be ready to support growing investment appetite with advice that is accessible, transparent and relevant.

Download the full report for detailed trend analysis, global and local insights and a deeper view of the consumer and business behaviours shaping financial services in the year ahead.

Interested in how these trends are shaping the US? Read this article.

Interested in how these trends are shaping the UK? Read this article.

What you need to know about financial services in 2026

Q: What are the biggest trends shaping financial services in 2026?

A: RFI Global’s latest analysis highlights five major trends: rising consumer expectations for trustworthy AI in banking, rapid innovation in digital user experience, the shift of neobanks from growth to profitability, escalating cybersecurity challenges and renewed investment appetite among affluent consumers. Together, these trends are redefining how people and businesses choose and interact with financial providers.

Q: How will AI change financial services in 2026?

A: AI will become more deeply embedded in everyday banking, supporting tasks from financial management to customer service. However, trust and transparency remain essential. Institutions that clearly communicate how AI is used, ensure accuracy and provide accessible human support will be best positioned to drive adoption and confidence.

Q: Why is digital experience (UX) so critical for banks now?

A: Mobile has overtaken online as the primary channel for banking and customers expect seamless, secure and intuitive digital journeys. Our data from more than 200 banking apps shows significant growth in features that enhance security, transparency and control. Providers that deliver strong digital experiences are more likely to retain customers and attract new ones.

Q: What does the rise in investment activity mean for financial institutions?

A: Falling interest rates are prompting affluent consumers to move money from low-yield deposits into higher-return investments. This creates opportunities for fee-based growth, but only for institutions that address behavioural inertia, improve cross-border visibility and deliver more personalised, digitally enabled advisory services.

Data-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.