Kakoli Banik, Senior Data Visualisation and Automation Executive, EMEA

UK borrowers are feeling the squeeze. New mortgage rates may have dipped to 4.26% from their 2023 peak, yet sustained high mortgage costs and persistent inflation are undermining consumer sentiment. RFI Global’s UK consumer banking survey, Orion, reveals that borrower confidence in meeting repayments has deteriorated, particularly for younger Gen Z and Millennial borrowers.

Borrowers are more motivated than ever to secure the best deal. However, the anxiety isn’t just about affordability; it’s also about access to help. With the Bank of England forecasting 3.6 million mortgage accounts set to refinance onto higher rates over the next three years, how can lenders support borrowers and earn their loyalty for renewal?

The market is active and mobile

Borrower activity is accelerating

Despite household pressures, the value of new mortgage commitments reached £78.2bn in Q2 2025 – the highest since 2022 – signalling renewed housing confidence and a replenished pipeline of lending.

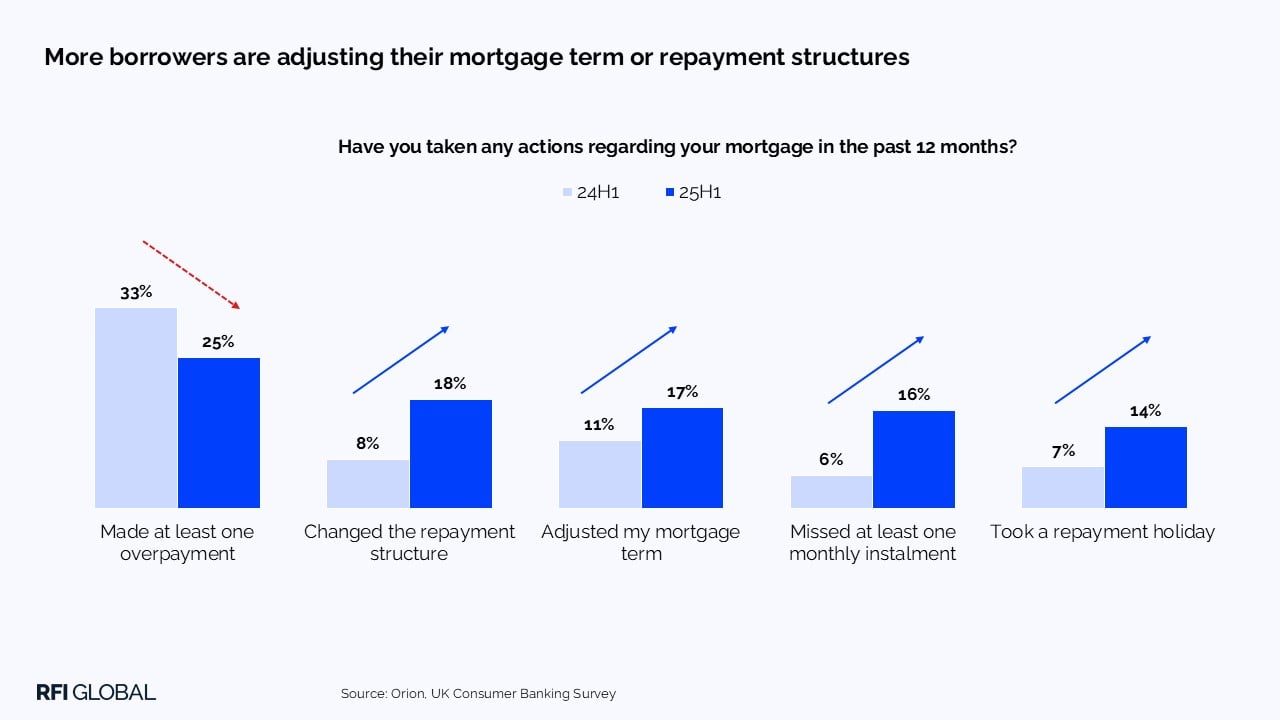

However, our data shows that overpayments are on the decline and missed payments are on the rise. Even a modest £100 increase in monthly payments will cause financial strain for a quarter of borrowers who are feeling the pinch, highlighting high levels of vulnerability in the market. Borrowers are increasingly exploring ways to adjust their mortgage terms or repayment structures. Repayments are hitting Gen Z the hardest, making them the most inclined to adjust their mortgage repayment structure. Millennials concerned about their finances are more likely to extend their mortgage term or take repayment holidays.

Switching intent is at a peak

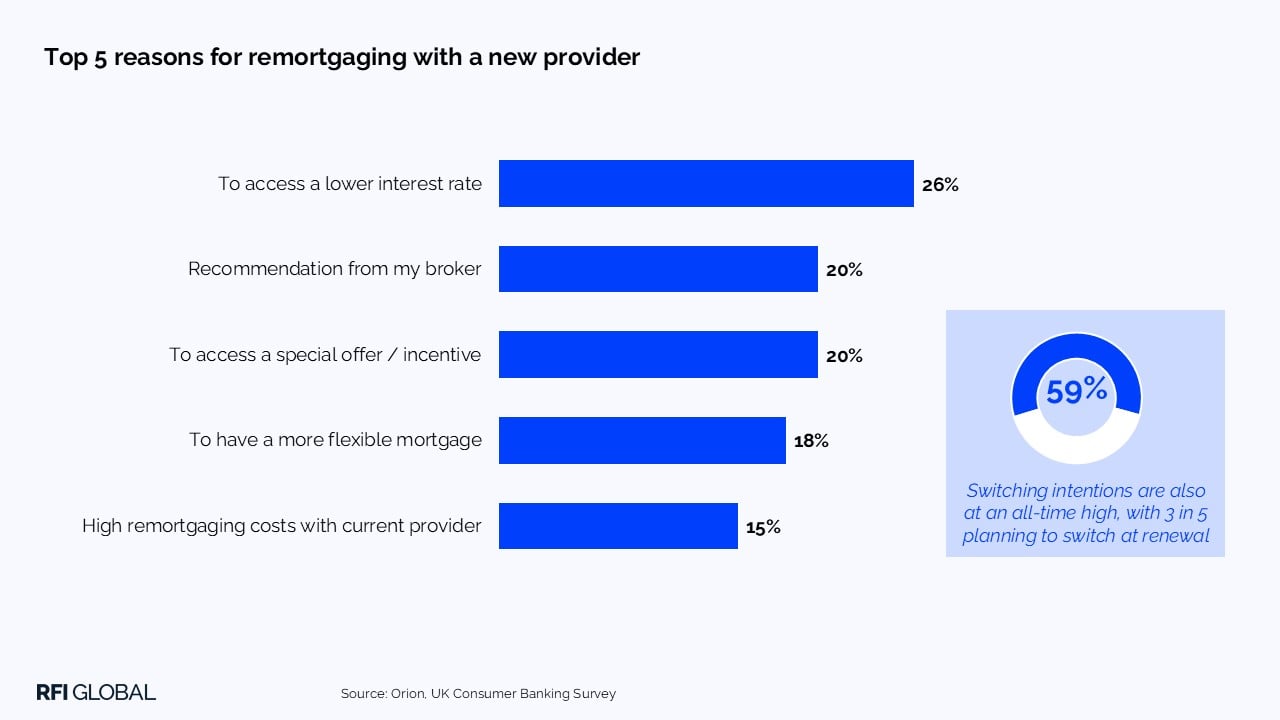

This activity coupled with a slight dip in mortgage rates has fuelled a surge in switching intent. Our data shows 3 in 5 borrowers plan to switch lenders at their next renewal, a 1.5x increase compared to six months ago. While rate competitiveness remains the primary driver, flexibility is also emerging as a critical differentiator. Switching intent rises further among consumers who have sought out support; these borrowers want access to options like term extensions, repayment holidays, and interest-only periods to help them manage uncertainty.

Ultimately, borrowers are seeking a deal that reduces their overall mortgage costs. Application incentives are increasingly shaping that perception of value, especially among those recently active like first-time buyers and people remortgaging. For lenders, this isn’t just a challenge, it’s a prime opportunity to acquire new customers by combining competitive pricing with smart incentives and frictionless remortgaging.

Policy tailwinds and early engagement

Regulation could further influence borrower expectations. The 2023 Mortgage Charter has made early engagement the norm: nearly half a million borrowers have locked in new deals up to six months early. This gives lenders a prime chance to re-engage customers before term-end to strengthen loyalty, and prevent churn. At the same time, borrowers need proactive, ongoing engagement, with lenders ready to step in when additional support is required. Recent reforms have expanded access to flexible repayment options, helping thousands of borrowers ease short-term financial pressure and maintain stability through challenging conditions.

Looking ahead, the FCA’s Mortgage Rule Review aims to further enable flexible affordability, later-life lending and balanced risk rules – creating room for innovation. We’ve already seen Skipton’s 100% LTV mortgage, which uses rental history to help first-time buyers – it shows how lenders can combine affordability innovation with incentives to win new customers.

How to win the active borrower market

With borrower demand and regulatory support aligned, now is the moment for lenders to act. Here are some guidelines based on what our data says about consumer needs.

1. Engagement borrowers early:

Treat maturity as a months‑long journey i.e., start outreach months before term-end. Use proactive nudges, pre‑approved personalised offers, in‑app comparisons and allow rate re‑pricing to keep customers loyal. Early engagement also gives lenders more direct control over renewals, reducing reliance on brokers and creating opportunities to strengthen relationships with customers before competitors step in. Pair this with application incentives like cashback or fee waivers to attract potential borrowers and convert intent into action.

2. Offer flexible-support:

Lenders should publish clear guidance on flexible options such as interest-only periods, term extensions and repayment pauses. Support must be easy to access across digital, phone and branch channels, with simple navigation and clear instructions. Making borrowers aware they can seek help without consequence is key to building trust and establishing lenders as genuine, customer-focused partners.

3. Make brokers your allies:

With 89% of new business expected via intermediaries, double‑down on broker experience: speed up decisions, clarify policies and provide real-time updates to make brokers your strongest acquisition channel.

4. Streamline the digital remortgage journey:

Fix operational ‘speed bumps’; identity repeats, document loops, manual affordability checks and opaque status updates.

5. Innovate for inclusion:

Product features matter as much as rates. Our data shows that borrowers weigh up term-length, mortgage type and application experience alongside price. Launch products for first-time buyers and later-life borrowers with features like delayed start mortgages and part-and-part structures.

Why act now: momentum and responsibility

The market is evolving. New mortgage commitments are rising, but affordability remains constrained and inflation sticky. Lenders that combine fair pricing with smart flexibility will gain trust and convert switching intent into durable relationships.

Understanding borrower behaviour has never been more important. Up-to-date insights into customer sentiment and engagement are essential for lenders to respond to financial pressures with tailored solutions that retain customers on track and foster loyalty.

Find out more about Orion here.

Kakoli Banik

Senior Data Visualisation and Automation Executive, EMEA

Kakoli Banik is a Senior Data Visualisation and Automation Executive at RFI Global, turning research data into clear insight across EMEA.

View full profileFrequently Asked Questions

Q: Why are UK borrowers under pressure in 2025?

A: Inflation remains elevated, and mortgage rates are well above pre-2022 levels. RFI Global data shows many borrowers, especially younger generations, are financially vulnerable, with even modest repayment increases causing strain.

Q: How can lenders support financially stressed borrowers?

A: Lenders can proactively help by providing clear, accessible options before arrears happen. Flexible solutions like repayment holidays, extending terms, or interest-only periods assist borrowers in managing short-term difficulties. Proactive engagement, budgeting tools, and early-warning signals from open banking data also enable lenders to identify and support vulnerable customers early, preventing issues from escalating.

Q: How many UK borrowers plan to switch lenders?

A: Almost two-thirds (59%) of borrowers intend to switch their mortgage at their next renewal, a 1.5x increase compared to six months earlier. Switching is being driven by competitive rates and demand for flexible mortgage features.

Q. What role do brokers play in mortgage switching?

A: Brokers are the main channel for new mortgage business: 89% borrowers apply through them. This is expected to rise to 91% by 2026. They increasingly guide customers toward lenders that offer both competitive rates and adaptable features.

Q: How can lenders build mortgage loyalty in a high-rate market?

A: Lenders can engage borrowers early, provide clear flexible options, streamline digital remortgaging, partner effectively with brokers, and innovate with inclusive products to meet evolving needs.

Data-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.