The changing face of consumer credit – competition and the mismatch of intention and reality

I’ve spoken a lot in my recent articles about the impact of a sustained period of high inflation and its knock on effects on household budgets. However, one aspect that I haven’t dealt with is the changing attitudes and behaviours of consumers when it comes to credit and debt.

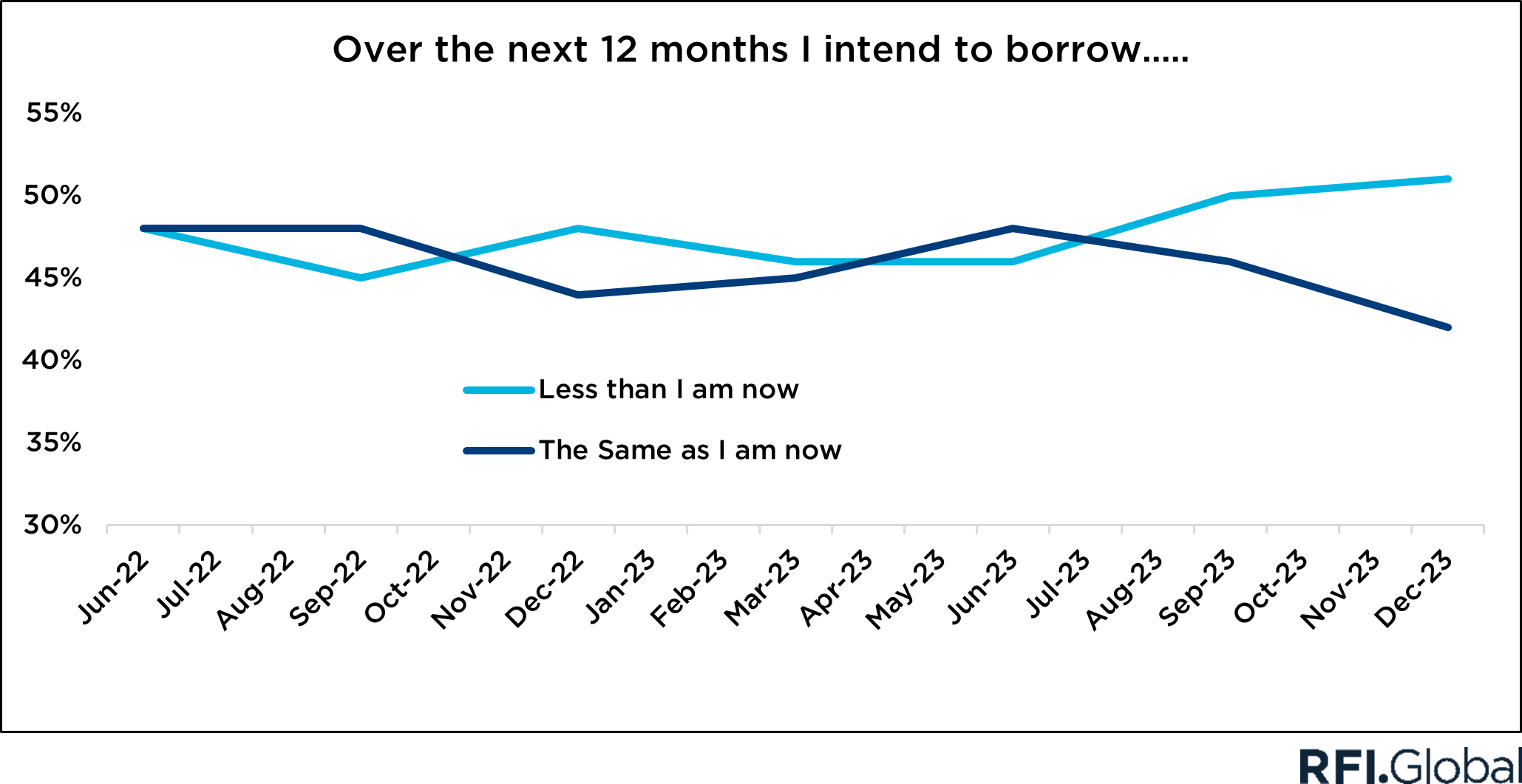

I was looking through some of RFI’s data this week in preparation for a presentation and saw that in the December quarter of last year, the proportion of Australians that said they were looking to borrow less in the next 12 months had hit 51%, the first time we’ve seen that figure go above 50% since we’ve been tracking it.

At the same time as we’ve seen the rise in intent to borrow less, we’re seeing an increase in the proportion of consumers wishing to pay down debt at an increased rate – 29% in December 2023 vs 23% in June 2023).

How does this play out in demand?

The question that this raises, is whether we should expect to see a real decrease in demand for credit. To answer this, I thought I’d look at personal loans (PL’s) as they are less impacted by interest rate levels and property market cycles than mortgages and less impacted by access to alternative payment mechanisms than credit cards.

Focusing on PL’s then, over much of 2023, acquisition velocity [1] – a measure of growth in personal lending – hovered around the high 4%’s compared to a long term average of closer to 3%, so the indications are that the market is running quite hot.

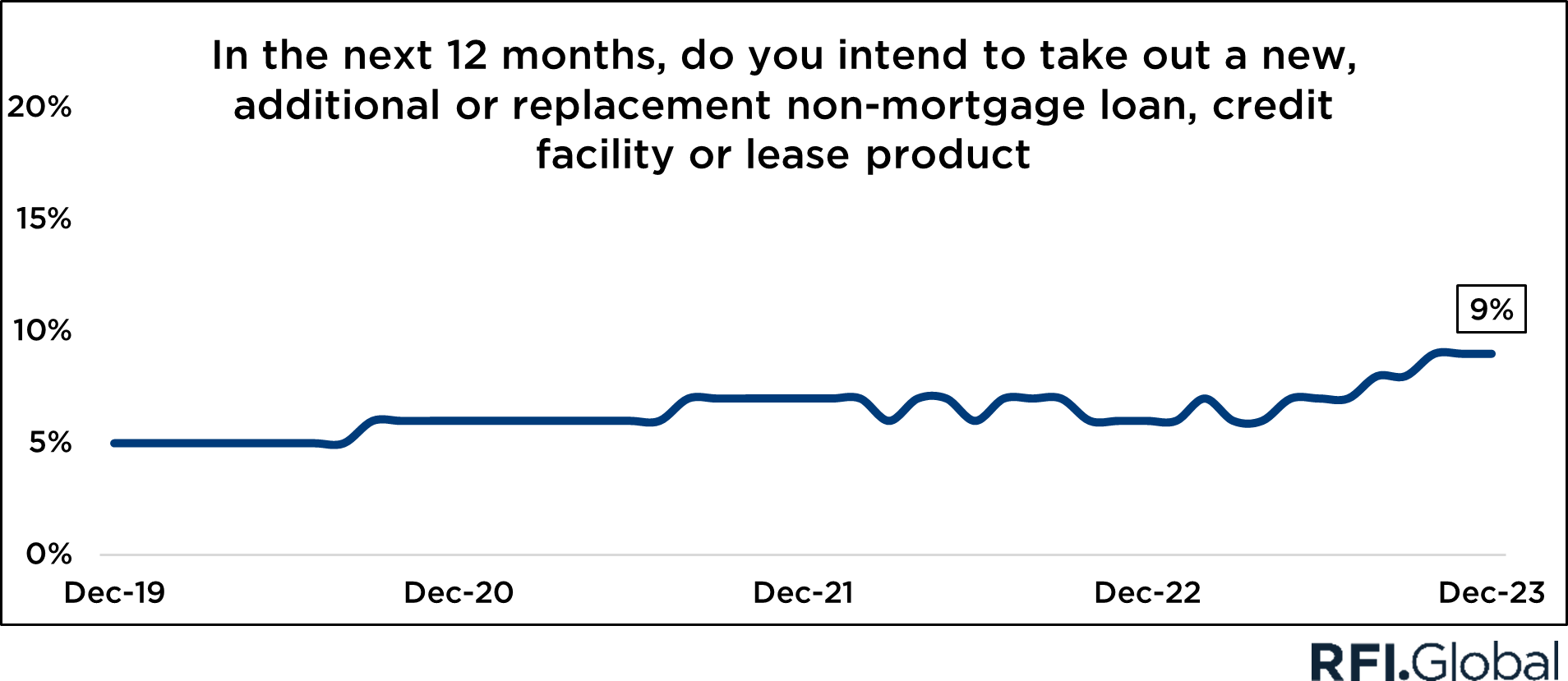

The interesting thing is that RFI’s Atlas data shows no signs of abatement. In fact, when we examine the proportion of adults that are looking to take out a personal loan we see that it has risen markedly from an average of 5% in 2019, to 6-7% between 2020 and 2022, to current highs of 9% at the end of 2023, almost double the demand of just a few years ago.

This data essentially highlights the mismatch between intention and reality on the part of consumers. On the one hand, they want to minimize their borrowing to a greater extent than we’ve seen historically, but on the other hand, there are more people than ever looking to take out personal lending products.

Regardless of intention, sometimes life just gets in the way. You need to consolidate or refinance existing debt, or you need to replace your car of make a large purchase that isn’t covered by your savings and there is no alternative.

Personal lending up against unprecedented competition

With almost one in ten adults looking to take out a personal lending product in the next 12 months, it’s also worth looking at the options available to consumers.

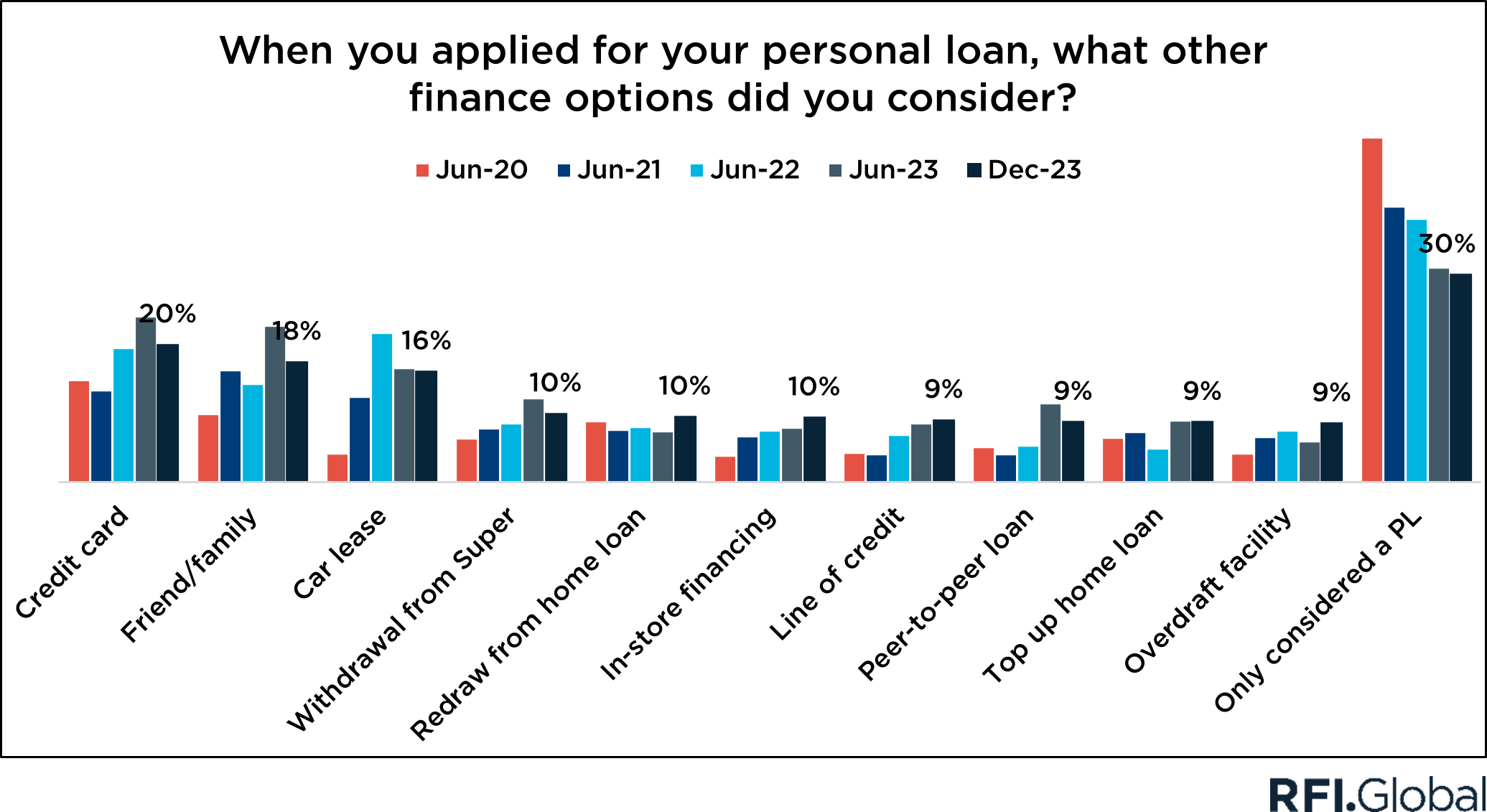

The data shows that in December 2023, just 30% of recent borrowers only considered a PL when they applied for their most recent loan. This compares to 51% in June 2020 – a figure that has reduced rapidly ever since.

The implication is of course that the competition for every new personal loan customer is higher than it’s been for years. And this is borne out by the number of alternatives considered by these borrowers. In June 2020 the average borrower considered 2.0 possible means of raising the funds they require and by the middle of 2023, this had risen to 2.7.

With new alternative lending options becoming available all the time, this view is particularly pertinent. This fact, coupled with consumer demand for PLs and the current inflationary environment putting pressure on household budgets mean that it’s unlikely in the medium term that we will see a reduction in the consideration of multiple credit mechanisms.

So does this mean that we will start to see consumers turn their backs on traditional PLs as a means of funding purchases? I don’t believe so.

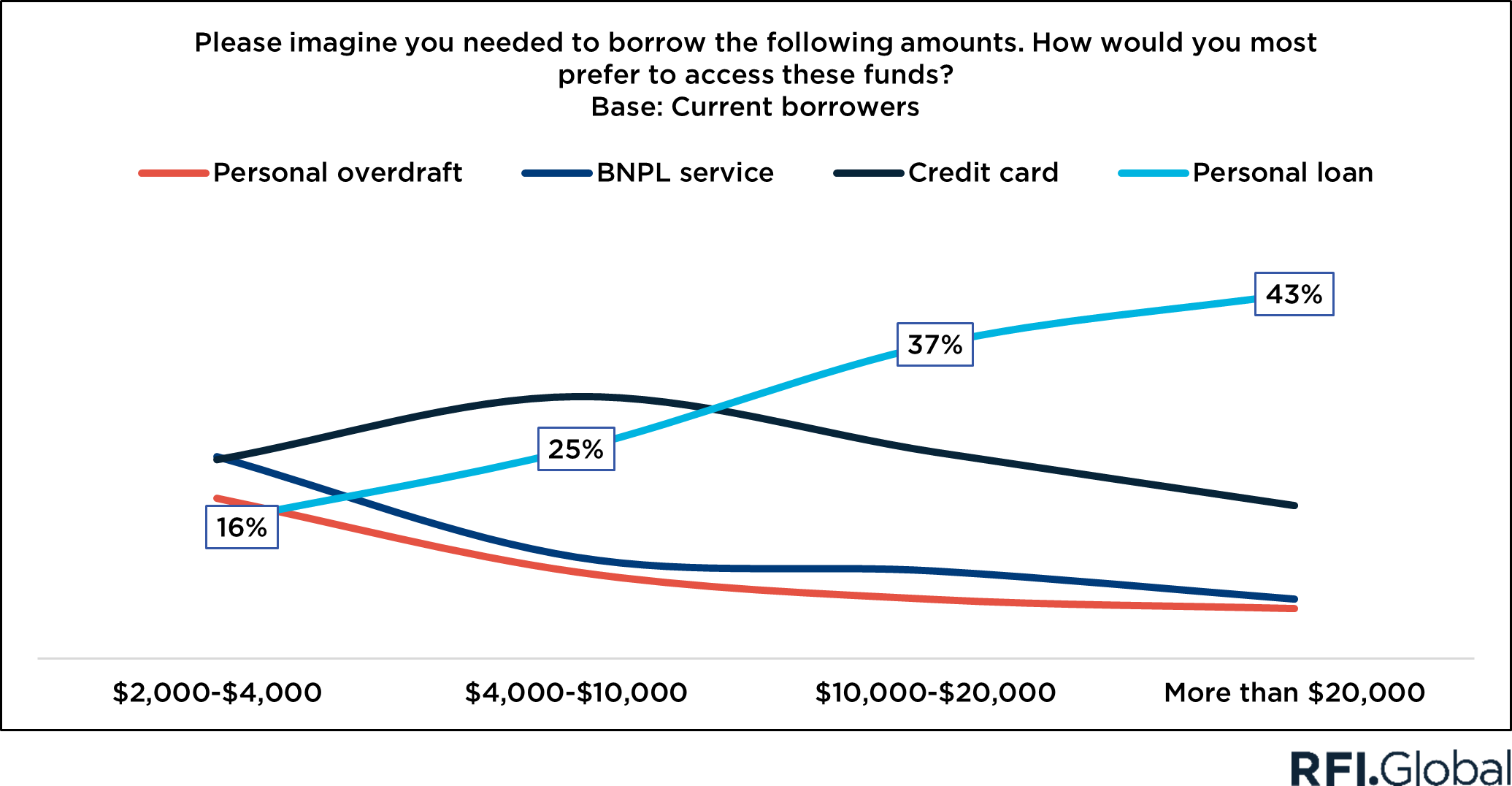

One reason is that consumer choice and preference is highly tied to the amount of money required. When RFI asked borrowers how they would prefer to borrow varying amounts of money, there is a clear point at which the personal loan comes into its own.

Below $4,000, credit cards and BNPL options win, with 24% of borrowers saying that each of these mechanisms are their preferred and PLs get just 16% of preference behind overdrafts on 19%. As we move into the $4k-$10k bracket, BNPL drops away and PL’s (25%) start to rival credit cards (31%) , and beyond $10k PLs have an almost unassailable lead in preference against other credit mechanisms.

The second reason is that consumers like the discipline of the personal loan. The very act of making repayments and seeing a balance reduce over time, without the temptation to redraw or add other purchases that other borrowing mechanisms offer, brings a comfort to consumers.

These feelings (discipline and comfort) are exactly what resonate with consumers in an environment like we see in 2024, where more than half of us want to borrow less and almost one in three want to pay down our debt at a faster rate than we are.

So, while competition for credit products will mean that alternative borrowing mechanisms increasingly snatch a share of loans at the smaller end of the dollar spectrum, in the traditional PLs space, we will continue to see a need for credit among consumers and a demand for loans above $10,000.

[1] Acquisition velocity is taken from RFI’s Personal Loan Business Tracker (PLBT) and is calculated by dividing new sales in a month by total book value

Subscribe to get the latest RFI data and insights.

Data-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.