When I started my first business, I asked my dad what the most important thing was. He answered ‘Cash’ and told me that first thing, every morning I should always open the books and check my cash position. In fairness, he started his business in the 1970s when ledgers were de rigueur, but the point remains. After successfully exiting that business and when I was launching RFI in 2006 I asked my boss, a self-made billionaire, the same question – he also answered, ‘Cash is king.’

The implications for SME owners

Understanding that cash is king and access to capital is all-consuming is crucial to understanding the pain points of SME owners. I’ve talked a lot about the differing needs between SME owners and consumers over the last few blogs. What is often ‘nice to have’ for consumers is a ‘must have’ for SME owners.

When we look at open banking, embedded finance and partnerships between banks and fintechs, understanding these differences becomes increasingly important. Open banking and embedded finance met the same initial reluctance among consumers as many other new technologies such as contactless, digital wallets, etc. The issue is always a concern around security. As the proof of the value proposition increases, the concerns around security diminish, to the point we reach a tipping point and the majority of the market takes up the new product/ technology.

What do consumers think about open banking?

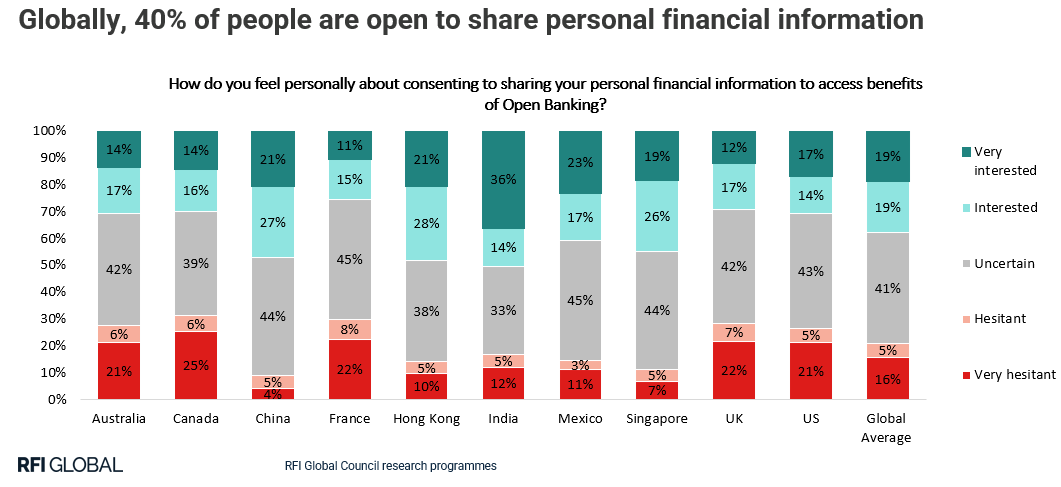

Launched in various markets between 2016 and 2018, open banking is a case in point. Led by regulators and politicians to drive greater choice for consumers ( i.e. voters) and open up bank switching – traditionally a static market with less than 3% switching accounts annually despite over 15% always looking to switch.

There has been an openness and willingness to share data for open banking benefits among Asian consumers, with an average of 50% in each market, with Western markets following somewhat reluctantly behind. While globally 40% of consumers are keen to explore open banking opportunities in the UK, this is less than a third even in 2024.

To date, the successful value positions around open banking for consumers remain few and far between.

SME’s perspective on open banking

However, among SMEs, where it is a pain point to be solved, there is significantly more appetite and take up.

Although there is still an initial reluctance, as Jane Prokop, EVP and Global Head of SMEs at Mastercard, says in our Banking Uncovered podcast, once an SME has been turned down for credit by a traditional bank and is then able to get approval instantly from a fintech via an open banking solution, “these proof points are extremely powerful.”

Again, the use case is one of necessity as opposed to choice. Jane points out “Open banking is used for a variety of tasks including KYB. Open banking is incredibly useful for credit decisioning.” “While this is great news for the SME owners it requires a new way of thinking for the traditional bank. If it attempts to own the customer experience and customer interaction it is unlikely to succeed. If however, it is open to partnering and working with fintechs who have built open banking into their decision making, where the relationship is initiated and owned by the fintech partner, then the potential opportunities for the traditional bank increase.”

Be where your customers are

When I spoke to Mohammed Keraine, in an earlier podcast, he talked about the need to be a chat-first institution and about how important it was to be where the customer is, as opposed to trying to bring the customer to you. We can see this starting to play out in the rise of super apps. While RFI Global’s data shows that 60% of consumers globally are interested in super apps where they can do everything in one place, this is heavily skewed towards Asia, with Western markets much less enthusiastic. In the UK only 3% of consumers want to see their banking apps combined with their non-banking apps.

Again security is a key issue and again it is a question of choice for consumers and a question of need for SME owners. While there remains reluctance among consumers as Jane says, “SME owners are looking for simplicity, for a one-stop shop experience. It is all about going to where they are doing their daily business. If they are using a vertical specific software, then it needs to have the payment functionality baked in.”

This is similar to Mohammed’s comment on consumers and shows that effectively they are looking to the SME equivalent of a super app. This is where embedded finance can come in to play. RFI Global data shows that the number of SME owners who are interested in embedded finance has grown in just a few years from 1 in 5 to 1 in 2. More and more use cases for SMEs are being developed and launched continuously.

Partnering with fintechs

The key to this is partnership. As with open banking, institutions that are willing to partner with fintechs who provide embedded finance solutions and, in doing so lose the primary access to the relationship, will be the eventual winners.

Jane says that there are some key global trends or universal truths about SME owners; the need for cash or access to capital and the need for operational efficiency. There is a global annual $6 trillion gap between the capital SMEs require and what they can access. SME owners that are put in the centre of the eco-system by an institution and have payment and finance solutions brought to them , in the place where they are doing business, will gain greater operational efficiency and reduce their need for cash. Cash is still king. Banks, payments providers and fintechs looking to succeed in this space need to:

- Understand that access to capital is key either via credit or integrated payments that create operational efficiencies and provide a value proposition that delivers on this where the SME owner wants it.

- Embrace partnerships, where in doing so, they acknowledge that they will lose the primacy of the customer relationship to their partners(s).

Subscribe to get the latest RFI data and insights.

Data-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.