Luke Allchin, Director, North America

Retirement planning has always been a crucial aspect of financial health, but the approach to it has evolved significantly over the years. The generational divide in the US presents a fascinating landscape where Baby Boomers, Gen X, Millennials, and Gen Z each exhibit distinct attitudes and strategies toward retirement. Understanding these shifts is essential for financial institutions aiming to support clients in achieving their retirement goals.

The evolution of retirement products

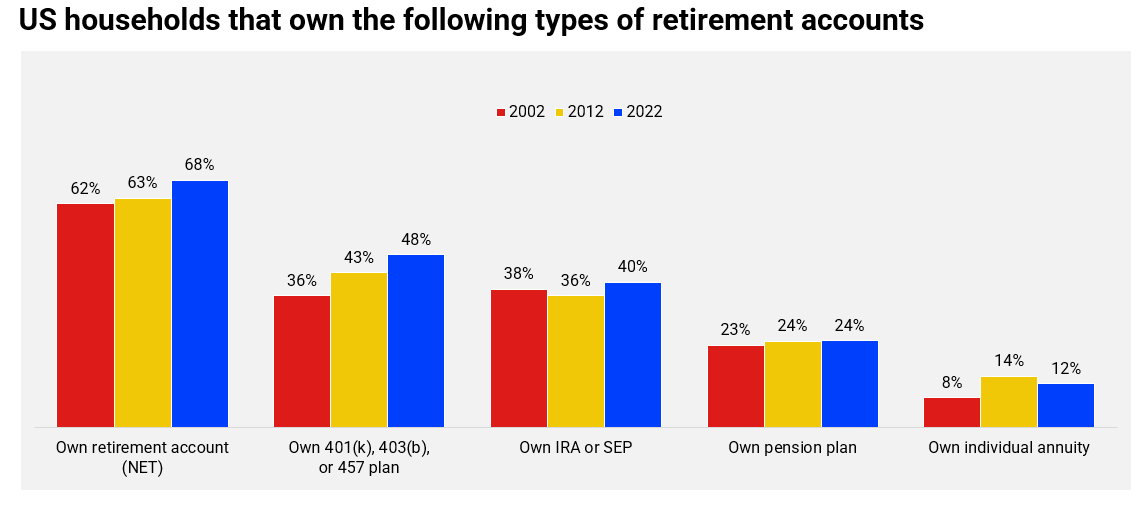

According to RFI Global’s MacroMonitor study, since 2002, there has been a consistent rise in the ownership of retirement accounts, primarily driven by the uptake of 401(k) plans and Roth IRAs. While ownership of traditional IRAs has remained mostly consistent, ownership of Roth IRAs has almost doubled since 2002. This trend underscores a growing awareness and proactive approach to retirement savings among US households. The variety of available retirement products has expanded, catering to diverse needs and preferences across the generations.

The 2008 global financial crisis had a significant impact on investment behaviors, with many consumers shifting their holdings in publicly traded stocks, mutual funds, and employer savings plans. While these have partially recovered, packaged and custodial accounts have seen a continued decline. In contrast, ownership of ETFs and 529 plans is rising, reflecting a preference for diversified and education-focused investments.

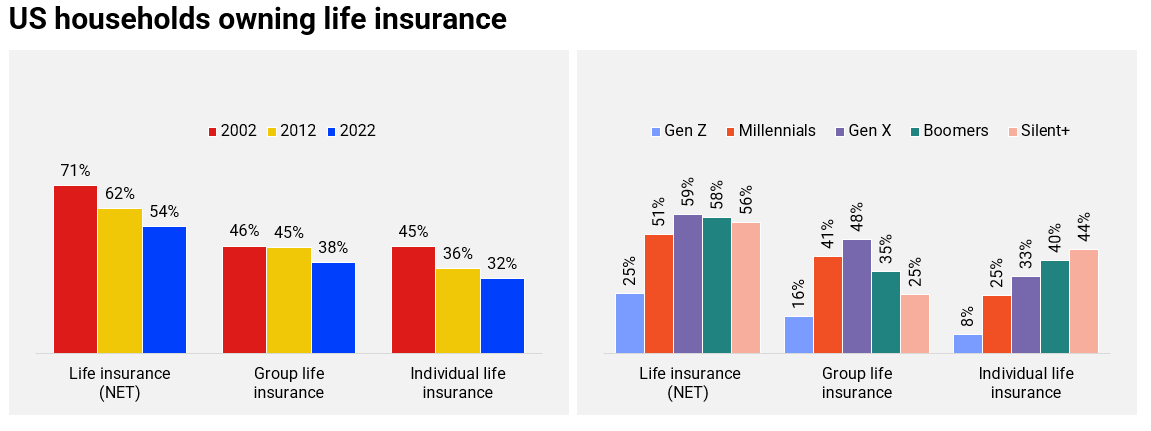

Individual life insurance holdings have also been on a downward trajectory since 2002, with a notable drop in group holdings since 2012. This decline contrasts with the steady recovery in health-related insurance holdings since their dramatic fall between 2002 and 2012. The uptake of Health Savings Accounts (HSAs) has more than doubled in the last decade, driven largely by Millennials and Gen X, with Gen Z not far behind.

A shift towards earlier financial planning

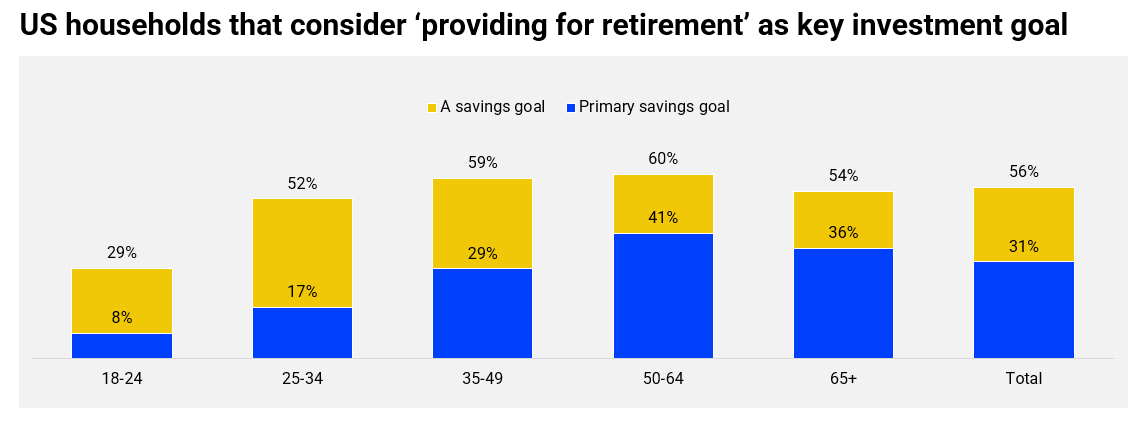

Despite the availability of employer-provided benefits, the utilization of retirement planning, life insurance, and long-term care insurance remains low compared to medical and dental insurance. Retirement planning, however, is becoming an increasingly prioritized goal, as seen in the MacroMonitor data. Many households start considering their retirement plans around age 30, with a growing proportion beginning even earlier, highlighting a shift towards early financial planning.

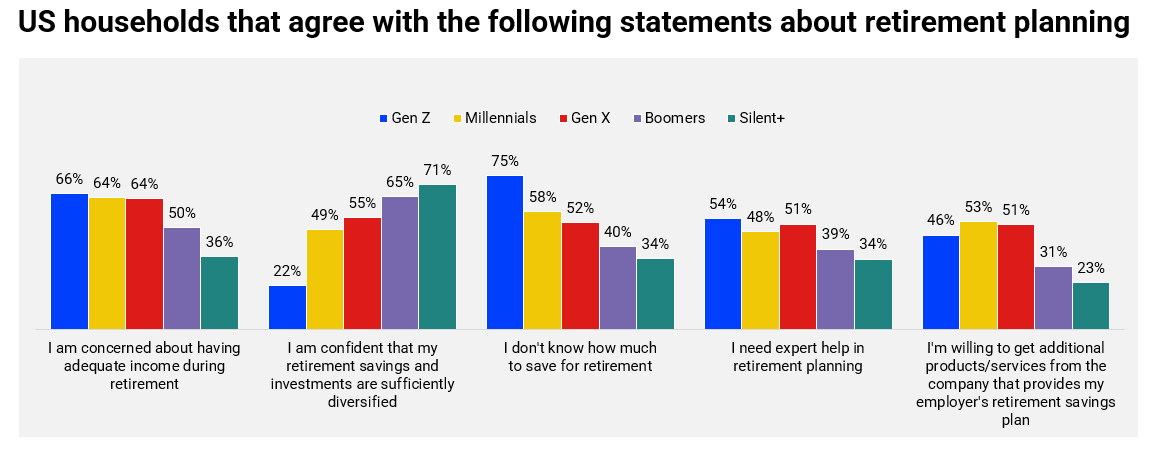

Younger generations, particularly Gen Z, face unique challenges in retirement planning. They often feel less organized and confident in their financial decisions, primarily due to a lack of information and clarity on how much to save. This demographic is more likely to seek expert help online, showing a preference for digital financial planning tools and automated investments.

Financial institutions have a significant opportunity to support these younger households. Providing accessible and reliable online financial advice can bridge the confidence gap for Gen Z and Millennials. Institutions should leverage digital platforms to offer personalized financial planning services, automated investment options, and comprehensive retirement planning tools. By doing so, they can attract and retain younger clients who are eager for guidance but unsure where to find it.

Bridging the life insurance awareness gap

One of the key barriers to life insurance uptake among younger generations is awareness. MacroMonitor data shows that while Gen Z, Millennials, and Gen X recognize the value of life insurance for long-term savings, many have not adopted these products due to a lack of contact from relevant salespeople. This indicates a substantial gap in outreach and education efforts by financial institutions.

Affordability, while a concern, has become secondary to the primary issue of awareness. Many younger consumers may have misconceptions about the cost of life insurance, assuming it to be excessively expensive. Financial institutions need to work towards dispelling these myths through clear, transparent communication and educational campaigns that better demonstrate the affordability and value of life insurance products.

Given the digital-native nature of younger generations, social media and informative webinars can be powerful tools for educating consumers about life insurance. Interactive tools and calculators available on mobile apps and websites can also help these consumers understand how much coverage they need and what it will cost, making the decision-making process more accessible and less intimidating.

The role of self-reliance and professional advice

There is a noticeable trend of households becoming more self-reliant in financial decision-making. Younger generations are increasingly taking financial matters into their own hands, often out of necessity due to a perceived lack of affordable and reliable financial advisors. This self-reliance, however, does not necessarily translate into confidence. Many young adults feel overwhelmed by the complexity of investment decisions and the multitude of financial products available.

Despite their willingness to handle financial planning independently, younger generations often express a desire for professional guidance to help them navigate the complex world of retirement planning. As seen in the MacroMonitor data, there is substantial interest among Gen Z and Millennials in acquiring expert help for retirement planning, with a significant portion of this demographic likely to seek professional advice in the next 12 months. This interest is often driven by the realization that professional advice can provide a clearer path to achieving long-term financial goals, particularly in an environment where economic uncertainties and market volatility are common.

Offering digital advisory services, which combine the convenience of online tools with the expertise of seasoned financial advisors, can meet the needs of younger consumers. These services can include virtual consultations, real-time chat support, and personalized financial plans that adapt to the user’s evolving financial situation. By bridging the gap between self-reliance and professional advice, financial institutions can help younger generations build confidence in their retirement planning while fostering long-term client relationships.

Financial institutions have a crucial role to play

The landscape of retirement planning in the US is undergoing significant changes, driven by generational differences and evolving economic conditions.

Financial institutions have a crucial role to play in helping consumers achieve their retirement goals. As the next generation approaches retirement with different expectations and challenges, the financial industry must adapt to meet the evolving needs of consumers, to ensure all are adequately equipped by the time they reach retirement.

Subscribe to get the latest RFI data and insights.

About MacroMonitor

Representing the views of 130 million US households, MacroMonitor uniquely provides 360 insights into all aspects of household financial behavior, attitudes, needs and trends. Across all financial products.

Luke Allchin

Director, North America

Luke Allchin is a Director, North America at RFI Global, leading financial services research and advisory across the North American market.

View full profileData-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.