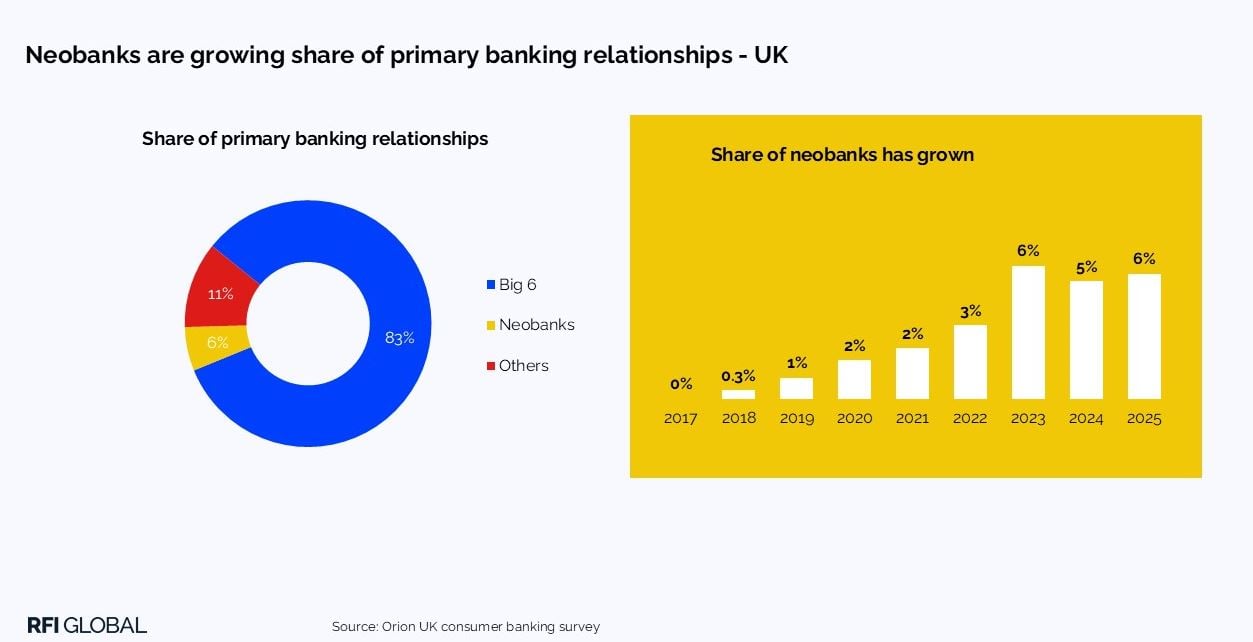

Ten years ago, fintechs erupted onto the banking scene with super cool user experiences on their apps and funky marketing. Neobanks were the poster child for the fintech movement, especially in the UK. According to data from RFI Global’s Orion programme, digital-only providers are finally coming of age with their share of primary relationships in the UK increasing from 1% in 2019 to 6% in 2025. However, despite this headline–grabbing success not everything is going their way.

As Clinton Cheng from Visa points out in our Banking Uncovered podcast, they have benefited hugely from increased mobility in banking. He says, “Twenty years ago it was the large incumbent banks with access to cash, broad product offerings and large physical infrastructure” who were the number one choice for consumers. As mobility has increased and services like Visa Cash App partner with Chime to provide access in retail stores, the ability to bank anywhere has increased. This has been further intensified with all the bank branch closures in most markets. Clinton points out that, “while getting cash from a retail store is not an elegant customer experience, it is better than not being able to access an ATM from a branch that has now closed.”

Capturing customers of tomorrow

Neobanks have also been fantastic at capturing the customers of tomorrow with their travel products. Previously, one of the easiest ways to acquire customers was when they first started needing financial products of their own, such as a travel card. Banks could then acquire them and migrate them to their broader offerings as they transitioned through life stages. Neobanks replaced prepaid travel cards with their offerings. Clinton points out that the transparency over transaction figures that neobanks like Revolut offer has allowed them to win significant market share in the UK. As Clinton says, what’s really interesting is that they allow you to lock in FX rates for future dates. Visa is now seeing the growth of a new segment of single household travellers who by 2030, will represent 25% of all international travel. Interestingly, they are booking their next vacation based on where the currency fluctuation gives them the best deal, so Japan is extremely popular at the moment.

The challenge for neobanks

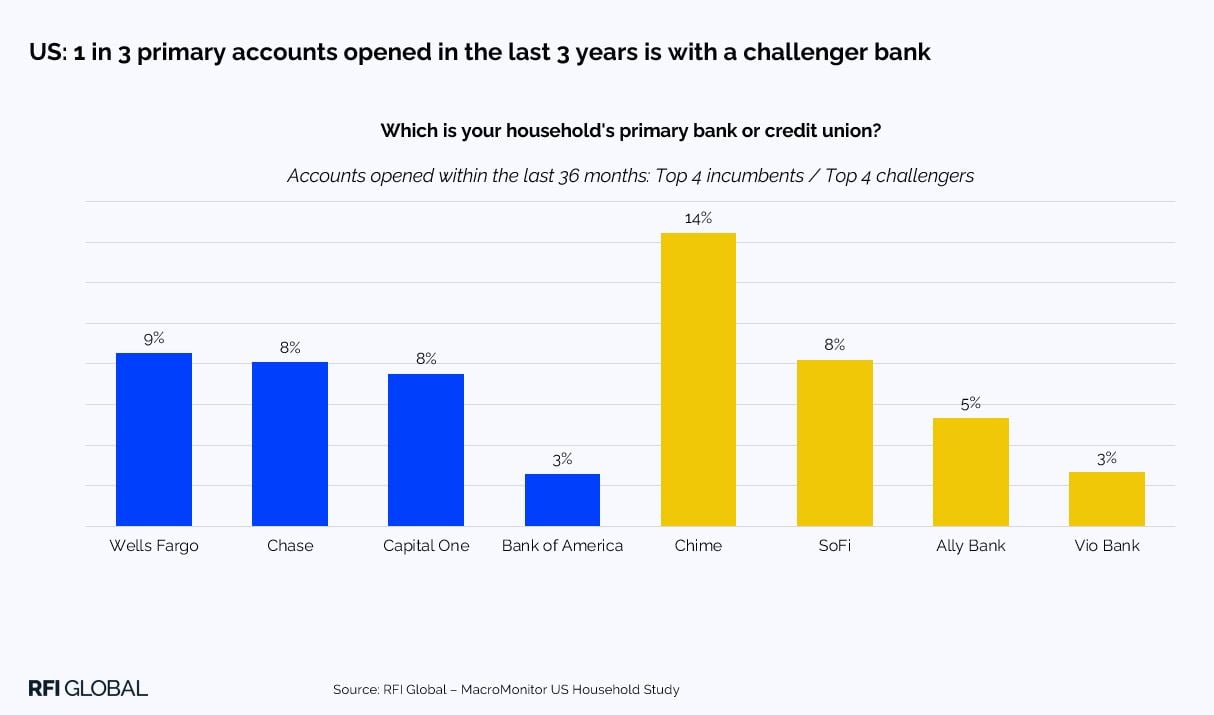

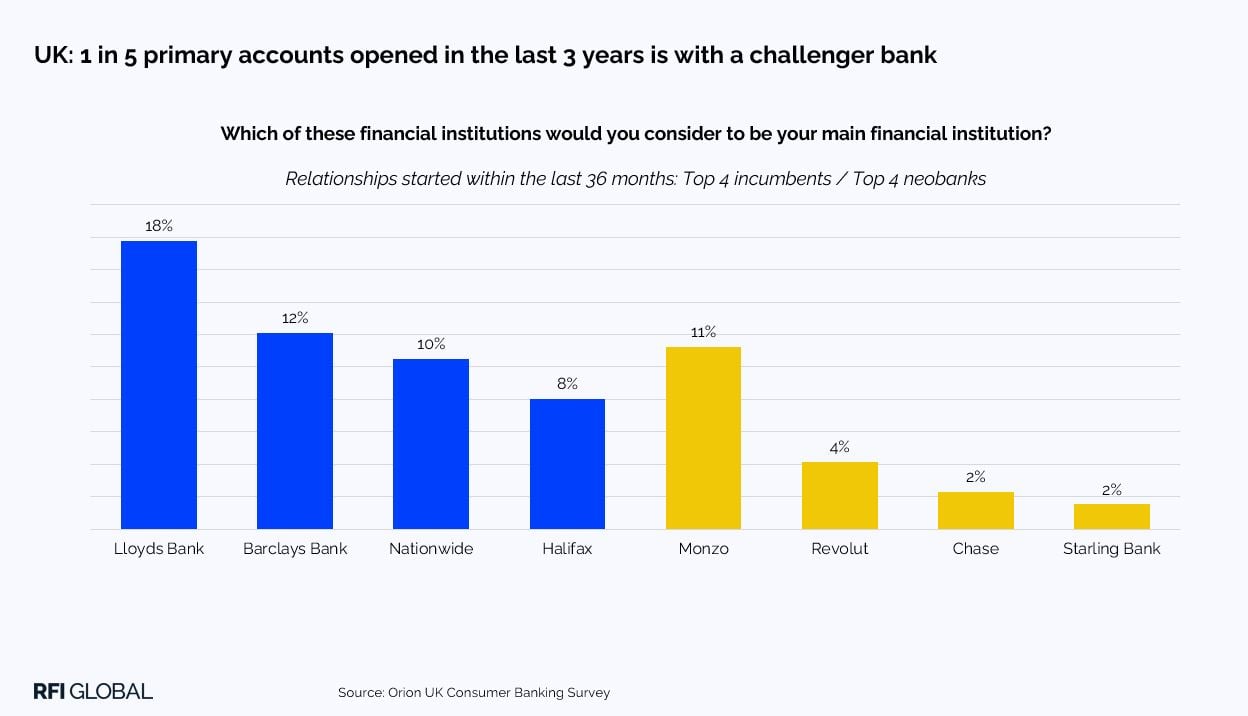

The first challenge neobanks have is to acquire not just relationships but to become the primary financial provider or main bank. According to RFI data, they have been successful at this in both the US and the UK.

With 33% of primary bank accounts opened with challenger banks in the US in the last 3 years and 20% in the same period in the UK, their results are staggering. On top of that, in the US Chime would be 1st and in the UK Monzo would be in joint 2nd with Barclays based on acquiring primary relationships over this period.

Whether or not the neobanks continue to acquire share will depend on how well they produce broader and deeper product lines that reflect the life stages of their customers as they mature, and this is the heart of the problem. Traditionally, they have built from travel and prepaid cards to deposit products and checking/current accounts. The next phase is offering the more profitable credit products and with this comes regulation and greater complexity. Neobanks burn cash, so they are heavily investor-backed. Typically, investors underestimate both the complexity and cost of regulation, giving the traditional banks a significant advantage over their new competitors.

What next?

The current volatile geopolitical situation possibly represents the most danger to neobanks. As the IMF cuts its forecast to almost all advanced economies and to the global economy, it is almost certain that interest rates will go down. This plays to the advantage of the traditional banks. They have much broader and deeper product portfolios on the credit side, allowing them to offer slightly higher deposit rates for longer. The cash burn rate of any neobank competing with this can quickly prove fatal. The demise of Xinja in Australia a few years ago was an example of this in action. Also, due to a greater spread, they will generate more profits over this period.

On top of that, we may also see another flight to safety. In the 2008 financial crisis, the early digital and challenger banks suffered as there was a consumer psychological need to see a branch. People wanted to see that a bank was made of bricks and mortar. Will this happen again as the economy stutters? Or will this be the time that consumers finally shake free of this shackle in their thinking? There is a huge amount of opportunity for neobanks, but at the moment, they are in both a fantastic position and also potentially in a perilous position. It’s not only a tale of two cities but also possibly the best of times and the worst of times…

A global perspective on the future banking landscap

Listen to the Banking Uncovered podcast with Clinton Cheng at Visa here, where we dive deep into the dynamics of digital banking, consumer behaviour, cash access and what’s next for the fintech movement. And get in touch for more insights from our UK or US data.

Data-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.