There is no doubt that the financial services sector is evolving rapidly around the globe. In this blog, I’d like to shine a light on Australia and New Zealand (ANZ) and the specific developments and implications for the region’s banks.

The word ‘unprecedented’ is often overused, but I feel it is pertinent in the current environment. The last 12 months have seen the advancement and adoption of generative AI into mainstream banks in ANZ in a way that will ultimately change how servicing and communication are executed across the industry forever. This has all happened against the backdrop of consistently low consumer sentiment driven by consistently high inflation and the cost of credit.

Five trends shaping the future of financial services

RFI Global’s Financial Services Trends and Predictions 2025 dug into five of the top themes that we see playing out in 2025, based on our analysis of over 200,000 consumers and 60,000 businesses worldwide. These were:

1. Winning loyalty in a world of change. When the cost of living and the rise of new competitors collide to drive up consumer choice, loyalty to traditional institutions is at risk.

2. The digital edge. Fintech and AI are shifting customer expectations and financial institutions must meet these expectations at every touchpoint.

3. Navigating market volatility. Saving and borrowing behaviour is changing with interest rates, and providers will need to renew their focus on retention and deepening relationships.

4. The wealth advantage. The Emerging Affluent segment is growing and driving demand for diverse investment classes. Financial service players will need to ensure they can match the demand.

5. Unlocking cross-border payments. Inefficiencies persist in what is an essential enabler of global trade, presenting opportunities for the right competitors and model.

I’d like to focus on the three trends that I believe are most critical for the ANZ region and highlight the nuances that exist.

Winning loyalty

Australia and New Zealand have seen a significant influx of innovation and new fintech players in the last few years. Consumers now have a plethora of options available to them when it comes to choice of service provider. This has driven an increase in the proportion of consumers looking to switch their primary transaction account (in Australia it’s up 4 percentage points on a long-term average of 10%).

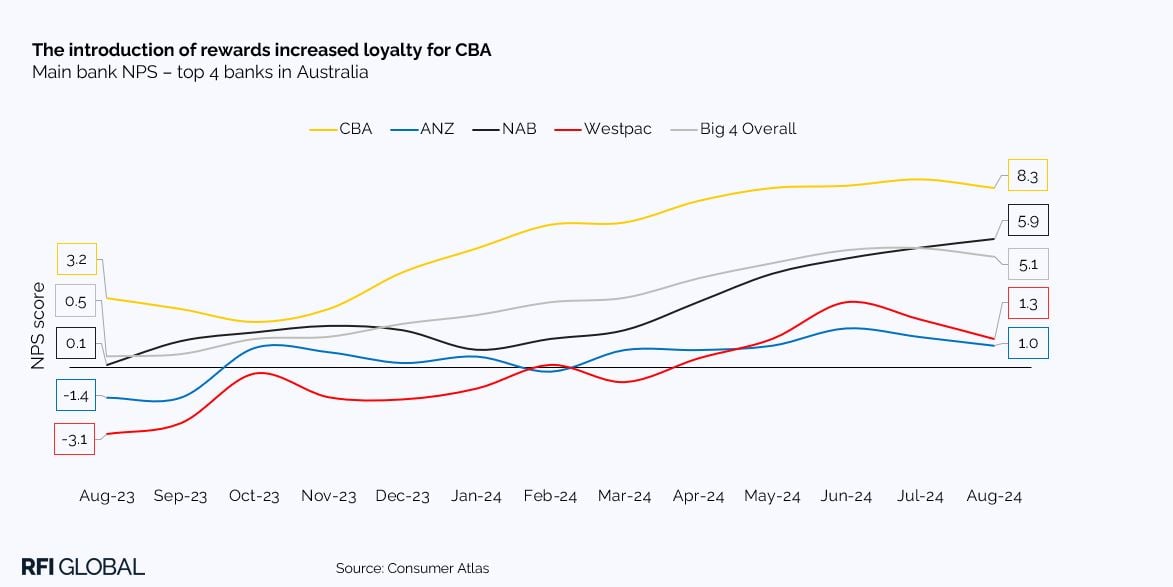

The response from banks has been to get on the front foot when it comes to engendering loyalty. We’ve seen two of Australia’s largest banks – NAB and CBA, which own two of the largest New Zealand banks, launch bank-wide programmes to engage and reward customers. CBA was the first, launching CommBank Yello in October 2023. Yello offers customers a range of benefits including cashback, personalised discounts and offers and prize draws for all active customers with minimum friction.

Has it made a difference? The answer is yes. Since the introduction of Yello, CBA’s Net Promoter Score (NPS) has increased significantly, from +2.1 in October 2023 to +8.7 in July 2024 (a record for the major Australian banks) and has maintained a high level since.

The digital edge

The implications of digital advancement extend beyond loyalty and into how consumers expect to be serviced and how they self-service. This is notable in the way they research and select financial services products, with an increase in usage of live chat and virtual assistance as well as AI tools and social media.

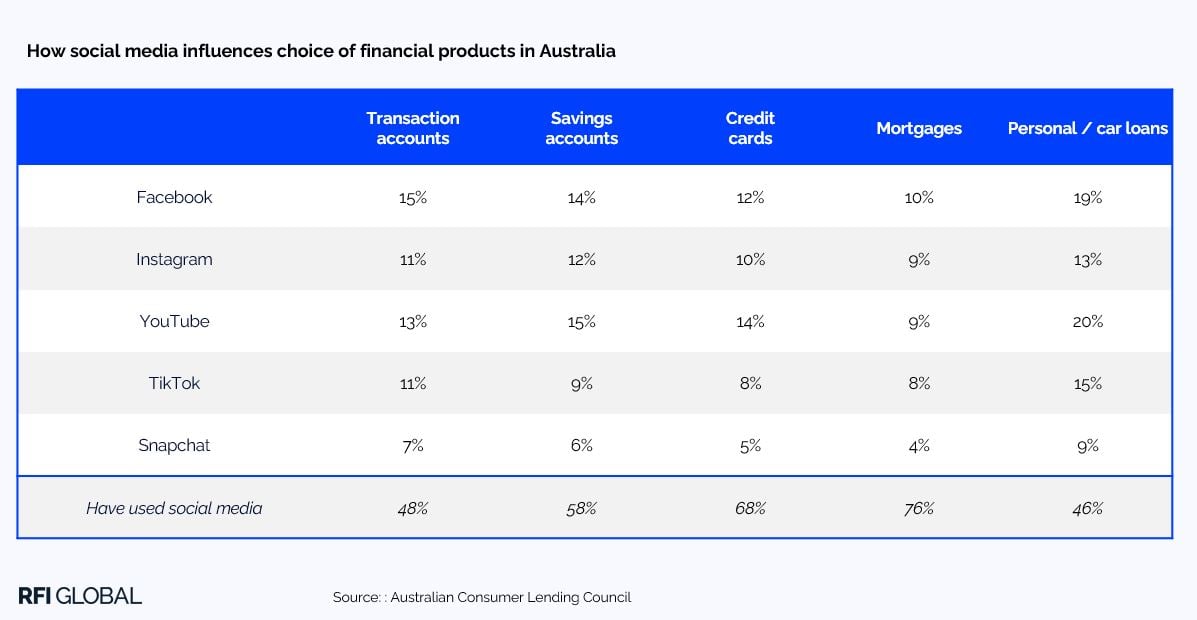

One of the most noticeable shifts in Australia has been how social media is reshaping financial product decisions, especially mortgages and credit cards where 76% and 68% of consumers turn to platforms like TikTok and Instagram for advice. Across all products more than 1 in 2 consumers say social media plays a role in influencing their choices.

Market volatility

I’ve already alluded to how global cost pressures and interest rates have influenced consumer choice when it comes to saving and borrowing. As interest rates rose, consumers were encouraged to put their money into cash deposits.

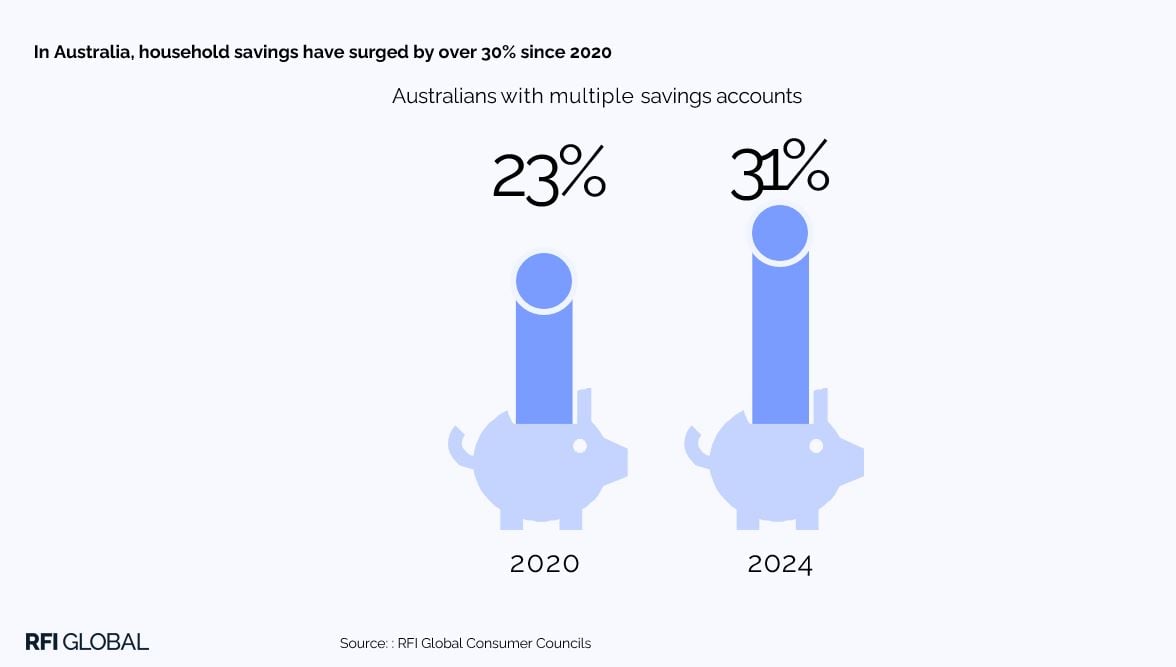

In Australia, for example, household savings have surged by over 30% since 2020. The percentage of savers holding multiple accounts has risen from 23% to 31%, and 74% of consumers now check competing rates, up from 65% in early 2022, highlighting increased financial vigilance.

The outlook for 2025 though is that interest rates will reduce (or continue to reduce) and this will introduce a new dynamic to customer behaviour. In Australia and New Zealand, the countries’ reserve banks have so far chosen very different paths when it comes to interest rates in the last few months. The RBNZ has taken one of the most aggressive stances globally, reducing rates (and thus the cost of credit) in three of the last four months, while the RBA is holding firm and at the time of writing had not reduced rates.

While we expect to see customers waiting to see when and by how much rates will fall before making decisions, we believe customers will place greater importance on product flexibility, wanting the freedom to move and change their behaviour across their savings products and the ability to reduce their costs when it comes to credit.

Higher savings rates gave financial institutions the opportunity to use savings products to attract new customers in ways that would not be possible in a lower-rate environment.

What does this mean for ANZ banks and institutions?

In Australia and New Zealand – as in the rest of the world, new digital developments are enabling consumers to access lower-cost, frictionless solutions to their banking and payments that appeal in an environment of higher costs.

Traditionally, a few major banking brands have dominated Australia and New Zealand. In 2025, these brands will be challenged by new players and new customer demands and expectations.

The institutions that successfully embrace new technologies to better meet their customers’ needs in what will be a dynamic market in 2025, will win. Regardless of size or legacy.

Subscribe to get the latest RFI data and insights.

Data-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.