In 1997 the world was shocked when Garry Kasparov, the world’s greatest chess player, was defeated by Deep Blue, the IBM supercomputer. In his book, Deep Thinking, Garry Kasparov writes about this and the implications of AI for humans. One of the most interesting points he makes is that, while he was defeated by Deep Blue in a one-on-one contest, an average chess player combined with an average desktop computer can beat Deep Blue every time. It is the combination of the digital working in partnership with the human that is unbeatable. This has lots of implications as we travel at what seems like an ever-increasing hyper speed into AI, but also provides a good analogy for the opportunity and future potential for both banking and especially SME banking.

The implications for SMEs

As an SME owner I’m always fascinated by the innovation and product development occurring in the SME banking space. While the digital evolution for consumers is well known and documented the corresponding evolution for SMEs is less so. It has been much more dramatic, more impactful and solved many more pain points. As I said in my last blog, many solutions which are simply ‘nice to have’ for consumers, are absolutely ‘must have’ for SME owners and solve real pain points for them. The plethora of well thought through products and offerings for anyone starting a business today compared to 20 years ago is both staggering and encouraging.

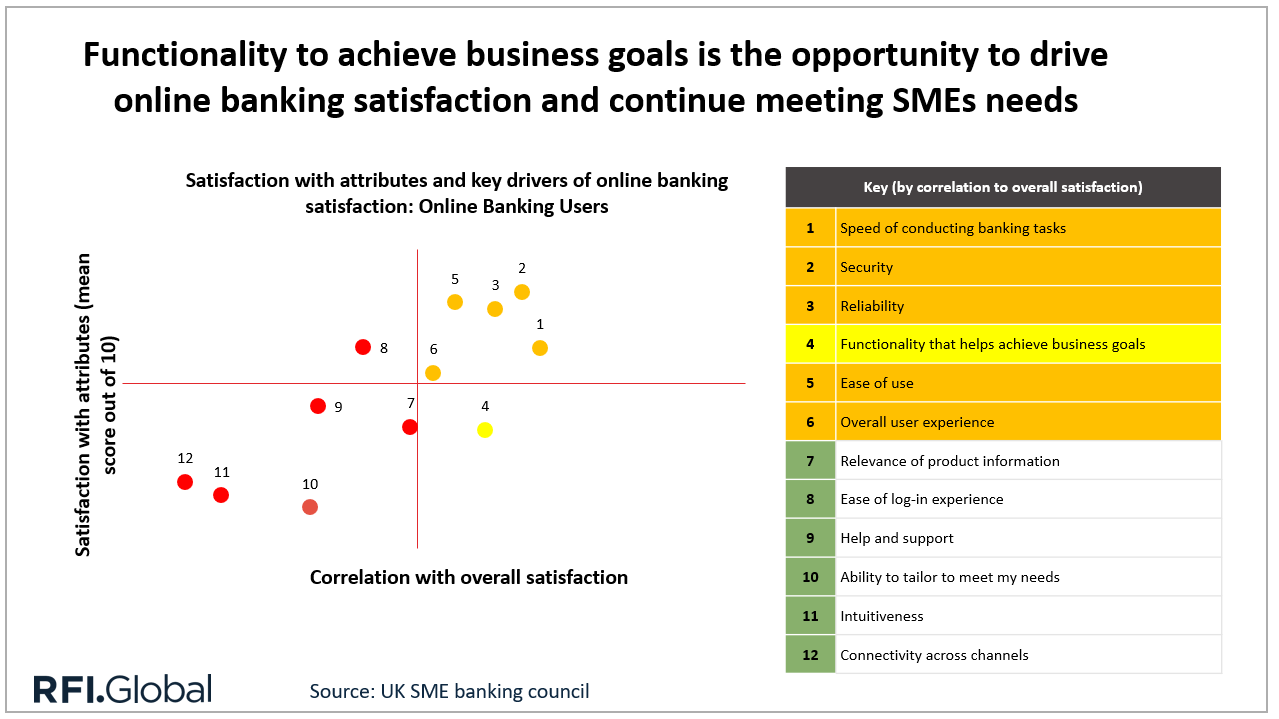

RFI Global’s data shows that the biggest pain point for SME owners is a lack of innovation in digital banking. When asked further to clarify this SMEs state that banks are failing to provide functionality that helps the business achieve its goals.

One of the top challenges facing SMEs is bookkeeping with 1 in 5 citing this as their top challenge every year since 2020. So, what is the result of these pain points and challenges? The result is a huge appetite among SME owners for value added services that integrate business banking and accounting software. The number of SMEs in RFI Global’s data citing this as their most preferred value tool increased in 2023 to almost 1 in 3. As Richard, CEO of Allica says in our Banking Uncovered podcast, ‘software that seamlessly attaches to both banking and accounting is where you can create the ease, convenience and speed that SMEs want.’ RFI Global’s data in every market shows that ease, convenience and speed are the top three drivers of SME banking choice.

The need for ease, convenience and speed

This is an area that has grown substantially in recent years. More and more banks, challengers and fintechs are now offering accounting software as a value-added service as part of their SME banking proposition. However, this relatively new offering, enabled recently by fintechs and digital solutions has quickly moved from a wow factor to a hygiene factor. Richard states, ‘integration with accounting software is now a must have in any SME banking proposition’.

The fact that it has moved from a value-add wow factor to a must have hygiene factor is further validated by RFI Global’s data which shows that SMEs now increasingly rank this as a key driver of switching their main bank. Accounting software integration ranks as one of the top 5 drivers and the numbers of SMEs ranking it as the top number one driver of switching has increased from 3% to 14% in just a few years – exponential growth although coming off a low base. So, if bank and fintechs can provide a digital value-added service with accounting software that meets the number one pain point and challenge for SME owners what’s has all this got to do with Garry Kasparov. The answer lies in one word – trust.

Trust is huge in banking

Trust is the most important factor for every customer in every market globally. As Richard states,’ you can’t magically create trust overnight – you need to build trust through consistent positive interactions and customer experiences for the SME owner.’ Where traditional banks and hybrid models like Allica have an advantage over app only providers/ fintechs is the human element and this is essential in building trust. The number one reason SME owners want to speak to a human is to resolve a problem that, for whatever reason, they can’t resolve digitally. They might want to do it in a branch, over video or increasingly, as I’ve discussed in previous blogs, via a chat. If you can be present in whatever channel the SME owner wants to operate in, to answer questions that they have with a human, then you can begin to build trust.

Whether you are a traditional bank, a challenger brand or a fintech, it is the ability to both provide a digital solution to a significant pain point (in this case integrating accounting software with their business banking) combined with the ability to interact with a human to build the critical trust that provides the basis for an unbeatable combination to underpin success. As Garry Kasparov states the future lies in digitally enabled human solutions / the humanisation of digital capabilities.

Listen to our Banking Uncovered podcasts here or get in touch to find out more about the survey results.

Subscribe to get the latest RFI data and insights.

Data-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.