Kieran Hines, Director, EMEA & North America

Last week, OpenAI announced a new set of personal finance tools in preview for ChatGPT Pro users in the United States. Users can now connect their bank accounts, credit cards and investment portfolios directly to the tool, with Plaid managing account connections across more than 12,000 financial institutions.

At first glance, you’d be forgiven for seeing this as little more than a feature launch. In a sense, there isn’t necessarily anything new here. Customers have been using fintechs and third parties to aggregate and manage their finances for years, and engagement with incumbent providers remains relatively strong.

What is different this time is the ability for ChatGPT to move from giving pointers to a customer looking to build deposits to providing a list of potentially suitable accounts for them to consider. In other words, putting it in a central position to influence future product sales. The nightmare scenario of big tech playing this role in the value chain was mooted years ago, but never came to pass. This partnership will doubtless raise those same concerns again.

For senior executives at banks, the questions are urgent. What kind of threat will this pose to the customer relationship? What impact does it have on your ability to cross-sell? And how should banks be bringing open banking and AI together in their digital channels?

We know customers are ready

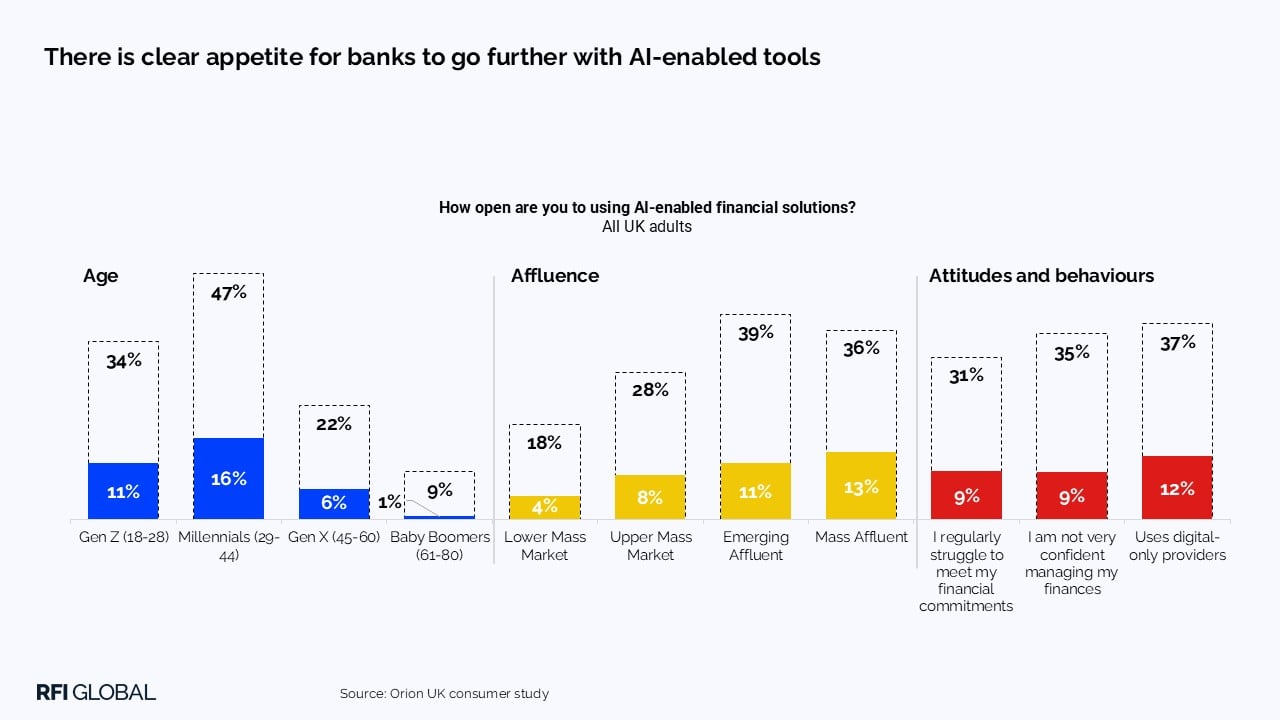

The consumer appetite for AI-driven financial management was already clear before this announcement. Our latest research, drawing on insight from 16,000 UK consumers per year through our Orion study, shows that 8% of adults are already using AI tools for financial advice or support. That figure may sound modest, but it skews towards the very segments many banks are striving to attract and retain: younger, more affluent and digitally engaged consumers.

More striking still is the gap between current behaviour and stated intent. Around 29% of UK banking customers say they are interested in AI-enabled financial solutions, which is roughly three times the proportion already using them. That equates to millions of people waiting for a credible provider to deliver it.

The Plaid and ChatGPT announcement shows OpenAI has decided it wants to be that provider. Banks need to decide whether they are going to compete, collaborate or cede the ground entirely.

What this means for open banking

Plaid provides the infrastructure for permissioned access to financial data, allowing customers to give consent for third-party applications to access their information. What the ChatGPT integration changes is not the underlying infrastructure, but the ambition of what sits on top of it.

To date, much of open banking has supported relatively narrow use cases: enhanced account aggregation, simpler product applications, or A2A payments. While these add value, none is transformative on its own.

What the ChatGPT integration does is place a sophisticated natural language interface on top of that data, one capable of contextualising spending patterns, surfacing savings opportunities, modelling financial scenarios, and responding to questions that consumers would never ask a branchadvisor.

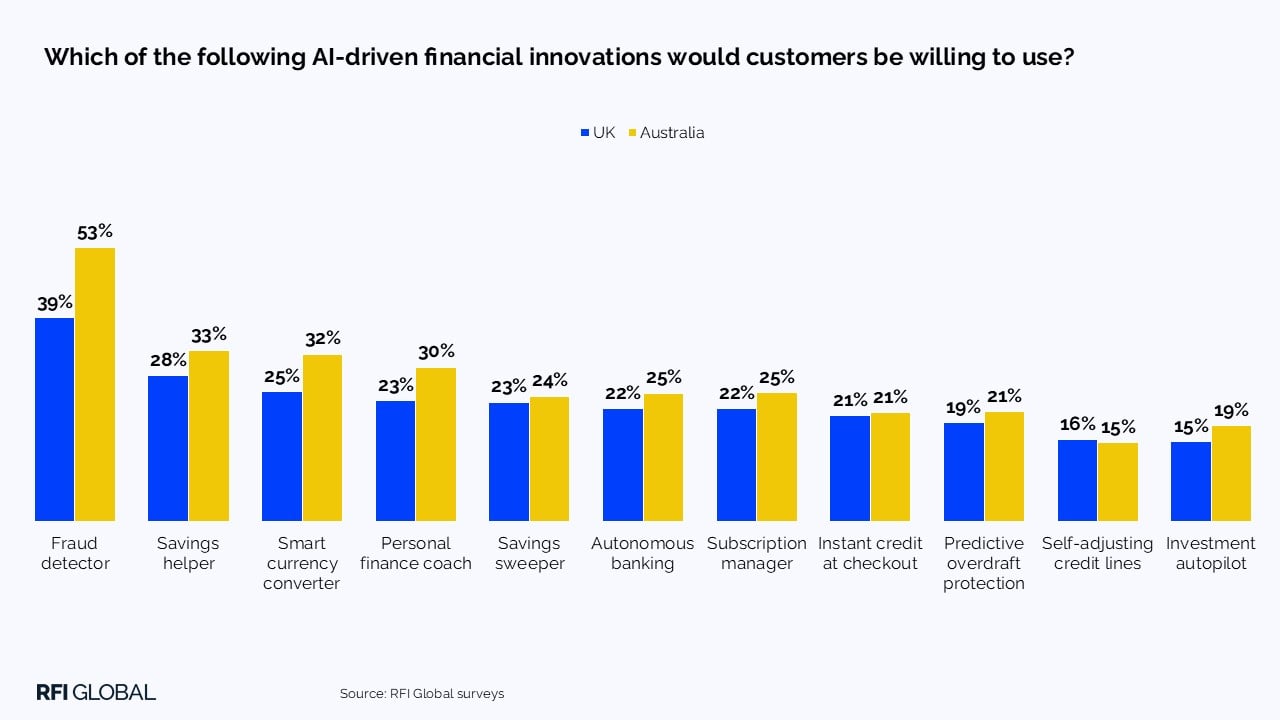

According to OpenAI, more than 200 million people already use ChatGPT each month to ask finance-related questions. Until now, those interactions were limited by what the customer could provide. The Plaid connection changes that entirely, moving ChatGPT from something more akin to a reference tool towards something that can offer a form of personalised financial support.

The implication for banks is clear. If customers are directing financial questions to ChatGPT and it can answer based on their actual account data, the bank’s app becomes less important as a primary interface for financial insight.

The opportunity banks should be seizing

The risk of framing this purely as a threat is that it misses the more important question: what could banks build if they combined their own data, their customer relationships, and AI capabilities in the same way, but with the trust advantage that only a regulated institution can offer?

Trust matters enormously here, and it is an asset banks still hold in relative abundance. When we ask consumers what would make them more comfortable with AI in banking, the answer consistently points to credible, regulated providers as their preferred source.

The architecture to build this already exists. The question is not whether the pipes are there; it is who builds the most compelling experience on top of them.

Three areas stand out where banks are well placed to compete.

1. Deep personalisation: Banks hold a wealth of contextual information on customers (e.g. lending history, product usage patterns, life stage signals), a significant data advantage that can be translated into genuinely useful experiences.

2. Proactive and agentic capability: Our research shows that more than one in five consumers is already comfortable with some level of automation in areas like savings, subscriptions and payments, and appetite is even stronger among those who lack financial confidence.

3. The ability to transact: Perhaps the biggest advantage for banks is the ability to allow customers to close the loop from advice to action.

What should banks do next?

The Plaid and ChatGPT announcement is the beginning of a more competitive phase in which the interface layer of financial services becomes genuinely contested territory.

This is not fundamentally a technology decision – it’s about product and positioning. The challenge is not whether to use AI or open banking, but how quickly banks can combine them in a way that is visibly useful to customers and credibly differentiated from what a generic AI platform can offer.

Our data clearly shows that consumer demand is running ahead of current bank propositions. Those using AI tools for financial advice are not waiting for banks to invent the concept, they are waiting for banks to deliver it. The window to do this on their own terms is narrowing.

If you’d like to understand where your customers sit on AI adoption – and what they expect next – get in touch for further insights from our surveys.

Kieran Hines

Director, EMEA & North America

Kieran Hines is Director at RFI Global, leading research and advisory work across EMEA and North America. He is a senior financial services analyst with deep expertise in retail and business banking, payments and digital transformation.

View full profileData-driven insights for financial service leaders

Subscribe to The Banknote, our monthly newsletter delivering expert perspectives and exclusive analysis, powered by 200,000 consumer and 60,000 business interviews each year to help you stay ahead in a fast-changing financial world.